Closing the Quarter – Q4’25

Closing the Quarter – Q4’25

Click here to download a copy

In today’s thought leadership, we cover:

- Key Events this week

- Closing the Quarter Summary – Q4’25 earnings performance, guidance moves and consensus shifts, AI, cost optimization, and capital allocation

Key Events

NVIDIA Reports Fourth Quarter and Fiscal Year 2026 Results Proving Continued Appetite

- The world’s largest publicly traded company continued to be the fuel behind the AI engine, reporting a beat on both the top and bottom lines. NVIDIA reported Q4 sales of $68B, up 20% YoY, while net income grew 35% to $43B. This reflected a positive surprise relative to analysts’ expectations of 3% and 15%, respectively. Despite the continued performance, persistent bearish talking points regarding customer concentration, revenue exposure to companies with fragile balance sheets, and circular financing arrangements remain. (Source: WSJ)

Initial Jobless Claims Up Modestly, Still Lower than Expected

- U.S. initial jobless claims increased modestly, with seasonally adjusted filings rising to 212,000 vs. expectations for 215,000. The marginal increase kept claims near levels consistent with a still-stable layoff backdrop. The 4-week moving average edged up to 220,250, while continuing claims fell to 1.83M for the week ended February 14. The report signals that churn remains contained even though labor markers cool at the margins. (Source: Dept. of Labor)

Takeaways from State of the Union

- Markets were broadly risk-on following President Trump’s first State of the Union address of his second term. During his nearly two-hour speech, President Trump focused on tax issues, demand incentives, trade policy, and AI-related power infrastructure. President Trump introduced plans to pursue deductibility of auto-loan interest on U.S.-made vehicles, a move that could steer demand and investment toward domestic OEMs. He also reiterated his tariff-forward posture, framing tariffs as a durable tool for both competitiveness and revenue. Finally, he addressed AI data-center electricity demand by reiterating a pledge by major tech firms to self-supply incremental power to avoid shifting costs to consumers, an important signal for hyperscaler and utility company capex.

Policy-by-Post

- February 23: President Trump criticized the recent Supreme Court ruling on tariffs – “The supreme court (will be using lower case letters for a while based on a complete lack of respect!) of the United States accidentally and unwittingly gave me, as President of the United States, far more powers and strength than I had prior to their ridiculous, dumb, and very internationally divisive ruling. For one thing, I can use Licenses to do absolutely ‘terrible’ things to foreign countries, especially those countries that have been RIPPING US OFF for many decades, but incomprehensibly, according to the ruling, can’t charge them a License fee – BUT ALL LICENSES CHARGE FEES, why can’t the United States do so? You do a license to get a fee! The opinion doesn’t explain that, but I know the answer! The court has also approved all other Tariffs, of which there are many, and they can all be used in a much more powerful and obnoxious way, with legal certainty, than the Tariffs as initially used. Our incompetent supreme court did a great job for the wrong people, and for that they should be ashamed of themselves (but not the Great Three!)… this supreme court will find a way to come to the wrong conclusion, one that again will make China, and various other Nations, happy and rich. Let our supreme court keep making decisions that are so bad and deleterious to the future of our Nation – I have a job to do.” (Source: Truth Social)

- January 23: President Trump indicated he may impose higher tariffs on countries he views as exploiting U.S. trade policy – “Any Country that wants to “play games” with the ridiculous supreme court decision, especially those that have “Ripped Off” the U.S.A. for years, and even decades, will be met with a much higher Tariff, and worse, than that which they just recently agreed to. BUYER BEWARE!!! Thank you for your attention to this matter.” (Source: Truth Social)

Closing the Quarter Summary

Heading into earnings season, our Q4’25 Inside The Buy-Side® Earnings Primer® survey, published on January 15th, revealed a generally optimistic outlook for 2026, but with outright bullish sentiment ebbing somewhat. Rate cuts, earnings momentum, and productivity gains drove favorable views, but enthusiasm was tempered by frothy valuations, policy risks, geopolitical concerns, and percolating AI bubble concerns. A majority of respondents, 50%, characterized their sentiment as Neutral to Bullish or Bullish, with nearly one-quarter Neutral to Bearish to Bearish. Nearly half, 45%, projected that 2026 U.S. GDP growth would be Higher than 2025, and most did not anticipate the U.S. economy would enter a recession within the next year.

