This Week in Earnings – Q4'25

Consumer Discretionary & Staples Sector Beat

Our thought leadership this week addresses:

- Key Events this week

- Earnings Snap, covering the S&P 500 stats to date

- Spotlight on Consumer Discretionary & Staples in The Sector Beat

Key Events

CPI

- The U.S. Consumer Price Index rose 0.2% in January, slightly below the consensus estimate of 0.3%, bringing the YoY increase to 2.4%. Core CPI, which excludes food and energy, increased 0.3% in January and 2.5% annually. The monthly increase was driven by transportation services (+1.4%), utility (piped) gas service (+1.0%), and apparel (+0.3%), while declines in fuel oil (-5.7%), gasoline (-3.2%), and used cars and trucks (-1.8%) partially offset those gains. (Source: BLS)

Employment

- January nonfarm payrolls increased by 130K, well above the consensus estimate of 70K. The unemployment rate edged down to 4.3%, while labor force participation rose to 62.4%. Job gains were concentrated in education and health services (+137K), professional and business services (+34K), and construction (+33K). (Source: BLS, Bloomberg)

- U.S. initial jobless claims declined by 5,000 to a seasonally adjusted 227K for the week ended February 7, slightly above the consensus estimate of 226K. Continuing claims increased to 1862K for the week ended January 30. The latest data suggest layoffs remain relatively contained, despite previously announced job-cut plans from large employers such as Amazon and UPS, indicating those announcements have not yet resulted in a broad-based rise in claims. (Source: Labor Department, Bloomberg)

Policy

- The House voted Wednesday to block President Trump’s tariffs on Canada, with six Republicans joining Democrats in support of the measure. The resolution, which seeks to overturn the national emergency declaration used to justify the tariffs, passed 219–211. The resolution now heads to the Senate, though a presidential veto is expected and Congress is unlikely to override it. Lawmakers opposing the tariffs argued they weigh on economic growth and function as an added cost to U.S. consumers, manufacturers, and farmers. (Source: CNBC, Politico)

- A Department of Homeland Security shutdown appears likely after the Senate failed to advance a funding bill amid a standoff over immigration enforcement limits, with Democrats seeking new guardrails on ICE and Republicans pushing for a stopgap measure. While most DHS functions would continue and roughly 92% of employees would remain on duty, a prolonged lapse could disrupt airport operations and delay pay for workers, increasing pressure on lawmakers to reach a deal. (Source: Bloomberg, WSJ)

Policy-by-Post

- February 11: President Trump threatened those in his party who voted against his tariffs – “Any Republican, in the House or the Senate, that votes against TARIFFS will seriously suffer the consequences come Election time, and that includes Primaries! Our Trade Deficit has been reduced by 78%, the Dow Jones has just hit 50,000, and the S&P, 7,000, all Numbers that were considered IMPOSSIBLE just one year ago. In addition, TARIFFS have given us Great National Security because the mere mention of the word has Countries agreeing to our strongest wishes. TARIFFS have given us Economic and National Security, and no Republican should be responsible for destroying this privilege.” (Source: Truth Social)

- February 7: President Trump criticized Canada’s trade and infrastructure polices – “As everyone knows, the Country of Canada has treated the United States very unfairly for decades. Now, things are turning around for the U.S.A., and FAST! But imagine, Canada is building a massive bridge between Ontario and Michigan. They own both the Canada and the United States side and, of course, built it with virtually no U.S. content. President Barack Hussein Obama stupidly gave them a waiver so they could get around the BUY AMERICAN Act, and not use any American products, including our Steel. Now, the Canadian Government expects me, as President of the United States, to PERMIT them to just “take advantage of America!” What does the United States of America get — Absolutely NOTHING! Ontario won’t even put U.S. spirits, beverages, and other alcoholic products, on their shelves, they are absolutely prohibited from doing so and now, on top of everything else, Prime Minister Carney wants to make a deal with China — which will eat Canada alive. We’ll just get the leftovers! … The revenues generated because of the U.S. Market will be astronomical. Thank you for your attention to this matter!” (Source: Truth Social)

