This Week in Earnings – Q2'23

The Sector Beat: Consumer Discretionary

In today’s Thought Leadership, we’re covering…

- Key Events this week

- Earnings Snap, covering the S&P 500 stats to date

- The Sector Beat: Consumer Discretionary

Key Events

Manufacturing and Service

- The ISM Manufacturing PMI® registered at 46.4 in July, a 0.4% increase from June, representing the eighth month of contraction after a 30-month period of expansion; the New Orders Index remained in contraction territory at 47.3, 1.7% higher than in June (Source: Institute for Supply Management)

- The ISM Non-Manufacturing PMI® decreased to 52.7 in July from 53.9 in June; a reading above 50 indicates growth in the services industry, which accounts for more than two-thirds of the U.S. economy (Source: Institute for Supply Management)

Labor

- Nonfarm payrolls expanded by 187,000 in July, slightly below the Dow Jones estimate for 200,000; though the headline number was a miss, it represented a modest gain from the downwardly revised 185,000 in for June (Source: Labor Department)

- The unemployment rate was 3.5% in July, slightly below consensus estimates that the rate would hold steady at 3.6%; a more encompassing unemployment rate that includes discouraged workers and those holding part-time jobs for economic reasons fell to 6.7%, down 0.2% from June (Source: Labor Department)

- Average hourly earnings, a key figure as the Federal Reserve fights inflation, rose 0.4% for the month, good for a 4.4% annual pace — both numbers were higher than the respective estimates for 0.3% and 4.2% (Source: Labor Department)

U.S. Politics

- Donald Trump was indicted Tuesday in a criminal case accusing the former president of trying to subvert the will of American voters; the indictment by a federal grand jury in Washington, D.C. charges Trump with four crimes, including conspiring to defraud the U.S., obstructing an official proceeding, and conspiring against the rights of voters for his actions that culminated in the Jan. 6, 2021 (Source: WSJ)

U.S. Debt

- Fitch Ratings downgraded the U.S. government’s credit rating weeks after President Biden and congressional Republicans came to the brink of a historic default, warning about the growing debt burden and political dysfunction in Washington; the downgrade, the first by a major ratings firm in more than a decade, now stands at “AA+”, or one notch below the top “AAA” grade (Source: WSJ)

S&P 500 Earnings Snap

78% of the S&P 500 has reported earnings to date.

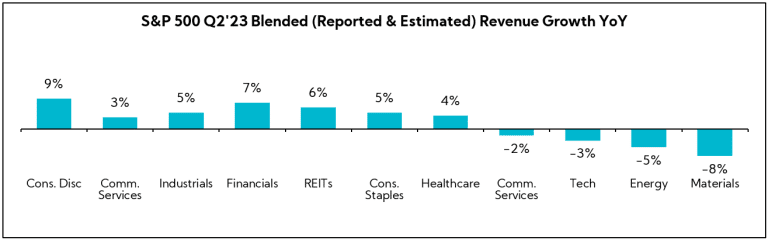

Q2'23 Revenue Performance

- 64% have reported a positive revenue surprise, below the 1-year average (71%) and 5-year average (69%)

- Blended revenue growth (combines actual reported results for companies and estimated results for companies yet to report) is 0.1%today, compared to -0.4% last week and -0.4% at the end of last quarter

- Companies are reporting revenue 1.7% above consensus estimates, below the 1-year average (+2.5%) and the 5-year average (+2.0%)

Q2’23 EPS Performance

- 79% have reported a positive EPS surprise, above the 1-year average (73%) and slightly above the 5-year average (77%)

- Blended earnings growth (combines actual reported results for companies and estimated results for companies yet to report) is -5.0% today, compared to -6.4% last week and -7.0% at the end of last quarter

- Companies are reporting earnings 7.1% above consensus estimates, well above the 1-year average (+3.2%) but below the 5-year average (+8.4%)

The Sector Beat: Consumer Discretionary

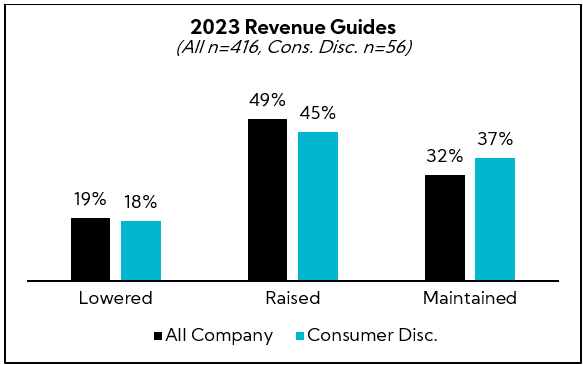

Guidance Trends

Consumer Discretionary Sector: Breakdown by Industry

On average, a greater number of Consumer Discretionary companies are raising revenue guidance, with slightly more maintaining versus our All-Company benchmark. As for EPS, 15% more Consumer Discretionary companies are lowering their earnings guides than the All-Company benchmark, with a roughly even proportion raising, maintaining, or lowering their annual projections — a reflection of the disparate levels of consumer spending being observed across industries.