All things being equal, investors continued to prioritize Growth over Margins, 64% to 36%, respectively, continuing the trend we saw in the prior quarter.

AI jumped to the top focus area for earnings calls, with investors seeking details on use cases, capex levels, and returns, followed by demand and growth trends, and rounded out by capital allocation.

With Q4’25 earnings largely in the books, we “Close the Quarter” with some notable themes:

1. Q4'25 Earnings Performance

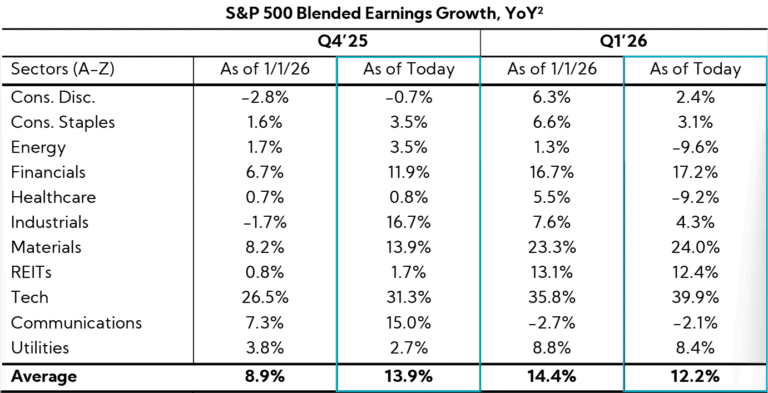

Companies Post Solid Results as Earnings and Revenue Growth Exceed Expectations; Q1’26 Revenue and Earnings Estimates Average 8.0% and 12.2%, Respectively, Indicating a Sequential Decline; Still, Q1’26 Revenue is Projected to be 300 Basis Points Higher YoY, a Good Sign for Underlying Demand with Many Assuming a Pick-Up in the Back-Half

Overall, S&P 500 revenue performance exceeded expectations in Q4, marking the highest revenue growth rate reported in three years. The YoY blended1 aggregate revenue growth rate stands at 8.8%, up from 7.3% estimated at the start of January and above the 6.6% estimate from early October. In addition, 72% of companies reported positive top-line surprises, modestly above the 5-year average of 70%, with results coming in 1.8% above consensus (versus the 5-year average of 2.0%). Looking ahead, Q1’26 blended revenue growth is expected to remain strong at 8.0%, albeit down from the acceleration seen over the past two quarters.

Q4 earnings also outperformed expectations. With over 85% of S&P 500 companies reporting earnings to date, the Index is on track to deliver YoY blended earnings growth of 13.9%, up from 8.9% at the start of January and well above the 7.7% estimate from early October. So far, 73% of companies reported a positive EPS surprise, below the 5-year average of 78%.

Forward estimates for Q1 have moderated, declining from 14.4% captured at the beginning of January to 12.2% today, primarily due to downward revisions in Healthcare, Energy, and the Consumer sectors. Conversely, Technology saw upward adjustments in aggregate earnings expectations.

2. Guidance Moves and Consensus Shifts:

More Companies Narrowed Revenue Guidance Ranges, While EPS Forecast Trended Wider; As for Consensus, Consumer Staples, Financials, Industrials, and Tech See the Highest Share of Positive Revisions, while Energy and Communications Receive the Most Downward Changes

Guidance Moves

We analyzed trends in annual revenue and EPS guidance across calendar-year companies within the S&P 500.3 Below are our findings.4

According to our Q4’25 Inside The Buy-Side® Earnings Primer®, investors expected 2026 guidance to reflect growth in both revenue and EPS, with ~60% anticipating guidance above 2025 actual results on both metrics.

