This Week in Earnings – Q3’24

The Sector Beat: Consumer Discretionary

Earnings season continues to march on, demonstrating that it’s tough out there from a top-line perspective. Something to be aware of, more companies continue to highlight cost-cutting initiatives, raising the level, while layoff announcements and restructurings underpinned by headcount reductions are on the rise. These are not positive signs. That said, the big wildcard is the unprecedented U.S. Presidential Election. In less than a week, the world will finally have the clarity it is seeking (hopefully) and a new set of dynamics will emerge.

Never a dull moment and all we can do is remain agile, envision, and execute!

In today’s thought leadership, we cover:

- Key Events this week

- Earnings Snap, covering the S&P 500 stats to date

- Spotlight on Consumer Discretionary in The Sector Beat

Key Events

Employment

- Nonfarm payrolls grew by 12,000 in October, well below consensus for a 113,000 increase. September and August were revised down by a combined 112,000. The unemployment rate held steady at 4.1%, in line with consensus. Average hourly earnings rose by 0.4% MoM, matching September’s increase and slightly ahead of 0.3% consensus. (Source: Bureau of Labor Statistics)

- Initial jobless claims came in at 216,000 for the week ended Oct. 26, below consensus for ~230,000 and down 12,000 from the prior week. Applications for U.S. unemployment benefits fell to their lowest since May as southeastern states continued to recover from the impact of severe storms. Continuing claims, a proxy for the number of people receiving benefits, fell to 1.86M in the previous week. (Source: Labor Department)

- Employment cost index (ECI), the broadest measure of labor costs, rose 0.8% in Q3. That was the smallest gain since Q2’21 and followed an unrevised 0.9% increase in Q2. Labor costs gained 3.9% YoY through September, the smallest rise since Q3’21, and down from 1% in Q2 and the 4.3% annual pace observed in Q3’23. (Source: Labor Department)

- September JOLTS report showed job openings at 7.443M, well below 7.900M consensus, down 1.9M YoY to the lowest level since March 2021. Quits rate was little changed at 1.9%, while layoffs rate rose slightly to 1.2%. Report pushed the job vacancies per unemployed worker ratio down to 1.1, suggesting further loosening of labor markets. (Source: Labor Department)

GDP

- U.S. GDP increased at a 2.8% annualized pace after rising 3.0% in the previous quarter. Consumer spending, which comprises the largest share of economic activity, advanced 3.7%, the most since early 2023. The acceleration was led by broad increases across goods, including autos, household furnishings, and recreational items. (Source: The Commerce Department)

- Eurozone Q3 GDP reports topped estimates. GDP in the 20-nation area that uses the euro currency grew 0.4% in Q3, better than expectations of 0.2% and accelerating from 0.2% in Q2. (Source: WSJ)

Consumer Confidence

- October consumer confidence jumped to 108.7, well ahead of consensus for 99.4 and September’s 99.2 headline level (revised up from 98.7), representing the strongest monthly gain since March 2021 and highest level since August 2023. (Source: The Conference Board)

Inflation

- The core personal consumption expenditures price index, which strips out volatile food and energy items, increased 0.3% in September and 2.7% from a year earlier. Overall inflation was 2.1%, the lowest since early 2021 and just above the central bank’s 2.0% goal. (Source: Bureau of Economic Analysis)

