Commencing the Quarter – Q1’26

15 min. read

This week, our Thought Leadership commences the quarter and covers:

- Key Events this week

- Q1’26 Earnings Communication Summary, based on a review of earnings reports to date

Key Events

Iran War Entering Second Month

- Launched in late February, what started as a combined air campaign by the U.S. and Israel against Iran has shifted to an expanding regional conflict with limited visibility toward a resolution.

- With limited ability to engage in effective counterattacks against U.S. and Israeli forces, Iran has instead targeted key oil and energy infrastructure in the region. This resulted in the closing of the Strait of Hormuz, a critical waterway that handles ~20% of global oil supply.

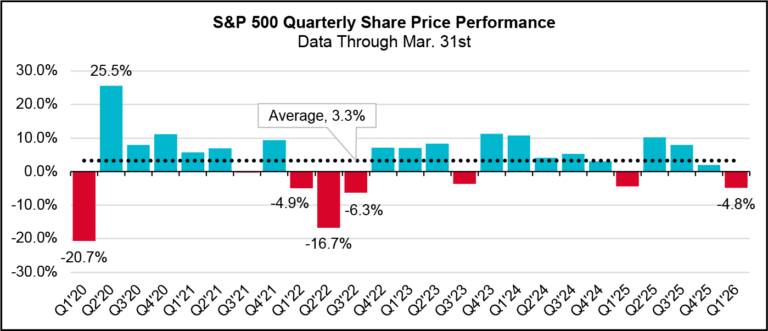

- Since hostilities began on February 28, the S&P 500, Dow Jones Industrial Average, and NASDAQ are all lower by 7.4%, 7.8%, and 6%, respectively.

- Stocks have trended higher during the waning days of March, as statements made by President Trump reflect a desire to conclude operations in 2 to 3 weeks.

- While the risk to oil supply has dominated headlines (Brent is up ~45% since Feb. 28), other regionally exposed commodities are also seeing upward pricing pressure due to supply fears. Urea, a common ingredient in nitrogen-based fertilizers, has increased by 45% since the conflict began.

Margaret Ryan, Director of the SEC’s Division of Enforcement, Resigns

- On March 16, ~6 months into her tenure as Director, the Commission announced Margaret Ryan’s resignation from the agency. Ryan reportedly “wanted to be more aggressive in pursuing charges for fraud and other misconduct, including in cases that touched the president’s circle,” yet faced resistance from SEC Chair Paul Atkins and other top Republican political appointees in doing so. (Source: U.S. Senate Committee on Banking, Housing, and Urban Affairs)

Manufacturing PMI

- The ISM’s purchasing managers index was 52.7 last month, versus 52.4 in February. Readings above 50 indicate a sectoral expansion. Analysts polled by The Wall Street Journal were expecting a reading of 52.1. (Source: WSJ)

- Tariffs continue to negatively impact new export sales, and growth was principally driven by higher domestic demand. (Source: S&P Global)

Q1’26 Earnings Communication Digest

Every quarter, we analyze earnings communications from off-cycle companies reporting over the past month to identify key themes and emerging trends across market caps and sectors. We have included updated examples of investor communications on the potential impact and actions as it relates to the Iran War.

We entered 2026 with markets navigating a complex and evolving macro backdrop. As noted in our Q4’25 Closing the Quarter publication, investor sentiment revealed a generally positive outlook for 2026, as optimism surrounding rate cuts, continued earnings momentum, and productivity gains outweighed concerns with elevated valuations, policy risks, geopolitical worries, and growing concerns of an AI bubble.

This optimism proved short-lived amid the entry of a black swan – the Iran War – with fallout from the ongoing geopolitical conflict causing a sharp increase across commodities, higher equity risk premiums, yields climbing to levels not seen since Liberation Day, and the largest sequential decline in the S&P 500 in nearly four years.