Annual Guidance (YoY Trends)

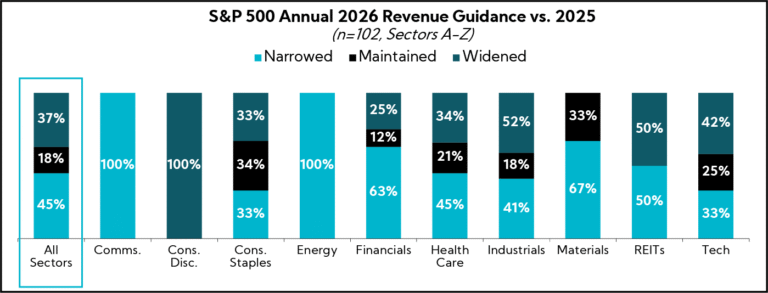

- Revenue: More companies, 45%, Narrowed the range relative to last year, while 37% Widened, and 18% Maintained; average spreads decreased 20 bps, with an average range of 2.1%

- 88% of companies expect full-year 2026 results to be above 2025 actuals

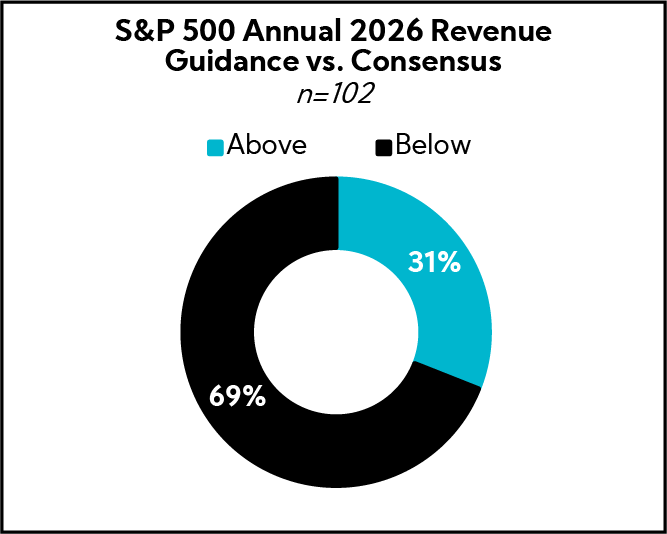

- 31% of companies forecast annual Revenue guides above consensus

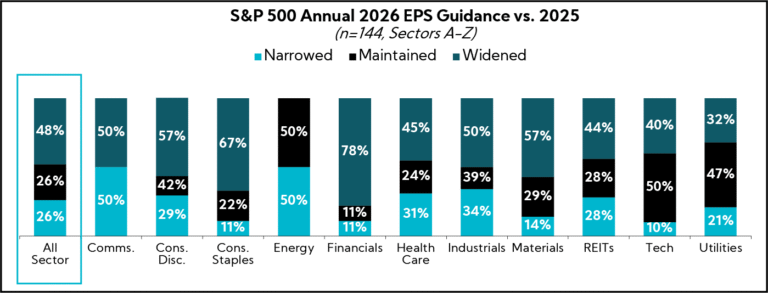

- EPS: More companies, 48%, Widened the range relative to last year, while 26% Narrowed and 26% Maintained; average EPS spreads increased from $0.30 to $0.36 on average EPS of $9.03 to $9.39.

- Widened ranges were most commonly attributed to macro uncertainty and limited visibility, potential policy, regulatory, and tariff changes, as well as higher expenses, interest rates, and tax rates