Earnings Snap

74% of the S&P 500 has reported earnings to date

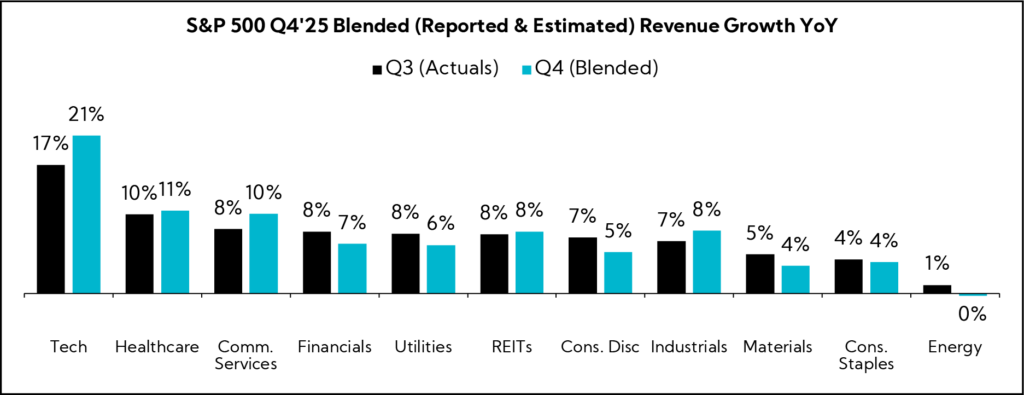

Q4'25 Revenue Performance

- 73% have reported a positive revenue surprise, above the 1- and 5-year averages of 71% and 70%, respectively

- Blended revenue growth (combines actual reported results for companies and estimated results for companies yet to report) is 8.6%

- Companies are reporting revenue 1.7% above consensus estimates, higher than 1-year average of 1.3% and lower than the 5-year average of 2.0%

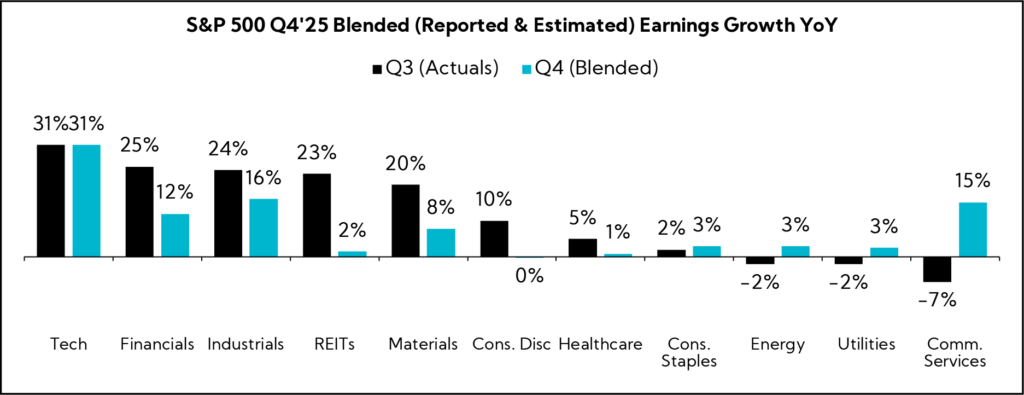

Q4’25 EPS Performance

- 75% have reported a positive EPS surprise, slightly below the 1- and 5-year averages of 78% and 79%, respectively

- Blended earnings growth (combines actual reported results for companies and estimated results for companies yet to report) is 13.6%

- Companies are reporting earnings 5.1% above consensus estimates, below the 1- and 5-year averages of 7.4% and 7.7%, respectively