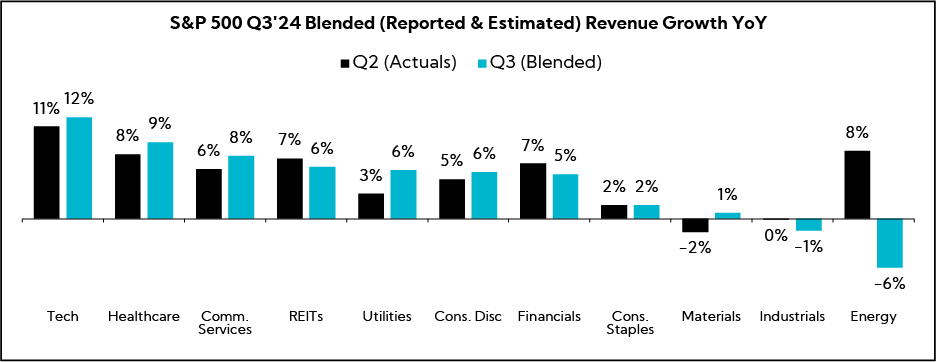

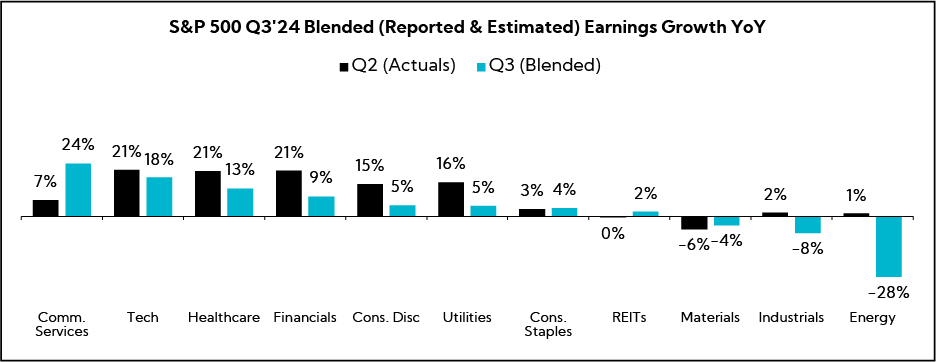

S&P 500 Earnings Snap

65% of the S&P 500 has reported earnings to date

Q3'24 Revenue Performance

- 58% have reported a positive revenue surprise, below the 1-year average (63%) and the 5-year average (69%)

- Blended revenue growth (combines actual reported results for companies and estimated results for companies yet to report) is 4.8%; this compares to last quarter 5.5%

- Companies are reporting revenue 1.5% above consensus estimates, above the 1-year average (+1.1%) and below the 5-year average (+2.0%)

Q3’24 EPS Performance

- 77% have reported a positive EPS surprise, below the 1-year average (78%) and in line with the 5-year average (77%)

- Blended earnings growth (combines actual reported results for companies and estimated results for companies yet to report) is 7.4%; this compares to last quarter’s 13.2%

- Companies are reporting earnings 7.7% above consensus estimates, above the 1-year average (+6.5%) and below the 5-year average (+8.6%)

The Sector Beat: Consumer Discretionary

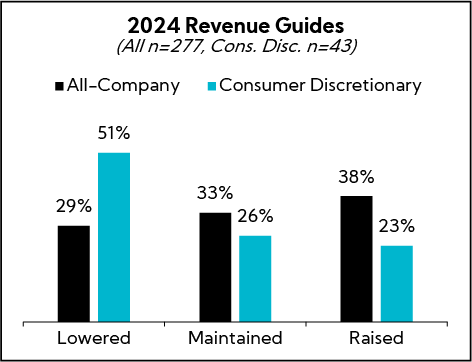

Guidance Trends

Each quarter, we analyze annual revenue and EPS guidance provided by Consumer Discretionary companies with market caps greater than $1B that have reported to date.1 Below are our findings.

For comparison purposes, we provide an “All-Company” benchmark, which tracks in real-time a basket of companies larger than $1B in market cap across all sectors that have reported earnings to date (n = 377).

Guidance Breakdown by Industry

| Industry | Number of Companies |

|---|---|

| Specialty Retail | 9 |

| Textiles, Apparel & Luxury Goods | 8 |

| Automobile Components | 8 |

| Hotels, Restaurants & Leisure | 6 |

| Diversified Consumer Services | 5 |

| Household Durables | 4 |

| Leisure Products | 2 |

| Distributors | 1 |

| Total | 43 |

Source: Corbin Advisors

Annual Revenue Guidance

Far more Consumer Discretionary companies are lowering annual revenue guidance figures than the all-company average. Of note, more than a third of those lowering guidance came from Auto-exposed companies, followed by Textiles, Apparel & Luxury Goods, and Specialty Retail. Those raising guidance were a mixed bag across the sector, although none of the auto-exposed companies fell within this group.