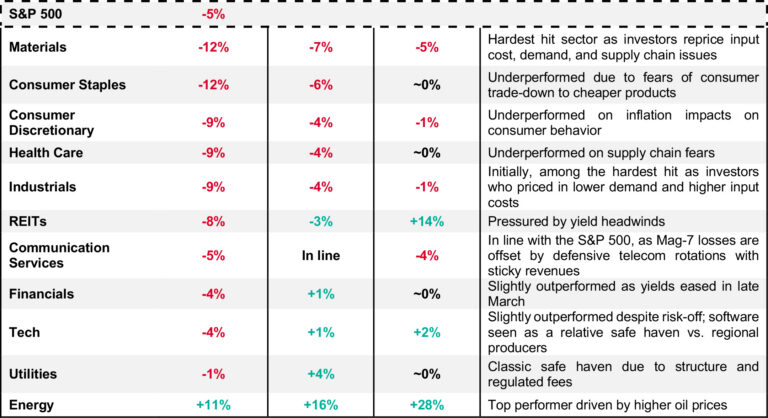

Iran War Market Reaction

Sector Impact

Data as of 2’27’26 – 3’31’26

Multiple Compression

2’27’26 – 3’31’2026

Earnings Summary and Key Themes

Across sectors, companies are navigating a now highly uncertain geopolitical environment and uneven macro, where persistent inflation, evolving tariff dynamics, dislocated equity markets, and war are limiting visibility, elevating costs, and yielding a more cautious tone than what was heard last quarter. Across earnings calls in the last several weeks, executives highlighted tightening constraints in raw materials, worsening logistics bottlenecks, and rising input costs, particularly in chemicals and industrials, where disruptions to feedstocks and shipping routes are already evident. At the same time, many companies emphasized the potential for second-order effects, namely higher inflation, higher-for-longer interest rates, and softening demand, suggesting that even a short-lived conflict could have prolonged economic consequences as supply chains take time to normalize.

Companies describe a consumer environment characterized by persistent inflation, cautious spending, and heightened sensitivity to everyday costs. Consumer-facing companies note demand remains intact but increasingly fragile and value-oriented, with lower- and middle-income consumers, the “Bottom-of-the-K”, continuing to trade down. Meanwhile, housing and discretionary categories continue to face ongoing affordability constraints, as higher material, labor, and financing costs weigh on activity. Despite this, some pockets of resilience remain, particularly among higher-income consumers and in experiences, though even these segments are being more closely scrutinized for signs of softening, as the “Top-of-the-K” endures a dislocated, roller-coaster equity market yielding losses.

Importantly, companies are not broadly pulling back on investment. Capital allocation strategies remain largely intact, with continued emphasis on long-term priorities such as AI, automation, and supply chain resilience. Large-scale capex plans in semiconductors and infrastructure persist, while consumer and industrial companies are leaning into productivity and efficiency initiatives to offset cost pressures. At the same time, some companies, particularly in consumer discretionary, are balancing these investments with shareholder returns, including accelerated buybacks, signaling confidence in longer-term fundamentals despite near-term uncertainty.

On tariffs, companies are taking a pragmatic approach. Most expect tariff impacts to remain steady despite policy changes, relying on well-established mitigation levers such as supplier diversification, pricing adjustments, and product redesign. Not surprisingly, across the board, companies continue to accelerate the adoption of AI, with a growing focus on demonstrable ROI, including efficiency gains, cost savings, and improved customer experiences.

Key trends from our analysis of off-cycle earnings calls include:

Iran Conflict

Companies Are Discussing the Immediate Disruptions to Rising Energy Prices and Constrained Materials Supplies While Also Monitoring Second-Order Effects

- Lennar ($23.1B, Household Durables): “It goes without saying that the war in the Middle East is a wildcard.It might end quickly and the world is a better and safer place or it might trigger higher gas prices, higher inflation and higher interest rates and we’ll just have to wait and see.”

- Costco ($428.4B, Consumer Staples Distribution & Retail): “We’ll have to see how things play out with the situation in the Middle East. But certainly, as we look at what happened during the second quarter for us, fresh food and sundries really drove the lower inflation overall. We’ve seen deflation in produce, eggs, butter, cheese, some of these commodities.”

- FedEx ($84.9B, Air Freight & Logistics): “With regard to the Middle East, our outlook assumes a modest headwind tied to business impact in the region, and we’ll continue to monitor the situation.As a reminder, also embedded in our assumptions is the continued revenue and profit headwinds from global trade policy changes, which are more than offset by transformation-related savings.”

- MillerKnoll ($1.3B, Commercial Services & Supplies): “With respect to the Middle East, this region remains an important long-term growth opportunity for our international contract business. In the near term, the current conflict is creating disruption, and we do expect some impact to fourth quarter sales and costs.”