The Sector Beat: Consumer Discretionary & Staples

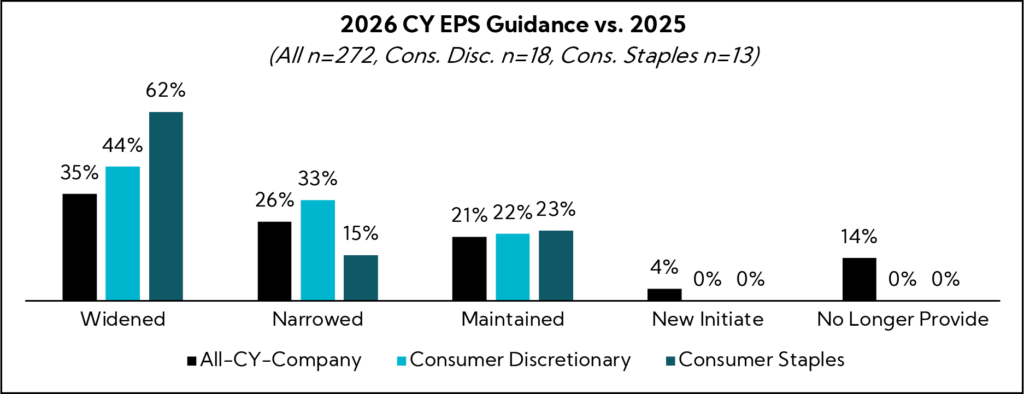

Consumer Discretionary & Staples Guidance Trends

We analyzed annual revenue and EPS guidance provided by calendar year Consumer Discretionary & Staples companies with market caps ≥$1B that have reported to date.

For comparison purposes, we provide an “All-Company” benchmark, which tracks in real-time a basket of calendar-year companies ≥$1B in market cap across all sectors that have reported earnings to date (n = 338).1

1. As of 2/12/2026

Consumer Discretionary Guidance Breakdown by Industry

| Industry | Number of Companies |

|---|---|

| Automobile Components | 6 |

| Household Durables | 5 |

| Leisure Products | 4 |

| Hotels, Restaurants, and Leisure | 3 |

| Specialty Retail | 3 |

| Diversified Consumer Services | 2 |

| Textiles, Apparel, and Luxury Goods | 2 |

| Automobiles | 1 |

| Total | 26 |

Source: Corbin Advisors

Consumer Staples Guidance Breakdown by Industry

| Industry | Number of Companies |

|---|---|

| Food Products | 6 |

| Household Products | 3 |

| Beverages | 2 |

| Consumer Staples Distribution & Retail | 2 |

| Diversified Consumer Services | 2 |

| Total | 15 |

Source: Corbin Advisors

Annual Revenue and EPS Guidance

Revenue – Overall Consumer Sector

52% of consumer companies have Narrowed guidance relative to last year, compared to the all-company benchmark of 39%, while 32% Widened their guidance; 77% of midpoints are above 2025 actuals.

- Consumer Discretionary (Revenue): Most companies, 62%, Narrowed spreads relative to last year, compared to the all-company benchmark of 39%, while 29% Widened; midpoints average 2.6% growth in 2026, 80% of midpoints are above 2025 actuals

- Consumer Staples (Revenue): 40% Widened guidance relative to last year, while 30% Narrowed and 30% Maintained guidance; midpoints average 3.0% growth in 2026, 70% of midpoints are above 2025 actuals

EPS – Overall Consumer Sector

52% of consumer companies Widened guidance relative to last year, well above the all-company benchmark of 35%; 26% Narrowed and 23% Maintained spreads; 94% of midpoints are above 2025 actuals.

- Consumer Discretionary (EPS): 44% Widened guidance relative to last year, above the all-company benchmark (35%). 94% of midpoints are above 2025 actuals

- Consumer Staples (EPS): Most companies, 62%, Widened guidance relative to last year, well above the all-company benchmark (35%); 23% Maintained spreads, in line with the all-company benchmark of 21%. 92% of midpoints are above 2025 actuals

Earnings Call Analysis

We analyzed the earnings calls across the Consumer universe to identify key themes.

Consumer companies are entering 2026 with cautious outlooks, expecting another year defined by macro volatility, geopolitical uncertainty, and a highly promotional operating environment. While moderating inflation and future rate cuts are expected to provide some relief, particularly in rate-sensitive categories such as housing and big-ticket discretionary, management teams are not expecting a sharp rebound.