- Companies that lowered guidance (n = 22)

- 59% lowered the top and bottom

- 36% lowered the top and maintained the bottom

- 5% lowered the top, but raised the bottom

- Average midpoint of -1.8% growth YoY versus 0.2% last quarter

- Average spread decreased by 170 bps to 1.3%

- Companies that maintained guidance (n = 11)

- Average midpoint of 2.3% growth

- Average spread of 1.3%

- Companies that raised guidance (n = 10)

- 80% raised the top and bottom of the original range

- 20% maintained the top, but raised the bottom of the original range

- Average midpoint of 8.1% growth versus 7.5% last quarter

- Average spread decreased by 30 bps to 1.1%

- Overall midpoints assume 1.5% annual growth vs. 1.6% analyst estimates, on average

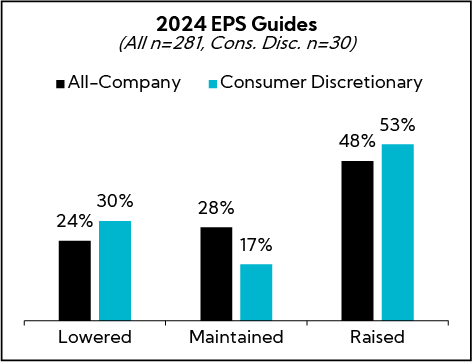

Annual EPS Guidance

More Consumer Discretionary companies are raising annual EPS guides than maintaining or lowering, though slightly more are lowering versus the benchmark. Those companies raising EPS guidance point to factors such as operational efficiency, cost reduction, and productivity efforts.

- Companies that lowered guidance (n = 9)

- 100% lowered the top and bottom of the original range

- Average spread decreased from $0.46 to $0.24

- Companies that maintained guidance (n = 5)

- Average spread of $0.15

- Companies that raised guidance (n = 16)

- 63% raised the top and bottom of the original range

- 37% maintained the top, but raised the bottom of the original range

- Average spread decreased from $0.25 to $0.18

Earnings Call Analysis

We analyzed the earnings calls for this group and the broader Consumer Discretionary universe to identify key themes.

Broadly, executives point to a continuation of consumer trends seen in recent quarters, with affordability and strained budgets shifting spending away from higher-ticket discretionary items. That said, while many characterize the environment as challenging — and expect it to remain so in the near term amid macro headwinds and U.S. election uncertainty —executives continue to express cautious optimism toward 2025 with hopes for an improved environment once Fed rate cuts have had a chance to work their way through the system.

Against this challenging macro backdrop, more companies across the sector are lowering revenue guidance than raising. Homebuilders point to buyers remaining on the sidelines amid the volatile interest rate backdrop, with mortgage rates having marched higher, reversing the pullback that came in anticipation of the Fed’s September rate cut. Companies tied to home improvement and automotive markets also cite sluggish demand, particularly for higher-margin discretionary items. Across restaurants, companies are doubling down on value offerings, with some citing strong traction in Q3 and heading into Q4.

At the same time, while top-line dynamics are challenged, companies are offsetting weaker sales through operational efficiency and cost reductions, positioning them for future growth once demand recovers. To that end, more Consumer Discretionary companies are raising EPS guides than lowering so far this quarter. Indeed, with 53% having raised EPS guidance thus far, the sector is outpacing our all-company group at 48%.

Regionally, Europe remains soft with sluggish economic growth and depressed real wages weighing on consumer sentiment. And in China, while consumer trends have worsened and are not seen rebounding near term, executives retain some longer-term optimism for the market. Ex-China, India remains a pocket of strength in Asia.