- H.B. Fuller ($2.8B, Chemicals): “Now let’s turn to the developing supply chain impact resulting from the conflict in the Middle East and its implications for our business. This conflict is already creating significant constraints on raw material availability with impacts that extend across feedstocks, intermediates, logistics lanes, and energy inputs. We have received over 40 force majeure letters from suppliers in recent weeks, clear evidence that this is a major disruption. Chemical production capacity has decreased significantly, and tanker routes have been disrupted and repositioned. Even if this conflict were resolved tomorrow, we would expect supply chain aftershocks to persist throughout the year as inventories rebalance, transportation and logistics normalize, and plants work through restart cycles.”

Macro Backdrop

Rising Energy and Raw Materials Foreshadow Increased Inflationary Pressure and May Hamstring Fed in Easing Rates, a Key Driver for Consumer Discretionary and Housing Related Names; Consumer Companies Continue to Cut Costs While Consumer Pressure Compounds

- Five Below ($12.7B, Specialty Retail): “The state of the consumer and the macro environment in which we’re operating…we just don’t think it gets easier from here, whether it’s the prices at the pump or this sticky inflation that seems to be hanging around, or a job market that is somewhat sluggish. We think the environment here is going to continue to be challenging.”

- Dollar General ($27.6B, Consumer Staples Distribution & Retail): “Consumers really need a Dollar General at this point as we look ahead with all of what’s ahead of that consumer, including the macroeconomic pressures that are out there and the geopolitical pieces that we’re all watching very closely.”

- Carnival ($35.3B, Hotels, Restaurants & Leisure): “Now what stands out most is that we’re achieving all of this against such an unpredictable macroeconomic and geopolitical backdrop. It says a great deal about the demand we continue to see across our portfolio of world-class cruise lines, about the team’s ability to execute on our long-term strategy and about the progress we’ve made in positioning the business to perform through a wide range of environments. This start to the year also supports increasing our full-year outlook operationally by approximately $150M compared to our December view. That improvement helps absorb a $500M fuel headwind.”

- Paychex ($33.5B, Professional Services): “On the macro side, what we’ve said and what we see is that it’s been relatively stable. It’s really a low fire and a low hire type of environment right now.We’ve not seen a significant change in this fiscal year in terms of the small business index that we report. And we’re in a dynamic environment right now where what we hear from clients, particularly in the small end of the market, less than 50, is a continued inability to find qualified people for the jobs that they have open, and we’re doing a lot of things to try to support them there. And then you’ve got a degree of potential hesitancy to add in this uncertain environment as you move upmarket.”

- Macy’s ($4.7B, Broadline Retail): “For our guidance, we are taking a prudent approach, giving ourselves flexibility to respond to changes in the competitive landscape and external environment as well as macroeconomic and geopolitical unknowns.”

- Academy Sports & Outdoors ($3.4B, Specialty Retail): “Our belief is that most of the macroeconomic pressures that consumers faced in the back half of ‘25 will carry into the 1H26. In particular, inflationary pressures on goods sourced outside of the U.S. should continue through the first half of the year.”

- KB Home ($3.3B, Household Durables): “Although market conditions remain challenging, we are focused on the appropriate levers to drive improved results, renewing our focus on built-to-order, reducing our build times, lowering our costs, opening new communities, and staying balanced in our capital allocation.”

- General Mills ($19.9B, Food Products): “Through our Holistic Margin Management productivity program, we remain on track to generate 5% gross savings in our cost of goods sold in FY26, driven by our digital advancements within our supply chain, particularly in logistics and manufacturing. And we continue to expand the impact of our multiyear enterprise global Transformation initiative. Combined, these and other efficiency efforts are expected to contribute $600M in total savings this fiscal year, extending our long track record of rigorous cost discipline.”

Capital Allocation

Capex Story Remains Intact Despite Iran War and Rising Yields; AI Investments and Upgrading Supply Chain Resiliency Remain Strong Secular Trends While Consumer Discretionary Companies Favor Buybacks

- Micron Technology ($456.0B, Semiconductors & Semiconductor Equipment): “We expect FY26 CapEx to be above $25B. We project our FY27 CapEx to step up meaningfully to support HBM- and DRAM-related investments. We expect construction-related CapEx to increase by over $10B YoY in fiscal 2027as we build out our global manufacturing sites to address long-term demand opportunities. In addition, we expect higher equipment spend YoY in FY27. As we make these investments, we will continue to be responsive to the market environment and our customer demand to appropriately align our supply plans.”