The consumer remains pressured and distinctly bifurcated. Lower- and middle-income households continue to trade down, seek value, shift channels, and manage tighter budgets through smaller baskets, private label adoption, and increased promotional sensitivity. At the same time, higher-income consumers remain comparatively resilient, supporting premium, innovation-led, and discretionary categories. This tale of two consumers dynamic is reinforcing a value-oriented, promotion-heavy environment in which pricing power is more selective and closely tied to perceived value.

Tariffs remain a meaningful headwind entering 2026, creating incremental cost and margin pressure across industries. While some companies have successfully mitigated impacts through pricing and supply chain diversification, tariff costs are not fully offset. The environment remains dynamic, with timing lags, cash flow implications, and demand elasticity all influencing how effectively companies can absorb or pass through costs. This is most notable for staples companies where guidance ranges are wider year-over-year.

Against this backdrop, expense management remains a central lever to protect profitability. Companies continue to execute structural cost reduction programs, productivity initiatives, and supply chain optimizations to drive meaningful savings. These efforts are funding targeted growth investments while helping offset inflation, pricing pressure, and tariff-related costs.

At the same time, AI and digital acceleration are emerging as key strategic enablers. Companies are moving beyond experimentation toward scaled, enterprise-wide deployment of AI across supply chain, operations, finance, marketing, and digital commerce. These investments are driving automation, efficiency gains, cost savings, and enhanced customer engagement, while freeing up organizational capacity to reinvest in innovation and growth.

Globally, performance remains uneven, with strength in North America, parts of Latin America, the UK, and select Asia markets offsetting softness in Europe and China, underscoring the importance of regional agility and diversified growth strategies in a complex macro landscape.

Key Consumer Themes

Macro and Outlook

Companies Broadly Expect a Volatile and Promotionally Competitive 2026, with Persistent Geopolitical and Demand Headwinds Partially Offset by Easing Rates and Moderating Inflation

- Aptiv ($17.0B, Automobile Components): “We navigated changes in geopolitical trends and global trade policies, as well as customer-specific challenges, and delivered earnings growth in the face of FX and commodity headwinds that were significantly larger than we had initially anticipated. As we look ahead to 2026, we expect the macro environment to continue to remain dynamic.”

- Reynolds Consumer Products ($4.8B, Household Products): “As we enter 2026, we anticipate another year of sustained headwinds in 2026, underscoring the need for continued nimbleness, adaptability and focus across the organization. As we move forward, we remain mindful of the state of the consumer environment and the retailer’s focus on inventory management and consumer value. Our insights teams are tracking consumer patterns closely, helping refine our promotional strategy, price pack architecture and innovation priorities to stay nimble as the year unfolds.”

- Clorox ($14.2B, Household Products): “The geopolitical environment, including tariffs, is volatile, particularly in Latin America, and the U.S. market remains sluggish; while we think trends will improve, we’re not building in a big rebound.Because of this uncertainty, we’re giving a wider range than normal in our net sales and organic sales growth guidance to incorporate various levels of category growth.”

- Brunswick ($5.6B, Leisure Products): “The U.S. Fed cut rates by 75 bps over the latter part of 2025, with additional rate cuts anticipated in 2026. While the cuts have reduced financing costs for both dealers and consumers, they came too late in the season to have a material impact on 2025, but will be a tailwind for the 2026 season. Additionally, while the geopolitical and trade environment remains very dynamic, continued equity market strength and the moderating inflation trend are also expected to create a more constructive environment.”

- The Estée Lauder Companies ($35.0B, Personal Care Products): “We remain cautious of potential near-term headwinds, including those from macroeconomic, geopolitical and retailer specific uncertainties though we are encouraged by our momentum and YTD performance.”

- Goodyear Tire & Rubber ($2.9B, Automobile Components): “Even though the overall tariff environment has broadly stabilized in the U.S., overall weak industry conditions continue to affect our global operations in terms of top line and cost. While our Q4 results demonstrate meaningful progress, we anticipate continued volatility as we move into 2026.“

- Taylor Morrison Home ($6.4B, Household Durables): “While there are reasons for optimism, industry-wide inventory levels remain elevated and consumers remain highly attuned to competitive dynamics in the marketplace and are closely weighing incentives, pricing and spec offerings in their purchase decisions. And while affordability has improved over the last year, alongside lower interest rates, wage growth and price discovery, I believe consumer confidence and the broader economic and political outlook will be critical for further demand recovery.”