Key Earnings Call Themes

Execs Continue to Navigate a Challenging Macro Environment amid Ongoing Consumer Pressure and Election Uncertainty; Cautious Optimism Remains for Economic Soft Landing and Rate Relief to be Felt in 2025

- McDonald’s ($209.9B, Restaurants): “It is clear that broad-based consumer pressures persist around the world. Consumers continue to be even more discriminating with every dollar that they spend as they faced elevated prices in their day-to-day spending, which is putting pressure on the [Quick Serve Restaurant] industry. It’s worth noting that in Q1, industry traffic was flat-to-declining in the U.S., Australia, Canada, Germany, Japan, and the UK. And across almost all major markets, industry traffic is slowing. In the context of a difficult macro environment for the industry, we know our customers are looking for reliable, everyday value now more than ever.”

- Ebay ($30.6B, Internet Retail): “Our outlook also contemplates a challenging operating environment due to persistent economic headwinds and several one-off dynamics in Q4, specifically greater consumer attention on U.S. elections and a shorter holiday shopping period this year from Hurricane Milton in early October.”

- Whirlpool ($5.7B, Furnishings, Fixtures & Appliances): “We had a solid quarter and are reiterating our full year guidance. We’re pleased to have delivered sequential margin expansion globally and, most importantly, in North America. We feel good about our pricing actions and cost plans, both of which are on track. While we continue to navigate a challenging macro environment, we see the housing market clearly positioned for an eventual rebound.”

- Hilton Worldwide Holdings ($58.3B, Lodging): “The word ‘resiliency’ that I use to describe our business is getting used a lot to describe the economy. There is a very broad consensus view that the economy has been slowing, but remains strong, resilient, and showing positive growth. The odds of a recession, at this point I think are quite low. I’m not an economist, but that’s the consensus view and I would generally agree with [it]. So, as we think about that as a backdrop, thinking about 2025, what’s going to be the macro, which can drive a bunch of our business, we feel pretty good about it.”

Interest Rates

- D.R. Horton ($58.8B, Residential Construction): “We believe that the volatility of rates, combined with general uncertainty during the election season, is causing some buyers to stay on the sidelines in the near term. To help spur demand and address affordability, we are continuing to use incentives such as mortgage rate buy-downs and we have continued to sell more of our smaller floor plans. For 2025, our homebuilding volume and profit margins will largely be dependent on the strength of the upcoming spring selling season.”

- PulteGroup ($25.9B, Residential Construction): “October has shown the highest web traffic, foot traffic, and lead volume of the year. However, the recent rise in interest rates has [led to] a more typical seasonal selling pattern, and incentives have remained elevated as a consequence. Between rate volatility, the impact of hurricanes, and the upcoming presidential election, the upcoming spring selling season will offer the best assessment of fundamental housing demand. Buyer reaction to the movement rates both down and now up again affirms that affordability remains a tough hurdle to get over for many potential home buyers.”

- General Parts Company ($16.7B, Auto Parts): “In the same way that higher interest rates have had the intended effect muting and slowing down overall growth, we are encouraged by the start of an easing scenario around the world. The UK has reduced rates once in the last, call it, six months; U.S. once; Eurozone three times; Canada three times. There’ll be a lagged benefit to that, but we would hope those types of policy decisions provide a tailwind as opposed to a headwind.”

- Mohawk Industries ($8.6B, Furnishings, Fixtures & Appliances): “In all our regions, market conditions were slower than anticipated, given high interest rates, lingering inflation and lower consumer confidence. Pricing remained under pressure as industry demand in Q3 continued to decline due to slowing in both residential and commercial activity. We expect the recent interest rate cuts in U.S., Europe and Latin America will strengthen the housing markets and increase Flooring sales as we progress through next year.”

- Brunswick Corp ($5.4B, Recreational Vehicles): “The downward movement in interest rates in the U.S. and some other markets since the beginning of the quarter is welcome and is already benefiting consumer financing costs and dealer floorplan costs. However, given the points in the current retail selling season, we do not anticipate benefits until 2025.”