- 89% of companies expect full-year 2026 results to be above 2025 actuals

- 65% of companies forecast annual EPS guides above consensus

Consensus Shifts

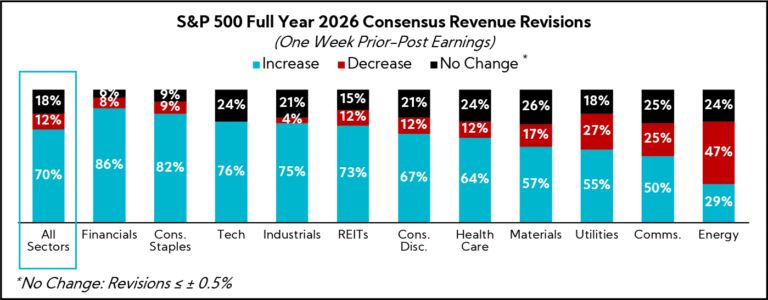

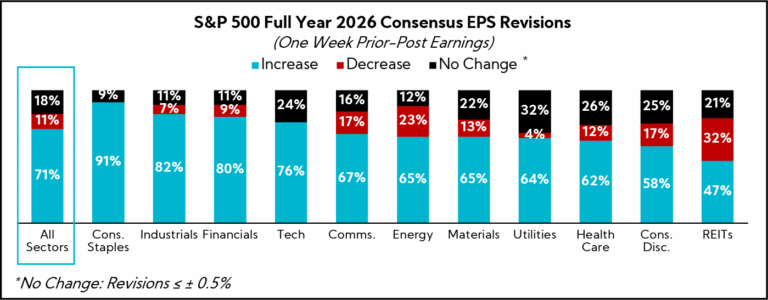

When analyzing Full Year 2026 consensus changes for calendar year S&P 500 companies from one week before through one week after Q4’25 earnings announcements, analyst revisions show a strong majority of companies experienced increased estimates for both Revenue and EPS.

Looking at Revenue, 70% of the group saw full-year consensus estimates raised. Upward revisions were broad-based, with increases of 50% or better for 10 of 11 sectors. The highest concentrations were in Financials (86%), Consumer Staples (82%), Tech (76%), Industrials (75%), and REITs (73%). Energy (47%), Utilities (27%), Communications (25%), and Materials (17%) saw the largest proportion of decreased consensus across sectors, though still offset by an equal or greater number of increases, with the exception of Energy.

For EPS, 71% of companies saw estimates increase. Again, upward revisions were broad-based, with the majority of sectors seeing increases at a rate of more than 50%. Upward revisions were concentrated in Consumer Staples (91%), Industrials (82%), Financials (80%), and Tech (76%). Downward revisions were most prevalent across REITs (32%), Energy (23%), Communications, and Consumer Discretionary (17%), which saw the largest share of lowered estimates.

Combining both metrics, Consumer Staples, Financials, Industrials, and Tech stood out with 70% of companies seeing both revenue and EPS revisions increase. In contrast, Energy and Communications saw a larger proportion of downward revisions across both metrics.

3. Artificial Intelligence

Markets are Increasingly Pricing AI Through a Disruption Lens, While Companies Continue to Highlight Productivity Gains and Margin Expansion; Clear, Quantifiable, and Defensible AI Communication is More Critical Than Ever

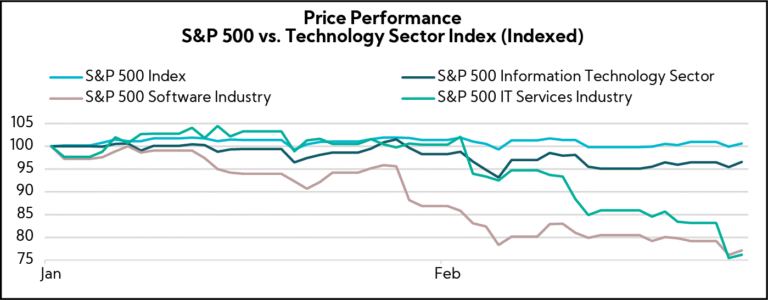

AI has entered a new phase in capital markets. The debate is no longer about technical capability, but about economic consequence. Over the past several weeks, we have seen a gradual and sustained divergence: while the broader S&P 500 has remained relatively stable, the technology index has steadily trended lower, particularly within software services. This measured underperformance suggests that investors have been incrementally repricing segments perceived as more exposed to AI-driven automation, labor displacement, margin compression, and structural disruption. It also underscores how sensitive markets have become to these narratives, as evidenced by the volatility observed this week following Citrini’s viral research post.

