While performances have varied from company to company, in aggregate, Industrials currently represent the only sector in the S&P 500 where the majority of reported top-line figures have come in below consensus. Moreover, while bottom-line results have fared more positively relative to estimates, those beating earnings consensus is still below the S&P 500 average (73% vs. 78%, respectively).

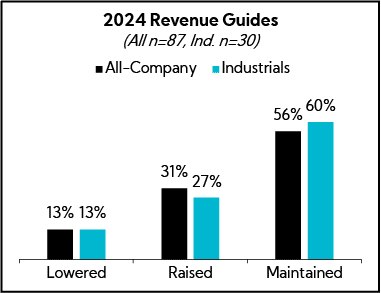

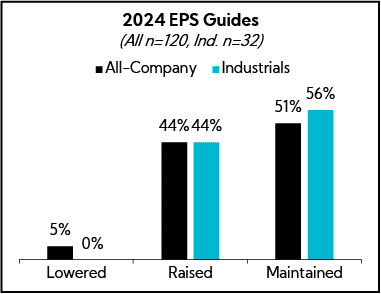

Despite executives pointing to continued macro headwinds, very few companies have lowered initial annual guides delivered at the top of the year, and many are in fact raising (albeit, not at propensities remarkably different than the broader market). Indeed, the Manufacturing PMI came up for air during the latest March print after 16 months of readings in contraction territory, in addition to a well-received improvement in the New Orders Index. While one month does not make a trend, these data points imply light at the end of this tunnel for some of the harder-hit segments, such as freight, which has been in a recession. As one executive put it, “We should be getting closer to the end of this than the beginning”.

Key Themes

Outlook – Tough Market Conditions Persist across Certain Industries Such as Transportation and Building Products, but Companies are “Controlling the Controllables” and Underlying Conditions Seem to be “Building Momentum” with “Back-Half Strength” a Consistent Theme

Demand and Order Trends – Moving Past Notable Inclement Weather Impact in Q1, Commentary Suggests Accelerating Backlog Growth in Coming Quarters; Freight Remains a Sore Spot, though Many Suggest We Have Reached a Bottom

Inflation and Pricing – Persistent Inflation Leads to Continued Pricing Actions Leads to Persistent Inflation

Corbin Advisors is a strategic investor relations and investor communications advisory firm with a track record of supporting our publicly traded clients in creating sustained shareholder value. Our approach leverages decades of Voice of Investor® (VOI®) research and data-driven insights; capital markets expertise and deep best practice knowledge; and a proven playbook and passion for client outperformance. We are a trusted advisor and partner to boards of directors, executive leaders, and investor relations professionals, serving a broad range of companies globally across sectors, sizes, and situations. Through defining the standard of excellence and challenging conventional thinking, we enable our clients to boldly differentiate their equity brand, maximize valuation, and build more durable franchises.