Challenging Market Conditions Persist for Many on the Top Line, Leading to Lowered Guides; Those Raising EPS Outlooks Highlight Strong Execution and Operational Discipline

- General Parts Company ($16.7B, Auto Parts): “Our results for Q3 missed our expectations. Our outlook in July included anticipated improvements in market conditions in Europe and global industrial activity, neither of which materialized. Given our results to date, and our expectation that these weaker market conditions will likely persist for the balance of the year, we’ve adjusted our 2024 outlook accordingly. While many of these factors are outside of our control, we remain focused on controlling what we can, and we’re confident in eventual market tailwinds.”

- O’Reilly Automotive ($68.43B, Specialty Retail): “While we are cautious that the current macro pressures could persist as we finish out 2024 and enter next year, we are confident our industry will return to more historical growth rates in the short term. Against this backdrop, we are tightening our full year comparable store sales guidance and are now expecting a full year increase of 2% to 3% [versus 2% to 4% previously]. As a reminder, our Q4 can be quite volatile given the variability of winter weather and consumer demand dynamics during the holiday season, as well as potential impacts this year from the November election.”

- Columbia Sportswear ($4.6B, Apparel Manufacturing): “Q3 financial results reflect a continuation of the trends we’ve experienced all year. The North American outdoor marketplace remains challenged, and we are working to maximize sales in a soft consumer demand environment. Looking across the global marketplace, there are many external risks and uncertainties: outdoor industry and U.S. consumer headwinds, weather, geopolitical conflicts, supply chain disruptions, and the upcoming U.S. elections. These factors, among others, have the potential to impact consumer demand and our operations. With this uncertainty in mind, we are reducing our net sales outlook to reflect a 3% to 5% decline this year [versus 2% to 4% previously]. While we are not providing any full year 2025 guidance at this time, our objective is to deliver net sales growth and operating margin expansion. We will provide our next update on 2025 when we report in February.”

- Leggett & Platt ($1.6B, Furnishings, Fixtures & Appliances): “Our Q3 sales and earnings were below our expectations, largely due to weaker than anticipated demand in residential end markets and headwinds in automotive, hydraulic cylinders, and geo components. Sluggish demand in these businesses is expected to persist through Q4 and is expected to be more impactful than previously anticipated. As a result, we are reducing full year sales and earnings guidance. While we are encouraged to see the Fed begin a cycle of interest rate cuts, we know a series of cuts is needed to meaningfully impact housing turnover and there will also be a lag between improvement in housing trends and an improvement in mattress demand.”

- General Motors ($58.9B, Auto Manufacturers): “We have been able to grow our retail market share in the U.S. with above-average pricing, well-managed inventories, and below-average incentives. Now, with our strong Q3 results, we expect our full year EBIT-adjusted to be in the range of $14B to $15B, and EPS diluted-adjusted to be in the range of $10.00 to $10.50, both at the upper end of our previous guidance. And we are once again raising our adjusted automotive FCF.”

- Newell Brands ($3.7B, Household & Personal Products): ”EPS was at the high end of plan, driven by strong operational performance. We reduced Newell’s cash conversion cycle versus year-ago and we significantly de-levered the balance sheet to under 5.0x. The strong performance in the first nine months of 2024 gives us confidence to once again raise our outlook for the full year.”

- Brinker International ($4.6B, Restaurants): “Chili’s comps came in at positive 14.1%, driven by price of 6.8%, positive mix of 0.8%, and positive traffic of 6.5% with traffic improving sequentially throughout the quarter. These impressive results were driven by the continued success of our marketing campaigns on both TV and social media, highlighting our industry leading ‘Everyday 3 for Me’ value and our popular Triple Dipper appetizer. October comp sales to date for Chili’s remain in the double digits with positive traffic, and we continue to increase our gap to the casual dining industry. In terms of our expectations for the balance of the year, as noted in this morning’s press release, we’re raising our fiscal 2025 full year guidance.”