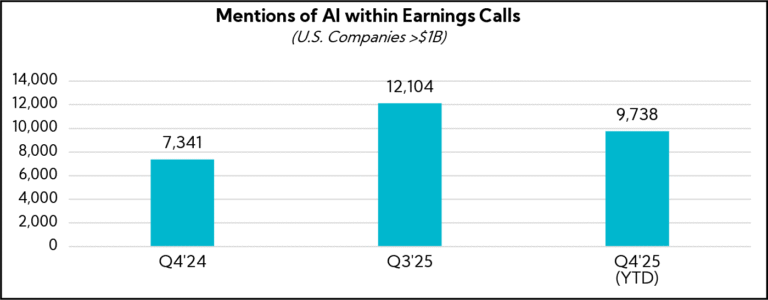

At the same time, earnings calls this quarter showed a markedly different tone. Companies continue to describe embedded deployment, measurable ROI, workflow integration, and multi-year demand. As we have mentioned before, AI has shifted from experimentation to institutionalization. The surge in AI mentions over the past year reinforces this shift, and the momentum continues into 2026. Mentions year-to-date are already approaching Q3’25 levels and are tracking roughly 33% above this time last year.

Across sectors, companies consistently frame AI as an enterprise productivity engine. Management teams emphasize automation across supply chains and operations, cost savings and margin expansion, enhanced customer engagement, and embedding AI directly into governed workflows. Infrastructure providers describe a “multi-year super cycle” in AI-related compute demand…services companies highlight AI-enabled transformation as an expansion of addressable markets…consumer companies are leveraging AI agents to enhance customer experiences. In short, AI is being positioned as a driver of operational leverage, revenue expansion, and competitive differentiation, rather than as a cause of systemic disruption.

However, the macro conversation has evolved. Investors are increasingly evaluating AI through the lens of disruption: who captures gains, whose margins compress, how labor markets adjust, and whether policy responses follow. In this environment, effective AI communication must do more than highlight innovation. It must demonstrate durability, governance, and measurable financial impact while acknowledging the legitimate questions around workforce and economic effects.

This quarter, many companies included a dedicated AI slide within their earnings presentations, and several published standalone AI presentations. These materials frequently address workforce impact, employment resilience, and data defensibility, signaling that management teams recognize the reputational and valuation sensitivities embedded in the broader AI debate.

Keep an eye out for our future Thought Leadership diving into AI Strategy and Communications. For the time being, below are key considerations when articulating your AI positioning:

- Quantifiable outcomes: Tie AI directly to measurable financial impact, including margin expansion, revenue growth, cost reduction, productivity gains, or retention improvement. Avoid abstract capability narratives.

- Workflow integration clarity: Emphasize AI embedded within governed enterprise workflows and orchestration layers, not operating autonomously or displacing core systems.

- Defensible data advantage (moat): Clearly articulate proprietary data assets, scale, model performance differentiation, compliance infrastructure, and strategic ecosystem partnerships.

- Balanced workforce positioning: Frame AI as an augmentation and a productivity enhancement. Address workforce implications thoughtfully, including reskilling, redeployment, and continued human oversight.

- Capital allocation discipline: Explain where AI investment fits within long-term strategy, expected return thresholds, and the time horizon for value realization.

- Governance and risk management: Acknowledge uncertainty without amplifying disruption narratives. Demonstrate strong governance, regulatory awareness, cybersecurity controls, and responsible deployment frameworks.

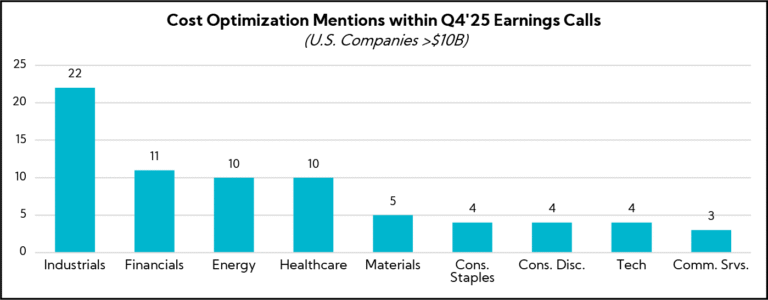

4. Cost Optimization

Companies Position Cost Optimization as a Multi-Year Strategic Imperative Rather than a Tactical Response to Inflationary Pressures, Tariff Headwinds, and Softening Demand Environments; Management Teams “Playing Offense” by Proactively Announcing Initiatives that Range from Structural Reorganizations and Workforce Reductions to Growing Deployment of AI-Powered Tools