- Kroger ($44.6B, Consumer Staples Distribution & Retail): “Beyond new stores, our capital investments will support technology and AI, where we are investing aggressively. These investments serve 2 purposes: improving the customer experience and driving productivity throughout the company. This year, we’re introducing agentic AI shopping for our customers, which will help them discover items, build baskets, plan meals, and stay within budgets, all in a personalized way. We’re also investing in supply chain modernization with more automation and expanded capacity. And we’ll also continue investing in our remodels to ensure our stores deliver a consistently strong experience.”

- Oracle ($443.9B, Software): “Investing in the AI infrastructure is capital-intensive, but our operating model is optimized to ensure profitability. Flexible infrastructure design, high utilization, and rapid handover, combined with diversified customers, create an incredible business. Increased scale spreads our fixed costs over a larger base, increasing profitability. It’s unprecedented to scale a capital-intensive business so quickly while also increasing profitability.”

- Smithfield Foods ($9.3B, Food Products): “Our targeted capital spend for 2026 will be in the range of $350M to $450M. In addition, subject to permitting and other approvals, we expect to invest up to $1.3B over the next 3 years to construct the new state-of-the-art Packaged Meats and Fresh Pork processing facility in Sioux Falls.”

- Ross Stores ($68.9B, Specialty Retail): “As noted in today’s release, we repurchased 1.5 million shares during the quarter, completing the 2-year $2.1B program announced in March 2024, in line with our plans. Our Board…recently approved a new 2-year $2.55B stock repurchase authorization. This new plan represents a 21% increase over the recently completed repurchase program.”

- Ollie’s Bargain Outlet Holdings Inc ($5.8B, Broadline Retail): “We bought back $34 million worth of our common stock in the quarter and $74 million for the full fiscal year. At year-end, we had $259 million remaining under our current share repurchase authorization. We are stepping up the buyback in 2026.”

Tariff Developments

Companies Largely Expect a Steady Impact from Tariffs Despite the IEEPA Ruling as Other Tariffs Likely to Replace IEPPA Currently in Effect; Expect Q&A Centered on Potential for Tariff Refunds

- Ollie’s Bargain Outlet ($5.8B, Broadline Retail): “The tariff situation obviously remains very fluid, and the current lower levels could be temporary. Bigger picture, tariffs are just another form of disruption, and we benefit from disruption. Whatever happens, we would expect to mitigate any margin pressure from tariffs.”

- Costco ($428.4B, Consumer Staples Distribution & Retail): “Regarding IEEPA tariff refunds, it is not yet clear what the process will be, what refunds, if any, will be received, and when this will happen. Throughout the past year, we’ve taken action to reduce the impact of tariffs. In many cases, we didn’t pass the full cost on to our members. The complexity of the tariffs implemented over the past year, including layering of different tariffs on top of each other and multiple changes in rates throughout the year, also made it challenging to track the exact impact to an individual item sold.”

- Dollar Tree ($21.4B, Consumer Staples Distribution & Retail): “We also navigated meaningful cost volatility this year. Tariff expense increased substantially YoY. As we’ve discussed, we continue to actively deploy the five mitigation levers we’ve historically used to manage cost headwinds, including supplier negotiations, product re-engineering, country of origin shifts, assortment adjustments, and targeted pricing actions, all to maintain strong profitability, while preserving value for our customers.”

- Lennar ($23.1B, Household Durables): “Traffic has remained reasonably consistent across our communities, but the urgency to transact remains measured. At the same time, a combination of tariffs and immigration issues are keeping upward pressure on material and labor costs and are pushing overall costs higher. With affordability at stake, we have been working hard to push against and to manage these pressures through our trade partner relationships and through the efficiencies we have built into our manufacturing model and our product. Nevertheless,the cost structure in the industry is pushing higher and is difficult to manage.”

- MillerKnoll ($1.3B, Commercial Services & Supplies): “From a tariff perspective, we don’t expect the most recent developments to result in any meaningful changes to our approach, and we expect to continue to fully offset tariff costs for the remainder of this fiscal year as we did in the third quarter. Recognizing that things can develop quickly, however, we are very experienced in navigating tariff changes and continue to monitor both policy and rates closely.”