Revenue Guidance

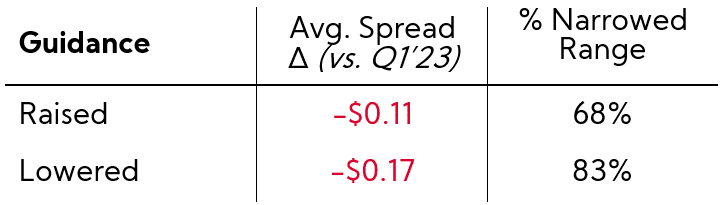

- Companies that raised annual EPS guidance (n = 17):

- 94% raised the bottom and top of the original range

- Average spreads decreased from $0.43 last quarter to $0.31 this quarter

- Companies that maintained annual EPS guidance (n = 15):

- Average spread of $0.24

- Companies that lowered annual EPS guidance (n = 18):

- 78% lowered the bottom and top of the original range

- 11% lowered the bottom and maintained the top of the original range

- Average spreads decreased from $0.47 last quarter to $0.30 this quarter

EPS Guidance

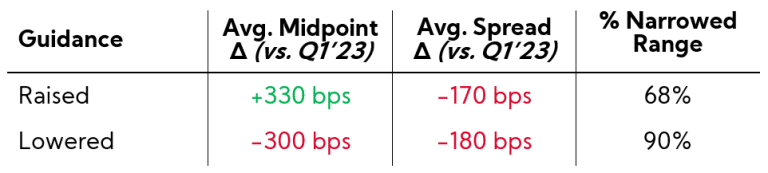

Consumer Discretionary companies that raised annual revenue guidance (n = 25):

- 72% raised the bottom and top of the original range

- 20% raised the bottom and maintained the top of the original range

- One company raised the top and lowered the bottom, while another maintained the bottom and raised the top

Consumer Discretionary companies that maintained annual revenue guidance (n = 21):

- 2023 growth guides range from -11% to +34%, with an average midpoint of +8.6%

Consumer Discretionary companies that lowered annual revenue guidance (n = 10):

- 80% lowered the bottom and top of the original range

- 10% lowered the bottom and maintained the top of the original range

- 10% lowered the top and raised the bottom of the original range

Earnings Call Analysis

Further, we analyzed the earnings calls for this group and the broader Consumer Discretionary universe to identify key themes.

As we reported in our Consumer Discretionary Sector Beat last quarter, inflation is persistent, albeit improving, across most industries and consumer activity increasingly suggested a widening gap between upper- and lower-income cohorts. Nonetheless, the consumer continued to spend, and companies, in general, continued to pass on costs, resulting in historically low savings rates and record credit balances.

Exiting Q2’23, executives largely cite a “fairly strong” consumer, though commentary suggests conditions have marginally softened versus Q1.

Indeed, a cursory view of headline consumer data points suggests an increasingly strained environment. According to the latest LendingClub report, 61% of consumers lived paycheck-to-paycheck in June, an increase of 4% from May, with 21% struggling to pay their monthly bills. Further, despite a 0.2% uptick, retail sales rose less than expected in June, and the U.S. savings rate ebbed to 4.3%, a 0.3% decrease from the month prior and well below the long-term average of 8.8%. Meanwhile, Fed data shows bank lending conditions continue to tighten.

As such, executives are reporting normalizing demand among most consumer sector industries, with back half expectations largely calling for “as good as” or potentially deteriorating conditions in light of the continued impact of rising interest rates and the resumption of U.S. student loan payments beginning in October.

Among the headwinds mentioned this quarter were persistent wage inflation pressures, a fluid pricing environment, and the residual effects of elevated inventory levels among wholesale distributors. On the positive side, input and shipping costs for many appear to have moderated over the past several months, and executives continue to tout the realized benefits of cost savings plans.

