With Q3 2023 earnings season in the books, we “Close the Quarter” with some notable themes:

Overall Performance

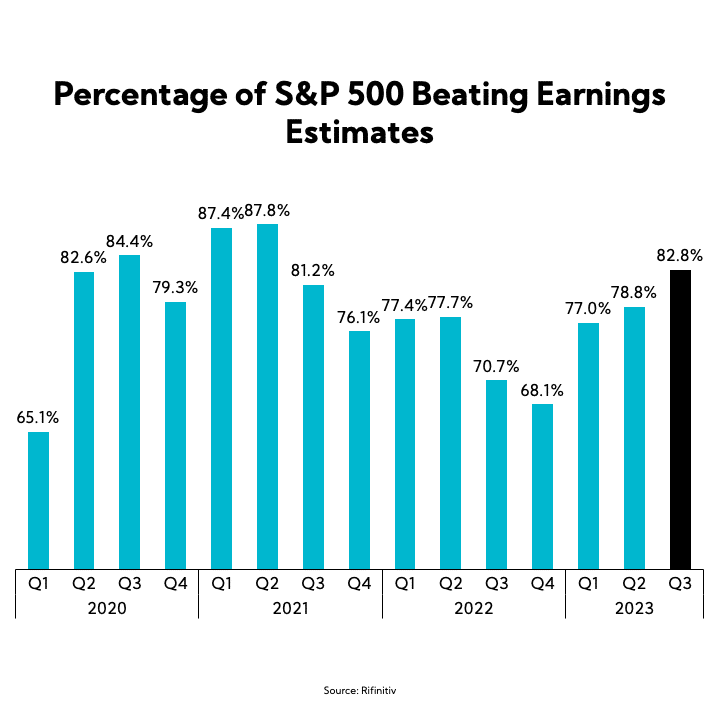

Stronger-than-expected S&P 500 Q3 EPS prints (~83% beat vs consensus) result in more than half of companies seeing estimate increases through the end of the year, while roughly one-third experience revenue expectation cuts despite 60% beating consensus.

Consensus Trends

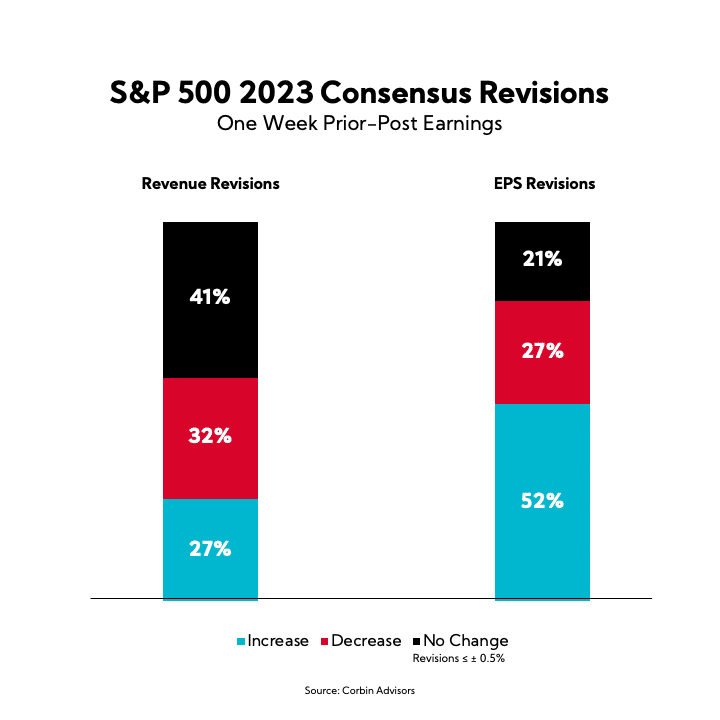

Revenue: 27% increase, 41% no change, 32% decrease

EPS: 52% increase, 21% no change, 27% decrease

Guidance

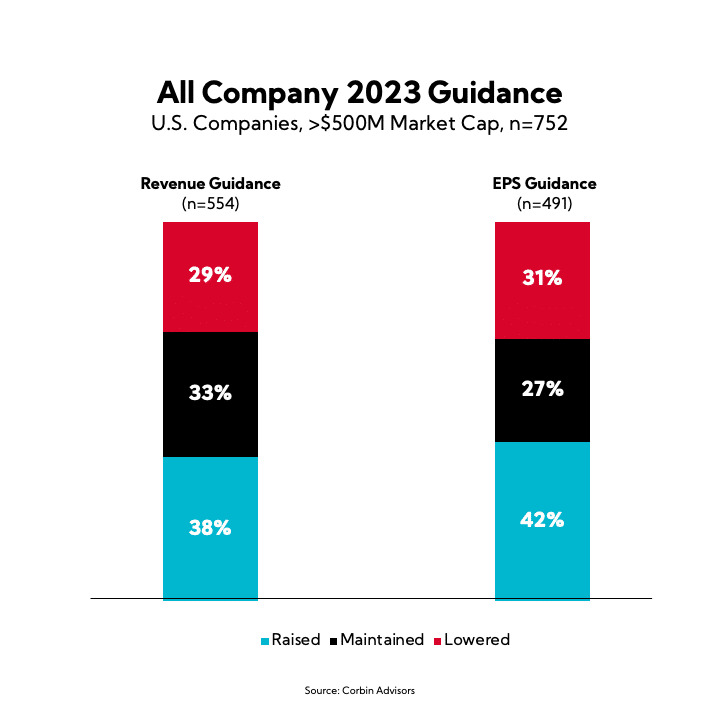

Based on a universe of over 750 companies we track every quarter, more companies raised guidance versus maintained or lowered, with EPS seeing a slightly higher number of increases over revenue.

Guidance Shifts

Revenue: 38% raised, 33% maintained, 29% lowered

EPS: 42% raised, 27% maintained, 31% lowered

Capital Allocation

Sequential cash uses indicate renewed interest in buybacks and M&A, though both increases continue to be overshadowed by their negative YoY comparisons.

S&P 500 Sequential Uses of Cash

+12.8% buybacks

+12.0% M&A

1.9% capex

+0.9% dry powder

-0.9% debt paydown

-3.6% dividends

Earnings

Stronger-than-expected Q3 EPS prints result in consensus raises through the end of the year, while roughly one-third cut revenue expectations.

Guidance

More companies across the broader U.S. universe are raising annual EPS guidance than they are revenue for 2023, though both metrics saw the majority of companies increasing. Still, roughly 30% decreased top- and/or bottom-line guides through Q3.

Corbin Advisors is a strategic investor relations and investor communications advisory firm with a track record of supporting our publicly traded clients in creating sustained shareholder value. Our approach leverages decades of Voice of Investor® (VOI®) research and data-driven insights; capital markets expertise and deep best practice knowledge; and a proven playbook and passion for client outperformance. We are a trusted advisor and partner to boards of directors, executive leaders, and investor relations professionals, serving a broad range of companies globally across sectors, sizes, and situations. Through defining the standard of excellence and challenging conventional thinking, we enable our clients to boldly differentiate their equity brand, maximize valuation, and build more durable franchises.