- Winnebago ($1.0B, Automobiles): “The recent decision by the Supreme Court on IEEPA…are still being evaluated. I do not expect that transition from IEEPA to Section 122 to have a material impact on our margin story or on pricing. I think that they will largely offset each other, if not even be a little bit favorable, but that is something that we’re monitoring very closely.”

- Nike Inc ($78.0B, Textiles, Apparel & Luxury Goods): “While the tariff environment has been uncertain, assuming no significant changes, we expect the first quarter of fiscal ’27 to be the final quarter where higher tariffs continue to be a material year-over-year headwind to gross margin. We expect gross margin expansion to begin in the second quarter due to actions to mitigate tariffs and recovery of transitory impacts from Win Now.”

- Cintas ($72.5B, Commercial Services & Supplies): “It’s a dynamic environment on tariffs as well. But our supply chain team has done a magnificent job of navigating that. We’ve said in the past that we’re not immune to tariffs. But any increase in tariff or decrease in that is going to take time to run through our system, whether we have to get into our supply chain and then amortize that. So, I would say nothing material there to factor in.”

- AutoZone ($55.3B, Specialty Retail): “There’s lots of discussion about what’s going to happen with tariffs, and the IEEPA tariffs have been stayed at this point. That was a relatively small portion of our tariff bill, if you will, most of our tariffs are Section 232 tariffs. So, we’re still expecting to see tariff impact as we move through the back half of the year. I think the other dynamic is that we’ve talked about this notion of having a multi-pronged strategy here where we would continue to negotiate with our vendors, we diversify our sources, and then in some cases, we’ll raise our retails. All of the costs that we’ve seen so far from tariffs have not made its way through the system, which is why we’re expecting [in store average transaction price] to continue to be elevated through Q3 and Q4.”

The Bifurcated Consumer

Remains Strained at the Margins and Increasingly Value-driven as Oil Prices Eat into Discretionary Income; Low- and Middle-Income Households Continue to Trade Down

- Ross Stores ($68.9B, Specialty Retail): “The composition of our customer base seems to be very much intact. We’ve seen growth across essentially all pieces of it in terms of income levels, age, and different ethnicities. So, to tease out any minor differences, it would be kind of unnecessary. It’s been an overarching rising tide, I think, for essentially all customers.”

- Darden Restaurants ($22.6B, Hotels, Restaurants & Leisure): “From an income perspective, what we’re seeing is there is growth across all households with income above $50K, and the biggest growth is coming from households over $150K. That’s just generally what we’re seeing across all brands. As we look at Fine Dining, we’re seeing decent growth as you start to go above $150K as well, but $200K+ is where we’re seeing the most growth. And that’s where we see even bigger disparity between the below $75K, below $100K, and then the above…$150K.”

- Ollie’s Bargain Outlet ($5.8B, Broadline Retail): “In terms of the state of the consumer, consumers are seeking value, and we’re here for them. The strength we’re seeing in trade down has continued with our upper-income cohorts. There’s momentum there in trade down. The lower income — the lowest of our cohorts, a little bit weak. The trade down is more than offsetting the weakness in the lower-income cohorts. We’re also seeing strength in consumables, which is an indication of where the consumers’ mindset is. It’s continuing to be a very strong business for us.”

- Dollar General ($27.6B, Consumer Staples Distribution & Retail): “Customers across all income brackets continue to stress the importance of finding value as they shop, and we are meeting this need as we continue to grow penetration with households of all income levels. And while we continue to be pleased with our pricing position against competitors and other classes of trade, we know value is multifaceted, especially for our core customer.”

- Best Buy ($13.4B, Specialty Retail): “Consistent with the past several quarters, we expect to see a consumer who is still spending, but is value-focused and attracted to sales moments. Importantly, while customers continue to be thoughtful about big-ticket purchases, they are willing to spend on high-priced products when they need to or when there is technology innovation. We do expect consumers to spend a portion of their higher tax refunds at Best Buy, concentrated in Q1.”

- Smithfield Foods ($9.3B, Food Products): “In the short term, consumers are definitely stretched. The grocery and foodservice industry is seeing people spend less or trade down to less expensive items or items that deliver more value.”