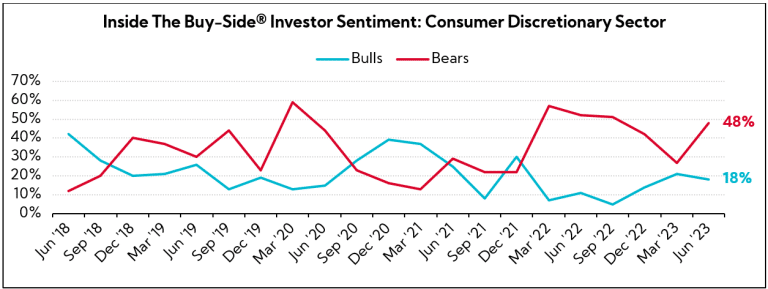

Notably, our Q2 Inside The Buy-Side® Earnings Primer® found an increase in bearish sentiment for Consumer Discretionary — an indication that the Street is predicting fallout.

“Fairly Strong,” but Showing Signs of Softness; Resumption of Student Loan Payments is an Anticipated Headwind in the Coming Quarters, while Purchasing Behavior Indicates Clear Preferences for Services and Consumables vs. Durable Goods

- Travel + Leisure (FY Q2’23 – $3.1B, Travel Services): “Although we expect consumers will continue to prioritize vacations, we came into the year anticipating some normalization of demand trends. We saw some of this in the second quarter, and our guidance for the second half of the year reflects a range of outcomes, including at the low-end potential softening of trends.”

- Amazon (FY Q2’23 – $1.3T, Internet Retail): “During the quarter, we saw improvements in macroeconomic indicators across our North America and international segments, but continue to see customers trading down and seeking value in their purchases.”

- Mohawk Industries (FY Q2’23 – $6.7B, Furnishings, Fixtures & Appliances): “We had expected that with the decline in energy prices…the consumer would be positively impacted. At this point, we haven’t seen the demand in flooring reflect that. There are more vacations being taken and experiences they’re having. But in our category, we haven’t seen an improvement yet.”

- Whirlpool Corp. (FY Q2’23 – $7.9B, Furnishings, Fixtures & Appliances): “Discretionary side of the demand continues to remain soft. And we see that in the major appliances, and we see it most in small domestic appliances. That’s the nature of discretionary demand, which is right now still impacted by uncertainty in consumer sentiment, which is still not in a positive territory.”

- Legget & Platt (FYQ2’23 – $4.0B, Furnishings, Fixtures & Appliances): “The health of the consumer…it’s fairly strong at this point as we’ve seen inflation easing and job market remaining strong and wages improving. But the focus on consumer spending really remains on services and consumables rather than durable goods. And that’s really the drag that we’re seeing on our Furniture, Flooring and Bedding, more residential end markets.”

- Pool (FY Q2’23 – $14.9B, Industrial Distribution): “[We’re] seeing a pattern in that the non-discretionary business is holding up quite well. But some of the equipment is more discretionary. ‘I should have one. I don’t have to have one. If I have an older one, I might be able to get by another year with it.’ ’[We’re] seeing some hesitation [from] the consumer at that point.”

- Overstock.com (FY Q2’23 – $1.7B, Internet Retail): “Consumer continues to prioritize service-related and need-based spending, putting pressure on the demand for discretionary home goods.”

- Tractor Supply (FY Q2’23 – $24.6B, Specialty Retail): “The consumer on some of the discretionary items is a little bit more prudent today. And then also we’re acknowledging as I mentioned some of the impulse and discretionary categories. We anticipate consumer behavior is in line with the first half of the year.”

- Bloomin’ Brands (FY Q2’23 – $2.2B, Restaurants): “The high end is doing well and our casual dining brands, we see the consumer hanging in there.”

- Yum! Brands (FY Q2’23 – $38.4B, Restaurants): “Value is rising in importance…KFC for U.S., for example, the most growth was seen in their low-income consumers.”

Student Loan Payments

- Newell Brands (FY Q2’23 – $4.5B, Household & Personal Products): “We are incrementally more cautious on the consumption of discretionary products, largely due to the resumption of student loan payments in October. As payments restart after a multiyear moratorium, many consumers will undoubtedly have to manage their budgets even tighter given persistently high core inflation, which has lowered real consumer income.”

- Carter’s (FY Q2’23 – $2.8B, Apparel Retail): “We believe consumer demand will continue to be pressured by various macroeconomic factors, including inflation, higher interest rates, and higher consumer debt levels. The resumption of required student loan repayments is a question mark at the moment, but this could further stretch our core consumers.”

- V.F. (FY Q1’24 – $7.5B, Apparel Retail): “Many consumers are feeling impacts to their disposable income and are continuing to deal with inflation, facing higher interest rates, and in the U.S., the upcoming end to the student loan pause. For fiscal year 2024, we are slightly more cautious on the evolution of revenue.”