The Consumer

A Tale of Two Cities with Lower-income Households Pressured, Value-focused, and Trading Down Amid Stretch Budgets and Higher-income Consumers Remaining Relatively Resilient, Reinforcing a Bifurcated and Promotion-sensitive Demand Environment

- McCormick ($18B, Food Products): “The environment across our key markets is marked by volatility and continued pressure from inflation, geopolitical and trade uncertainty and threat of rising unemployment and overall consumer confidence remains low. Consumers, especially low- to middle-income households, continue to make more frequent trips to the store, while purchasing fewer units per trip, a trend that was evident at the start of the year and accelerated through Q4. In addition, consumers continue to stretch meals across multiple occasions and seek affordable ways to prepare fresh home-cooked meals. The consumer continues to show resilience by increasing their demand for value and behaviors that enable them to stretch their budget.”

- D.R. Horton ($45.8B, Household Durables): “We are encouraged by the fact that we’ve still got people out there looking to buy a home. There’s certainly not a lack of interest. I think it’s breaking through consumer confidence and seeing people feel good about their decision to move forward.We are encouraged by the traffic we see. I do believe that if you look at today over last year at this time, there’s a little more balance of inventory.”

- Mondelez International ($77.3B, Food Products): “The consumer confidence is near historic low. They’re worried about overall affordability. They are fed up with the price increases. They don’t feel good about their personal economic outlook. They doubt job security. What we are seeing is that the average shopping basket of the consumer in the U.S., whether you’re in the higher or in the lower social economic classes has not increased for the last 2, 3 years. Within that basket, they have spent more money on the basics, milk, meat, bread and so on. You talked about the K-shaped economy. There is clearly a group of consumers, the more wealthy consumers that do spend differently in the sense that you can see that things like premium and better-for-you are growing within the snacking markets, also some on the go. But the bulk of the consumers are really into value seeking. So what they do is they look for lower unit prices. They look for deals. If they have a bit more money, they will look for bulk packs or multipacks.”

- Clorox ($14.2B, Household Products): “The consumer is largely what we expected it to be. We’re seeing consumers continue to focus on value. We’re seeing them trade… down to smaller sizes. We’ve seen trips increase in the broad market basket in our categories. We’re seeing more stock up behavior, which is normal in our categories. We see consumers moving to more value-oriented channels, but I would say the consumer was largely steady as we had expected and in line with category growth.”

- Hasbro ($13.4B, Leisure Products): “Right now, we continue to see a tale of two cities. The top 20% of households in terms of wealth are really driving a lot of demand and are staying resilient. The lower quintiles of wealth and income, their pennies are pinched. If the economy proves better, if some of the tax refunds that are on tap in the U.S. market proves to be shared out versus like going into the bank account, that could be a boon for us as well.”

- Energizer Holdings ($1.6B, Household Products): “Consumers are continuing to search for value. You are seeing consumers stressed about finances. In light of those dynamics, they’re comfortable switching channels, retailers, brands, pack sizes. So, they’re willing to rotate their purchases to meet their needs. Private label plays a role in the category. In Q1, we did see an increase in private label at certain retailers, as well as some aggressive pricing. This results in volume growth for those retailers but actually erodes category value at the same time. And our view is this is all about balance, and we’ve already seen some retailers recalibrate their approach and bring more balance to both private label value and premium equation.”

Tariff Impact

A Still-fluid Environment Remains a Meaningful and Volatile Cost Headwind Entering 2026, Pressuring Margins and Demand; Companies Relying on Pricing, Supply Chain Diversification, and Cost Actions to Partially Offset the Impact

- McCormick & Co ($18.0B, Food Products): “In terms of tariffs, recent reductions are a positive step from a cost standpoint. However, ~50% of the incremental tariffs on McCormick items remain in place and we continue to face related inflationary pressures. Our pricing actions have been surgical. We took pricing actions to offset inflation, but we have not fully passed through tariff costs.”