AI Opportunity

Expect More Investor Scrutiny of ROI and Discussions of Specific Examples across Operations, Products, and Workflows

- Broadcom ($1.53T, Semiconductors & Semiconductor Equipment): “Consistent now with the strong outlook for our XPUs, demand for AI networking is accelerating. Q1 AI networking revenue grew 60% year-on-year and represented 1/3 of total AI revenue. In Q2, we project AI networking to accelerate a lot more and grow to 40% of total AI revenue.”

- Dollar General ($27.6B, Consumer Staples Distribution & Retail): “While we are still early in our AI journey, we are building an AI operating system for the enterprise, focused on reshaping our workflows to improve productivity and enablement. We believe that over time, these efforts can improve our customer-facing applications while accelerating our value delivery, decision automation, and continuous process improvement, lowering SG&A per unit of work, and driving efficiency in processes throughout the organization.”

- Chewy ($9.8B, Specialty Retail): “Across the broader organization, we are already deploying AI to drive greater structural efficiency. Functions such as customer service, fulfillment, pharmacy, and marketing operations are leveraging internally developed AI tools to streamline workflows and improve productivity. As we move through 2026, these efforts will translate into measurable financial impact. Based on our current roadmap, we expect AI-driven efficiencies to contribute a low tens of millions of dollars benefit in 2026 with a meaningful step-up in 2027, where we see a path to approximately $50M or more in annualized savings as these capabilities scale.”

- Worthington Enterprises ($2.4B, Machinery): “AI is now embedded across many of our applications, and our focus is shifting from experimentation to operational impact. Deploying AI in specific workflows where it can drive measurable efficiencies, not just individual productivity. We also continue investing in automation as we gain efficiencies and create elevated opportunities for our accounts.”

- Paychex ($33.5B, Professional Services): “Integral to our growth strategy, we continue to accelerate in embedding AI into our workflows. This amplifies our expertise with human-in-the-loop oversight and strong governance. We now have over 500 AI-powered capabilities and agents that can drive higher productivity, smarter decisions, and outcomes.”

- Kroger ($44.6B, Consumer Staples Distribution & Retail): “We see AI as a meaningful opportunity to both improve the customer experience and drive productivity across our business. We’re already seeing results from more competitive pricing, improved shrink, faster fulfillment, and tools that help our associates work more efficiently. As we move forward, we plan to expand these capabilities, including agentic shopping on our digital properties.”

- Docusign ($9.5B, Software): “We’re adopting AI across the organization, deploying new tools and enablement programs to boost productivity and gain efficiencies. The vast majority of our engineering organization is developing with AI, and 60% of new code is AI-assisted.”

- Lululemon Athletica ($19.0B, Textiles, Apparel & Luxury Goods): “We’re targeting meaningful savings as we simplify our operations and focus on scaling more effectively while continuing to invest in key growth initiatives. Key workstreams are increasing efficiencies across inventory management, supply chain and non-merchandise procurement, and reducing complexity while capitalizing on automation and AI opportunities.”

Updated Communication Examples

Building on our prior publication, Navigating Disruption: How the Iran War is Shaping Investor Discussions, below are additional examples of how companies are communicating actions and impact.