Q2 Margins Benefit from Lower Freight and Input Costs, Offset by Elevated Wage Pressures; As Elasticities Shift, Execs Toe the Line Between Volume and Price

- Carter’s (FY Q2’23 – $2.8B, Apparel Retail): “We believe the outlook for gross margin is positive with planned expansion driven by lower ocean freight and product costs and continued discipline in pricing and promotions.”

- Autoliv (FY Q2’23 – $8.7B, Auto Parts): “The gross profit increase was primarily driven by price increases, volume growth, and lower costs for premium freight. This was partly offset by increased cost for personnel related to volume growth and wage inflation, as well as adverse effects from unfavorable exchange rates and energy costs.”

- Amazon (FY Q2’23 – $1.3T, Internet Retail): “Across our North America and international results, inflation headwinds continue to ease, most notably in fuel prices, linehaul rates, ocean and rail rates.”

- Polaris (FY Q2’23 – $7.4B, Recreational Vehicles): “EBITDA margin…was down, driven by continued high labor costs and finance interest. Partially offsetting some of these headwinds was net pricing and lower cost premiums on items such as logistics.”

Pricing

- Dana (FY Q2’23 – 2.7B, Auto Parts): “Cost inflation continues to be an issue as many input costs remain high, including labor and European energy. Pricing actions are muting the impact of inflation but will not completely offset it in the second half.”

- Mohawk Industries (FY Q2’23 – $6.7B, Furnishings, Fixtures & Appliances): “We expect lower industry volumes will continue pressuring pricing and mix across the whole industry. “

- Bloomin’ Brands (FY Q2’23 – $2.2B, Restaurants): “We’ve got to be very prudent on our pricing. Rather than price up and discount back, we’d rather try and be prudent in our pricing and make sure that value comes to the consumer that way along with great food and great service.”

- Hilton Worldwide (FY Q2’23 – $40.7B, Lodging): “We are pushing hard on price because we’ve been in a highly inflationary environment. And from the standpoint of trying to make our hotel owners the most money, that relative trade is the right trade, keep pushing price hard even though it might impact occupancy.”

Cost Controls/Restructuring

- Monro (FY Q1’24 – $1.1B, Auto Parts): “Broad-based inflationary pressures have persisted such that the consumer slowed their purchases of some of our higher ticket service categories. As a result of this, we took swift action to reduce non-productive labor costs, including overtime hours in our stores, which allowed us to preserve margins and profitability on lower-than-expected sales.”

- Newell Brands (FY Q2’23 – $4.5B, Household & Personal Products): “Additional sales compression, coupled with our decision to lower inventory balances even further, does create a short-term fixed cost absorption challenge. Although we are aggressively optimizing the company’s manufacturing labor force within the confines of our existing plant network, fixed cost deleveraging will still weigh on our second half gross and operating margins.”

- Autoliv (FY Q2’23 – $8.7B, Auto Parts): “Our labor efficiency continues to trend up, supported by the implementation of our strategic initiatives, including automation and digitalization. Our gross margin improved by 180 bps compared to the first quarter, as a result of the higher labor efficiency, customer compensations, higher volumes, and a more stable light vehicle production.”

Proceeding with Caution, Wholesalers Limit Buys Amid Residual Inventory Glut

- Crocs (FY Q2’23 – $6.6B, Footwear & Accessories): “As we look at our bookings for Q4, they were more conservative than we thought they were going to be…the reasons that we’ve been told and the reasons that we understand for that is, number one, the wholesale channel. The majority of the wholesale channel has been pretty cautious about the back half of this year. They have some inventory overhang from some other brands that they need to work through.”

- Skechers (FY Q2’23 – $8.6B, Footwear & Accessories): “[Wholesalers are] dealing with inventory issues that extend beyond the Skechers brand and that has been one of the bigger challenges. It’s not every customer. We have wholesale customers out there who are doing fantastic. And that’s what led to some of the improvement in results relative to our second quarter. I don’t know how long it will take them to deal with the totality of whatever congestion they’re experiencing.”

- Columbia Sportswear (FY Q2’23 – $4.6B, Apparel Manufacturing): “For the back half…retailers are generally being more cautious. As we sit here today, spring sell-through has been a bit slower [and] inventory levels in the marketplace are moderately elevated. So, when you look at some slowdown in higher inventories, naturally retailers are going to be a bit more cautious. That’s what we’re reflecting in terms of the change in how we’re seeing the revenue forecast for the balance of the year.”

- Vista Outdoor (FY Q1’24 – $1.8B, Leisure): “While inventory levels are improving in big box and retail, they remain challenged at wholesale distributors, dealer, and international channel. Until the back half of our fiscal year, we expect point-of-sale to exceed sell-in as excess inventory is cleared.”