- SharkNinja ($16.0B, Household Durables): “As we look at the 1H26, we will be normalizing tariffs as we go into the year. And having them come through the P&L in a way that we didn’t have last year in 1H. We didn’t really start to see those flow into our P&L until Q3 a bit and then into Q4. So the 1H, we expect a decent gross margin headwind driven by tariffs with slight offsets, driven by all the cost optimization efforts.”

- Harley-Davidson ($2.4B, Automobiles): “In 2025, the global tariff environment was more volatile and uncertain than we had expected at the beginning of the year. In Q4 of 2025, the cost of new or increased tariffs was $22M, and for the full year of 2025, the cost of new or increased tariffs was $67M. This included direct tariff exposure, Harley-Davidson importing and exporting product, as well as indirect tariff exposure from suppliers. This excluded pricing mitigation actions as well as operational costs relating to new or increased tariffs. Harley-Davidson is a business very centered in and around the U.S. Three of our four manufacturing centers are U.S.-based. We also have a U.S.-centric approach to sourcing with ~75% of component purchasing coming from the U.S. We have a number of actions underway to mitigate the impact, and we expect this situation will remain fluid given the uncertainty that still exists.”

- Newell Brands ($1.9B, Household Durables): “While we do not typically provide explicit gross margin guidance, it may be helpful to provide some context since tariff impacts will not fully annualize until Q2’26. The tariff environment remains dynamic, as we have consistently communicated, tariffs pressure demand and price competitiveness in impacted categories and create short-term cash and P&L headwinds. In 2025, the total gross cash tariff impact was $174M and the total gross P&L impact before offsetting actions was $114M. For 2026, our current outlook assumes a total gross cash tariff impact of $130M, with an estimated total gross P&L impact of $150M. On a P&L basis, that implies roughly $0.30 of headwind in 2026, which on a YoY incremental basis is $0.07 more than 2025.”

- General Motors ($75.3B, Automobiles): “Starting with tariffs, we anticipate gross tariff costs in the $3B to $4B range, slightly higher than 2025 due to an additional quarter of tariff exposure, partially offset by the reduced Korea tariff and expanded MSRP offset program. For Q1, we expect the gross tariff impact to be in the $750M to $1B range, which is well below the quarterly impact in Q2 and Q3 of 2025, but more than Q4. The higher quarterly run rate in 2026 versus Q4 2025 is largely driven by the timing of tariff costs, which can be lumpy, particularly as it relates to the supply chain. The team did a great job offsetting over 40% of our gross tariff costs in 2025 through go-to-market strategies, footprint changes and cost efficiencies.”

- Ingredion ($7.5B, Food Products): “It is also worth highlighting that despite the volatile trade and tariff environment in 2025, Ingredion was minimally, directly impacted. This was due to the fact that more than 80% of our production is locally made and locally sold.”

- Mattel ($6.6B, Leisure Products): “For the full year, gross margin was 48.9%, a decline of 200bps. The same factors that impacted the fourth quarter gross margin impacted our full year gross margin…higher discounting, inflation and foreign exchange, as well as the timing lag between pricing actions and the recognition of tariff costs in the P&L. However, pricing and other mitigating actions fully offset tariff costs on a full-year basis as the benefits of those actions were realized over time. Mitigating actions included accelerating the diversification of our supply chain, optimizing product sourcing and product mix, and selective pricing actions.”

Expense Management

Continued Emphasis on Structural Cost Reduction and Productivity Initiatives is Driving Meaningful Savings, Funding Growth Investments, and Helping Offset Inflation, Pricing Pressure, and Tariffs

- Reynolds Consumer Products ($4.8B, Household Products): “We delivered cost savings through productivity initiatives, strategic sourcing and disciplined cost management, and we invested in a number of high ROI initiatives across our business, including capital to support growth in our fastest growing segments, as well as making solid progress against our automation pipeline.”

- Philip Morris International ($283.3B, Tobacco): “We also continued to invest in expanding our U.S. capabilities to capture the substantial growth opportunities This performance was supported by a relentless focus on both cost of goods sold and back-office efficiency, enabling meaningful margin expansion even as we continue to invest for growth. We have delivered around $1.5B in gross cost savings since 2024, placing us firmly on track to achieve our $2B objective for the 2024-2026 period.”