Affordability Challenges Continue to Weigh on Housing and Auto amid Uncertain Interest Rate Backdrop; Restaurants See Traction with Value Offerings

- Whirlpool ($5.7B, Furnishings, Fixtures & Appliances): “Demand in the U.S. has shifted significantly toward lower margin replacement-driven purchases, and the higher margin discretionary demand continues to be weak due to historically low existing home sales. Although the timing of the U.S. housing recovery is still uncertain, we are confident that the industry will have a multiyear recovery with the underlying housing fundamentals remaining strong.”

- D.R. Horton ($58.8B, Residential Construction): “We are seeing our buyers sit on the sidelines, sit on the fence, and a little less motivated today than they were previously in prior quarters. And affordability has been challenged. I don’t think this is a structural issue with demand. There’s just a lot of noise in the market today. With the rate volatility we’ve seen, combined with the election news that’s out there, we’re seeing people take a pause.”

- General Parts Company ($16.7B, Auto Parts): ”The weaker demand environment continues to be impacted by interest rates combined with persistent cost inflation and election and geopolitical uncertainty. These factors are impacting our customers, most notably with tightened budgets and reduced spending for capital projects in our Industrial business, and reduced spending in general maintenance and discretionary categories across our Automotive segment. We continue to hear from customers considering capital projects that they are pausing, not canceling, these plans until they have better visibility into the interest rate environment and the outcome of the election in the U.S.”

- Lear Corporation ($5.3B, Auto Parts): “Currently, macro conditions, including vehicle affordability, the regulatory environment and wage inflation continue to weigh on the automotive industry. The unprecedented transition to electric vehicles has caused near-term uncertainty around vehicle production. As customers assess their powertrain strategies, we have seen a delay in sourcing activity, particularly in North America and Europe.“

- Sonic Automotive ($2.0B, Auto & Truck Dealerships): “Elevated used retail prices remain a challenge for consumers, contributing to affordability concerns amid the current interest rate environment. However, the return to normal seasonal trends in used vehicle wholesale pricing are positive for our business outlook and, when combined with potential further interest rate cuts, should begin to benefit affordability and used vehicle sales volume in 2025.”

- Polaris ($4.0B, Recreational Vehicles): “Consumers remain cautious with discretionary spending, especially for larger purchases, and it will likely take more interest rate cuts and time to improve the financial position before spending returns on pre-pandemic levels.”

- McDonald’s ($209.9B, Restaurants): “[Our U.S. business] has significantly outperformed the QSR industry with comp guest count and traffic gaps at their highest point since the beginning of 2023. The $5 meal is doing exactly what we had set out to have it achieve. For the first time in over a year, we gained share with lower-income consumers. And we also saw that customers that were buying that $5 meal were visiting us more frequently. We ended Q3 on an upward trajectory in the U.S. business. So, a really strong finish to the end of Q3 and start to Q4 when you consider we were still operating in a very challenging broader industry context.”

“Judicious” Spending Patterns Seen Punctuated by Pullback on Big-ticket Items; Bifurcation Still in Focus with Higher Income Cohorts Driving Spend While Lower Income Consumers Face Increased Pressure

- O’Reilly Automotive ($68.43B, Specialty Retail): “In our view, the average consumer is still reasonably healthy, but we believe is exhibiting an element of caution when managing their pocketbook in an environment of uncertainty surrounding price levels, macroeconomic conditions, and an upcoming election.”

- McDonald’s ($209.9B, Restaurants): “The consumer is certainly being very discriminating in how they spend their dollar, and the inflation that has occurred over the last couple of years in the U.S. has certainly created that environment. While it may be more pronounced with the lower income consumer, it’s important to recognize that all income cohorts are seeking value.”

- General Motors ($58.9B, Auto Manufacturers): “With respect to credit, our charge-offs YTD at GM Financial are almost spot on what we expected. We did expect a modest moderation in credit YoY, and that’s exactly what we’re seeing. Our portfolio is heavily prime, and the prime credits have continued to perform very strongly with good employment levels, good household income, and still pretty strong household balance sheets. All in all, credit is developing very much in line with what we expected.”