Across the Q4’25 reporting cycle, companies increasingly framed cost optimization as a strategic, multi-year imperative rather than a transitory response to VUCA. Management teams consistently “played offense,” positioning cost initiatives as deliberate efforts to structurally rationalize expense bases amid sustained investment cycles, reinforce competitive advantages, and strengthen long-term strategic positioning, all while continuing to invest in priority growth vectors.

As shown in our findings below, the most cyclically exposed companies discussed cost optimization at the greatest levels. From a messaging perspective, the dominant framing was structural rather than transitory. Companies described the need to reset their cost base and improve unit economics by reconfiguring physical networks, consolidating footprints, and driving automation.

Among notable Industrial reporters, cost optimization was framed as a structural reset of the operating system, focused less on discretionary reductions and more on reconfiguring footprints, simplifying organizations, and creating durable productivity gains that can withstand mixed demand conditions. The most effective narratives explicitly tie actions to improving unit economics and quantify multi-year savings that underpin a burgeoning margin-improvement story.

Mechanically, initiatives spanned workforce reductions, organizational simplification, supply chain redesign, and accelerating deployment of AI-enabled tools. Importantly, companies rarely positioned these initiatives as a standalone strategy but instead explicitly tied them to broader margin expansion and growth narratives. By justifying investment spend through cost optimization, companies can signal steps taken to improve unit economics while positioning themselves for future growth.

Selected Commentary from Earnings Calls

January 26 – Baker Hughes ($38.8B, Energy): “Notably, our disciplined approach to cost optimization is fully aligned with our ongoing comprehensive review, with each initiative prioritized to drive structural margin improvement and enhance long-term competitiveness.”

January 29 – Waste Management ($90.9, Industrials): “Cost optimization remained a central theme in 2025. SG&A expense for the Legacy Business was 9.2% of revenue for the full year, a 10 basis point improvement compared to 2024, as we continue to rationalize discretionary spending.”

February 3 – Pepsi Co. ($183.5B, Consumer Staples): “To provide appropriate support for these commercial initiatives and improve profitability, we have accelerated our cost reduction efforts and improved the focus on operational excellence.”

February 24 – Westlake ($ 10.5B, Materials): “Building on the success for structural cost reduction efforts achieved in 2025, we have implemented an additional structural company-wide cost reduction program that we expect will deliver $200 million in 2026. These decisive steps and the commitment to deliver improved financial performance through these self-help actions will deliver better utilized assets and an improved cost structure to compete in a global marketplace.”

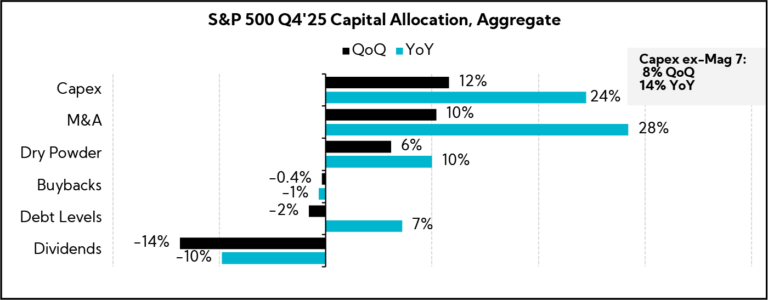

5. Capital Allocation:

Cash Deployment Trends Remain Growth-oriented as M&A Activity Strengthens and Capex Remains Robust; Dividends Decline QoQ and YoY

To garner insights into capital trends, we analyzed the average sector allocations within the S&P 500.5