- Brunswick ($5.6B, Leisure Products): “We continue to be laser-focused on structural cost reduction actions, but we are and have accelerated some investments in new products and technology, notably in propulsion.”

- Lear ($7.1B, Automobile Components): “We expect overall company adjusted margins to improve by 10 bps, driven by strong net performance and our margin accretive backlog. Positive net performance primarily reflects the benefits from our IDEA by Lear [operational] initiatives and savings from restructuring actions with wage inflation, customer contractual price reductions, and higher launch and engineering costs, largely offset by material cost reductions from our suppliers, cost technology optimization, commercial recoveries and normal plant efficiency programs.”

- Marriott International ($87.6B, Hotels, Restaurants & Leisure): “In 2025, the company benefited from over $90M of above-property cost savings related to our enterprise-wide initiative to enhance productivity across the company that is also yielding cost savings to our owners.”

- Hasbro ($13.4B, Leisure Products): “The 2026 outlook assumes ~$150M of gross cost savings from initiatives across supply chain, including the manufacturing diversification efforts as well as a continuation of our transformation in several areas impacting operating expense. Our cost transformation efforts contributed over $175M in gross savings across supply chain, product development, and operating expenses, driving margin expansion and helping to offset the impact from tariffs. Through 2025, we have delivered almost $800M of gross cost savings and are well on our path to the $1B commitment.”

AI & Digital Acceleration

Companies Continue to Expand AI Deployment to Drive Automation, Efficiency, Cost Savings, and Enhanced Customer Engagement Across Supply Chain, Operations, and Digital Commerce

- Procter & Gamble ($368.6B, Household Products): “Supply Chain 3.0 has driven a more complete system connection from purchase signal back through inventory systems to our production planning and material ordering to ensure consumers find the product they want each time they shop. We are freeing up capacity and capabilities with the organization redesign we announced as part of the restructuring in June. We have built a structured data lake stocked with petabytes of relevant data. We have built data platforms, AI capabilities, programmatic shelf tools, and media creation and evaluation systems. We have supply chain platforms that can run autonomously reacting to retail demand signals, consumer innovation needs, or productivity opportunities faster than ever before.”

- General Motors ($75.3B, Automobiles): “AI, machine learning, and robotics are also driving safety, quality and speed in our manufacturing plants so we can get great products and technologies into the hands of customers faster. We are also deploying robotic systems alongside humans to make their jobs safer and easier to perform.”

- Amazon ($2390.6B, Broadline Retail): “The stores team is also continuing to innovate and deliver for customers with AI. Our Agentic AI shopping assistant, Rufus, has rapidly expanded. Rufus can research products, track prices and auto buy, purchasing a product in our store when it reaches your set price. It can also now shop tens of millions of items in other online stores and make purchases for customers using our Agentic Buy for Me feature. Last year, more than 300M customers used Rufus. In addition, customers use Lens, our AI-powered visual search tool to find products with a phone camera, a screenshot or a barcode, and they did it 45% more YoY.“

- Taylor Morrison Home ($6.4B, Household Durables): “We are doubling down on innovation across the organization. From the sales floor to purchasing, land due diligence, financial services and back office functions, we have made significant strides in deploying our proprietary digital sales tools to reduce friction during the customer journey and AI-enabled processes to enhance efficiency and manage costs. For example, we have developed a proprietary AI-powered platform that today houses digital tools and AI agents spanning purchasing, sales, customer service, financial services, and employee resources.”

- Hasbro ($13.4B, Leisure Products): “We’re taking a human-centric, creator-led approach. AI is a tool that helps our teams move faster and focus on higher-value work, but people make the decisions and people own the creative outcomes. Teams also have choice in how they use it, including not to use it at all when it doesn’t fit the work or the brand. We’re beyond experimentation. We’re deploying AI across financial planning, forecasting, order management, supply chain operations, training, and everyday productivity, under enterprise controls and clear guidelines around responsible use and IP protection. We’re partnering with best-in-class platforms, including Google Gemini, OpenAI, and ElevenLabs, to embed AI into workflows where it adds real value. The impact is tangible. Over the next year, we anticipate these workflows will free up more than 1 million hours of lower-value work. And we’re reinvesting that capacity into innovation, creativity, and serving fans.”