- Deckers Outdoor (FY Q1’24 – $14.2B, Footwear & Accessories): “There’s some noise out there in the wholesale channel with markdowns and promotions from other brands, a lot of inventory in the channel.”

- V.F. Corp. (FY Q1’24 – $7.6B, Apparel Manufacturing): “The reason for the change in revenue outlook is based primarily on wholesale. Despite the progress made in lowering inventory levels, our wholesale business remains pressured. While our sellout trends are evolving favorably in the Outdoor segment in particular, selling is challenged across the segments.”

While Inflation Appears to be Ebbing for Most, Many Continue to Point to Persistent Wage Pressures as Labor Conditions Remain Tight

- Harley-Davidson (FY Q2’23 – $5.5B, Recreational Vehicles): “Labor and warehousing costs continue to be the primary drivers of inflation, with deflation and moderation expected within logistics, freight, and raw materials.”

- O’Reilly Automotive (FY Q2’23 – $56.3B, Specialty Retail): “Overall, from a workforce perspective, we’re continuing to see pressure from a wage rate standpoint there.”

- Texas Roadhouse (FY Q2’23 – $7.5B, Restaurants): “We expect the level of labor inflation to moderate as we move through the year. That said, we have seen marginally more wage pressure in the first half of the year than we originally contemplated. As such, we have updated our full year 2023 guidance for wage and other labor inflation to between 6% and 7%, with current trends pointing towards the midpoint of that range.”

- Genuine Parts Co. (FY Q2’23 – 21.9B, Specialty Retail): “We’re seeing some inflationary pressure on operating expenses, particularly in wages. That’s sitting in the mid-single digit range right now. It’s probably the most pronounced impact in the business, but we’re managing it. We’re doing all the right things and taking some actions to try to offset that. And that’s not a GPC-specific comment, it’s a comment that all businesses are facing with wage pressure and inflation and wages.”

- Installed Building Products (FY Q2’23 – $4.3B, Residential Construction): “It’s been talked a lot about in the press that wage inflation, while still higher maybe than some people want, is normalized considerably.”

Japan and India Demonstrate Strong Growth in Lieu of Companies De-Risking China; In Line with Industrial Commentary, the Expected Recovery in China Lagged Expectations

- Hugo Boss (FY Q2’23 – $4.9B, Apparel Manufacturing): “We are de-risking China a lot in the Asian markets. We are moving from China to Vietnam, Pakistan, Sri Lanka to Turkey to other regions to de-risk China. “

- Accor SA (FY Q2’23 – $9.7B, Lodging): “We saw good growth in Japan cities in particular in the first half. They do tend to travel and have high purchasing power. This was an objective we had to significantly grow our presence in Japan. The other market that we’re looking at is India. This is a market that has really, really good growth potential given the emergence of middle class and very good growth potential for us.”

- Schaeffer AG (FY Q2’23 – $3.8B, Auto Parts): “We all need to be aware of the lower comps in Q2 when it comes to China. [The] Industrials [business] is already indicating that there is headwind, and we are also expecting a headwind going forward. India is one of the areas where we will continue to localize more. And that also goes for the new sectors like robots or medical applications.”

- MakeMyTrip (FY Q2’23 – $3.4B, Travel Services): “India generated Asia’s highest outbound travel volume for the first time in 2023, exceeding those of China, South Korea, and Japan, partially aided by lagged recovery of outbound travel in China.”

- Garmin (FY Q2’23 – $20.6B, Scientific & Technical Instruments): “Asia is a big place, some countries are doing very well while in other cases, maybe the economies aren’t so good, specifically China.”

In Closing

There is little question that the consumer has held up better than most feared entering 2023. As a result, many of the companies in the consumer sector that have reported thus far have been able to navigate this environment due to conservative assumptions heading into the year.

While continued strong employment and wages have been the primary driver of continued consumer spend thus far, there is a growing bifurcation in the data we see indicating that consumers with less savings remain constrained by and more sensitive to higher interest rates, the impact of higher cost of living (even as headline inflation ebbs), tightening bank lending standards, and the upcoming resumption of student loan payments.

We expect the next few quarters will be very telling, especially if the Fed is successful in affecting wage inflation through loosening of the employment market. We suspect there will be greater sensitivity for consumer spending versus past economic cycles if and when unemployment starts trending up again.

- As of August 3, 2023

- The total number of companies in the all-company benchmarks are different across revenue and EPS charts and based on the data available and reported by companies at the time of our publication.