S&P 500 capex remained robust this quarter, increasing 12% QoQ and 24% YoY. Normalizing for The Mag 7, growth was 8% QoQ and 14% YoY. Across other capital allocation categories, results were broadly consistent when The Mag 7 were excluded, with the exception of dry powder, which increased 2% QoQ and 6% YoY, compared to 6% QoQ and 10% YoY for the full S&P 500. Buybacks were largely stable, edging down 0.4% QoQ and 1% YoY. Debt levels were mixed, rising 7% YoY but declining 2% QoQ. Dividend growth posted the largest decline, down 14% QoQ and 10% YoY.

Sector-level analysis of median capex shows increases across all sectors on a QoQ basis, led by Communication Services (17%), REITs (16%), Health Care (16%), and Industrials (15%).

The trends are largely positive YoY, driven by increases in Communication Services (29%), Utilities (12%), Financials (10%), and Energy (10%), with Tech and REITs also showing solid YoY increases. Materials and Consumer Staples were the only sectors to pull back on capex, down 4% and 2% YoY, respectively.

Keep an eye out for our upcoming Thought Leadership on Capex, including the implications of increased spend in key growth areas like data centers.

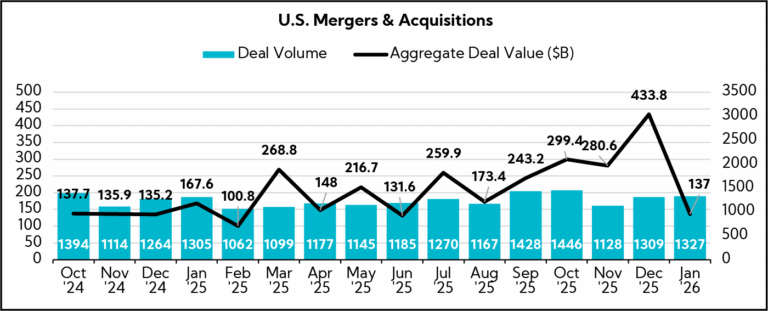

M&A activity was notably higher, up 10% QoQ and 28% YoY. In the U.S., deal volumes declined in November but rebounded through December accompanied by a meaningful increase in aggregate deal value. That strength proved short-lived, as aggregate value declined sharply in January despite continued momentum in deal volume.

In Closing

As we close out 2025 and look ahead, more and more companies are leaning into strategic growth. Capex is increasingly framed as targeted investment (automation, innovation, capacity) and M&A appetite remains robust as boards reassess portfolios and pursue scale, capabilities, and adjacent growth. All things being equal, the compounding effect of capex investment could support an inflection in 2026, with post-tax season consumer demand a key gauge of whether OBBBA stimulates activity.

To that end, the consumer remains the clearest real-time barometer, and Q4 reinforced a subtle but important change in behavior. Spending isn’t broken, but it has continued to become more selective and more skewed toward essentials. Confidence measures softened into year end, and customers are still participating, just with a sharper filter: value first, substitute where possible. That dynamic is manageable, but it puts a premium on mix and pricing discipline and creates tighter expectations in 2026. At the same time, equity market performance continues to be a source of confidence for those who are lucky enough to be on the top of the K.

AI continues to reset competitive baselines, but the market is now grading it with a tougher rubric. The narrative has matured from capability to accountability: where is the measurable productivity, what is the payback period, and how does incremental AI spend show up in margins and cash flow? At the same time, operating model implications are becoming more visible. Automation is compressing cycle times and headcount, and “efficiency programs” increasingly look like permanent redesigns and strategic imperatives rather than reactive cost-cutting actions.

The stage is set for a seemingly productive 2026 with the main disruptor to success being geopolitics and policy. Can we just have a “normal” year?

- Combines actual reported results for companies and estimated results for companies yet to report

- Source: LSEG I/B/E/S

- As of February 23, 2026

- Based on company guidance provided at the time of publication; total number of companies differs across revenue and EPS

- As of February 25, 2026; “All Sectors” figures are equal weighted sector averages