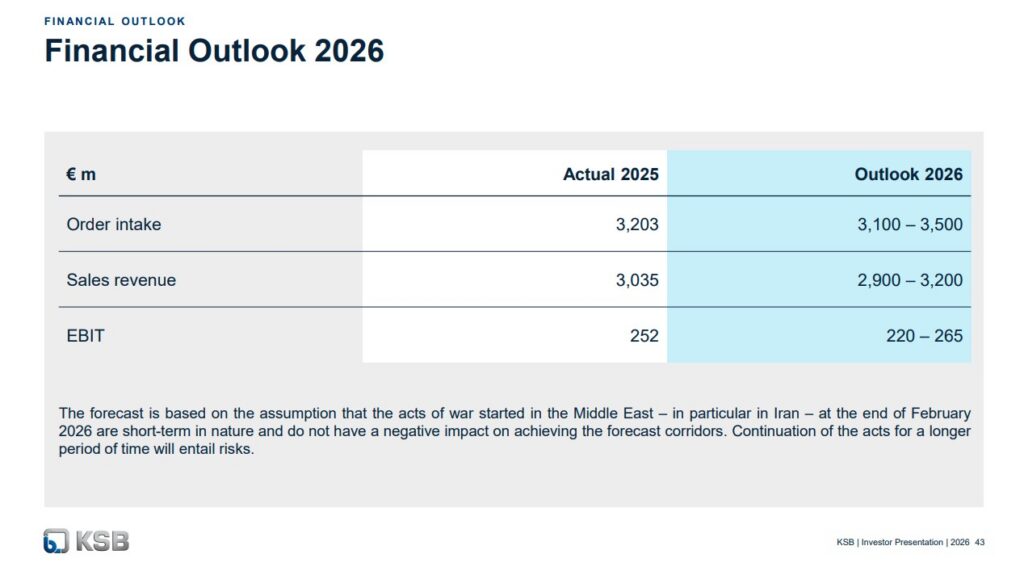

KSB Group ($1.4B, Industrials)

Embeds geopolitical scenarios into baseline planning, signaling a shift toward conditional outlooks rather than point estimates.

T1 Energy ($1.2B, Industrials)

Reframing as a structural tailwind for domestic investment, particularly in energy and infrastructure. Also positioning regional exposure as both a risk mitigant and a demand accelerator, where appropriate.

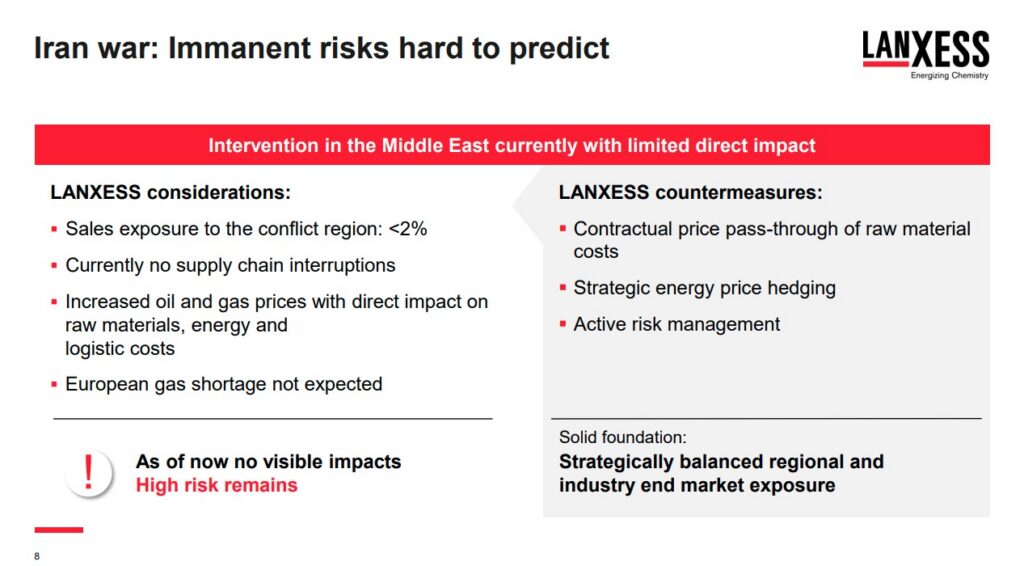

Lanxess ($1.8B, Materials)

With limited direct exposure, leaning into transparency and preparedness to reinforce credibility, emphasizing mitigation levers over the near-term impact.

Rheinmetall ($74.1B EUR, Industrials)

Explicitly positions geopolitical volatility as a driver of demand, signaling confidence in structural, multi-year tailwinds rather than cyclical uplift.

In Closing

The Q1’26 earnings season commences with a more cautious tone as geopolitical uncertainty and related fallout on the macro build. The Iran War is compounding risk, particularly around fuel, supply chain, and sticky inflation. So far, companies are adopting a wait-and-see approach, choosing to maintain the current course and scenario plan rather than make immediate changes.

To that end, companies continue to invest – in AI, productivity, and long-term growth – while actively managing costs, tariffs, and supply chains to protect margins. Overall, fundamentals are holding, but prudence is increasing.

We will be publishing our Q1’26 Inside The Buy-Side® Earnings Primer® next Thursday, April 9, 2026, providing insight into investor sentiment and expectations for the reporting period and more broadly.