- Tractor Supply ($29.0B, Specialty Retail): “I would describe the sentiment of our customer as relatively stable as supported by the recent jobs report and the current unemployment rate of 4.1%. Consistent with prior quarters, our consumer continues to be judicious with their spending, focused on innovation, newness, and needs-based products. YTD through Q3, the macro retail environment is running in line with the subdued expectations that we had as we entered the year.”

- Newell Brands ($3.7B, Household & Personal Products): “We are seeing a market bifurcation and consumer dynamics between low income versus higher income At lower income levels, there has been a significant decrease in unit volume compared with pre-pandemic levels, as these households are prioritizing spending on basic needs like food, rent, and insurance due to the cumulative impact of inflation outpacing wage increases. Conversely, the higher income households have increased spending significantly in both units and dollars, as these consumers are benefiting from home price appreciation and stock market gains. With higher income consumers driving the market, we are seeing stronger demand for more premium price products that represent a good consumer value.”

- Harley Davidson ($4.2B, Recreational Vehicles): “Overall, we continue to see greater spend from higher than lower income customers, as evidenced by motorcycle mix, where our CVO motorcycles continue to be up double-digit percentages throughout the year. In Q3, the global consumer has seemingly taken a pause from big-ticket consumer discretionary spend based on different dynamics in each region.”

Amid Challenging Top-line Environment and Competitive Pricing, Companies Highlight Operational Efficiency and Cost Management Efforts

- Garrett Motion ($1.7B, Auto Parts): “We find ourselves in a softer top-line environment. But the team delivered excellent operational performance, which translated into an adjusted EBITDA margin of 17.4%, a 160 bps increase compared to Q3 last year. Consistent operational execution in line with our financial framework allowed us to continue to increase margin this year as we flex our variable cost structure and implement sustainable fixed cost actions while still investing in new technologies.”

- General Motors ($58.9B, Auto Manufacturers): “The competition is fierce, and the regulatory environment will keep getting tougher. That’s why we’re focused on optimizing our ICE and EV margins. It all begins with our stellar ICE portfolio, where we’ve been able to maintain strong pricing compared to the industry, and our highly profitable full-size pickup and full-size SUVs continue to gain market share in their respective segments. We’ve been able to achieve these market share gains with significantly lower incentives than our competitors. This demonstrates the strength of our products and our disciplined go-to-market strategy.”

- PulteGroup ($25.9B, Residential Construction): “The gross margin is an important driver of ROIC, and we don’t want to give away lots that we’ve worked hard to secure. At the same time, we must be price competitive and offer a clear and compelling value to potential home buyers. Our Q3 results show this balancing act as we continue to generate historically high gross margins, but with meaningfully increased incentives in response to the more competitive market conditions in which we’re currently operating.”

- O’Reilly Automotive ($68.43B, Specialty Retail): “We would still characterize the acquisition cost environment as stable and would anticipate seeing a mix of both incremental cost improvements and modest inflation pressure as we finish out 2024. These cost dynamics are coupled with a pricing environment that remains rational across our industry.”

- McDonald’s ($209.9B, Restaurants): ”We still have pretty muted top-line growth, which is going to put pressure on margin from a percentage standpoint, because we still have cost impacts that are hitting the business. If you use the U.S. as a specific example, we’ve got just above mid-single-digit wage pressure, in large part from the more significant increases in California earlier in the year. In terms of pricing power, you’ve heard us talk a lot about the more challenging environment, particularly in our international markets. We still feel we can get pricing, but that is going to be at more conservative levels until we get the right momentum back in the business in each and every one of our markets.”

- Mohawk Industries ($8.6B, Furnishings, Fixtures & Appliances): “We remain focused on managing the controllable aspects of our business to enhance our results with gross margins under pressure from weaker industry demand. All of our businesses are implementing strategies to maximize volume and plant utilization. Our teams are executing the $100M of restructuring initiatives that we announced last quarter. Our businesses are making additional cost reductions in SG&A, operations and logistics. These actions will continue throughout next year to achieve our planned savings.”

Consumer Headwinds Persist in Europe; China Weakness Seen Continuing Near Term; India Remains a Key Growth Market

Europe

- General Parts Company ($16.7B, Auto Parts): “Starting in Europe, during Q3, overall market growth remained muted, down low single digits, which was consistent with Q2. The weak economic backdrop in Europe is being driven by an elevated level of deferred maintenance attributable to real wage declines, unemployment, higher interest rates and uncertain political and geopolitical situations. As we look at the economic backdrop in three key European markets, Germany, France and the UK, higher interest rates continue to negatively impact consumer purchasing power. Furthermore, higher unemployment rates and real wage declines in France and Germany have contributed to softer spending at the consumer level.”

- Ebay ($30.6B, Internet Retail): “In the UK and Germany, we continued to navigate more challenging macroeconomic condition and lower consumer confidence, while seeing strength in parts and accessories and improved trends in C2C volume.”

- Sketchers U.S.A ($9.4B, Footwear & Accessories): “We saw marked improvement in several of our international businesses, particularly in Europe, where our mitigation strategies to address supply chain delays bore fruit.

China

- Crocs, Inc. ($6.5B, Footwear & Accessories): “It is clear that the Chinese consumer is being far more conservative in their purchase behavior, and we’ve seen an even more pronounced pullback within key Tier 1 cities like Shanghai and Beijing. In light of the broader macro environment in China, we are taking a more cautious view for the rest of the year. Despite this backdrop, our brand continues to gain share in China, which we believe is a direct result of our accessible, authentic brand positioning, serving as a meaningful, competitive advantage.”

- VF Corp ($8.8B, Apparel Manufacturing): “You’re reading the same things we are in China. We have so much in our control that I’m not too worried about macro But it is true, the macro in China is a little softer than it has been.”

- Sketchers U.S.A ($9.4B, Footwear & Accessories): “Let me address the market in China, where macroeconomic pressures and its impact on the consumer are well-documented. Sales declined 5.7% YoY, which was below our initial expectations for the quarter. Our talented local team has responded by adjusting our near-term plans to navigate the uncertain situation, and we have modest expectations for the balance of the year, including Singles’ Day. Over the years, we have built an incredible brand in China and remain confident and optimistic about the long-term opportunities for Skechers in this market.”

APAC ex-China

- General Parts Company ($16.7B, Auto Parts): “The macro environment is also challenging in [Asia Pac], with Australia experiencing the weakest economic growth in nearly three decades and New Zealand currently in its second recession in 18 months. However, our teams are executing well, extending our industry leading position and taking market share.”

- Crocs, Inc. ($6.5B, Footwear & Accessories): ”In addition to China, we’re confident around India. We have a very attractive business model in India that has been impeded recently with the BIS. The Indian government has been imposing some restrictions associated with the need to make your products in India. We will have production up and running for both Crocs and HEYDUDE in India next year. It started this year, but it will reach enough supply to fund the market next year, so we’re confident about India.”

- Sketchers U.S.A ($9.4B, Footwear & Accessories): “In contrast to [China challenges], ..saw a rebound in India, where the continued collaboration between our local team, suppliers and regulators led to a meaningful turnaround from last quarter’s results. Demand for our product is strong, and we will continue to invest in this important market.”

- Whirlpool ($5.7B, Furnishings, Fixtures & Appliances): “We recently expanded our offering with a majority stake in Elica of India in 2021, and we just started the production of frontload washers in India, and we want to continue to invest in this business.”

In Closing

Executives maintain a largely cautious tone amid elevated macro uncertainty and a continuation of trends around discerning consumer spending patterns. The challenging demand environment has persisted longer than expected for many, with Consumer Discretionary companies lowering revenue guides at a much higher propensity than the broader U.S. equity market. With top lines under pressure, companies are leaning into operational efficiency and cost controls, managing through this choppy environment to position themselves for future growth in anticipation of an eventual demand recovery.

We will continue to monitor these trends and more as we seek to support you, our valued clients, and as we work through the quarter and the rest of the year.

- As of 8/1/24