- Coty ($2.8B, Personal Care Products): “Our AI journey is accelerating and we’re already putting real foundations in place, though it’s just the tip of the iceberg of what AI can do for our business. Building on our strong, sizable AI partnerships with Microsoft and ServiceNow, our new strategic collaboration with OpenAI expands our AI ecosystem to support focused applications, including advanced consumer persona insights. We’re actively creating digital assets using generate AI, helping us reduce spending, compress timelines, and generate more content. While still in the early stages of implementation, through AI, we’ve reduced the post-production asset costs for select fragrance, cosmetics and skincare brand by 70% to 90%.”

Around the World

Regional Performance Remains Uneven; Strength in North America, Parts of LatAm, the UK, and Select Asia Markets with Ongoing Softness in Europe and China amid Broader Macro and Discretionary Spending Pressures

- Aptiv ($17.0B, Automobile Components): “In North America, revenue grew 8%, with double-digit growth in both Intelligent Systems and EDS. In Europe, revenue was down 1%, in line with vehicle production in the region and relatively comparable across our segments. And in China, revenue was down 5%, reflecting the continued impact of unfavorable mix. That being said, our performance versus the market in China improved further this quarter, a positive sign as the team works to further enhance our customer mix. And of note, ~80% of our China new business awards in 2025 were from the local OEMs.”

- Ingredion ($7.5B, Food Products): “Mexico specifically demonstrated resilience to offset challenging unforeseen economic conditions, delivering another record year of operating income.”

- PepsiCo ($229.0B, Beverages): “Middle and low-income consumer that continues to be stretched and choiceful and that we have to earn being part of their basket every day. That’s how we’re thinking about it for the U.S. We’re seeing different parts of the world behaving differently, but we’re optimistic about Mexico. We’re seeing positive trends in China. I’m referring to our business and the surroundings of our business rather than larger macros. We’re seeing positive situation in the Middle East. We’re seeing a good consumer there as well. A bit weaker in Western Europe. And then Brazil kind of neutral.”

- SharkNinja ($16.0B, Household Durables): “The UK delivered another strong quarter with over 9% YoY growth, while EMEA saw robust results across multiple geographies and channels. Our Latin America business also performed exceptionally well. In Mexico, we believe triple digit growth underscores the strength of our momentum and the exciting opportunities The success that we’re seeing across Latin America is fueling consumer interest for our products and places we don’t currently sell, like Ecuador and Peru. In 2026, we’re focusing more attention on expanding our reach by ramping a new partnership with the dominant e-commerce players in the region.”

- Harley-Davidson ($2.4B, Automobiles): “North American retail was up YoY, while international retail, particularly in EMEA, was softer than we expected. The choppiness and volatility in global retail results is a continuation of what we have observed since mid-2024 with a difficult global backdrop in big-ticket discretionary Pricing continues to be on the top of customers’ minds given the current global setup that includes inflationary pressures and interest rates that continue to run above recent historical lows. In EMEA, Q4 retail sales declined by 24%, driven by weakness across the region and different bike families. EMEA continued to be adversely impacted by overall macroeconomic conditions. In Asia Pacific, Q4 retail sales declined by 1%, which was a significant improvement from the 1H25 and mostly attributed to a continued challenging environment in China, which was down meaningfully. The Q4 retail sales included positive results in Japan and Asia emerging markets. In Latin America, Q4 retail sales increased by 10%, where both Brazil, our largest Latin American market, and Mexico were up, while other Latin American countries were down modestly YoY.”

- Levi Strauss & Co ($7.8B, Textiles, Apparel & Luxury Goods): “The Americas net revenues were up 2%. Our U.S. Direct-to-Consumer (DTC) business grew 6%, driven by strength in both brick-and-mortar and e-commerce. Our LATAM business was up 8%, fueled by growth across most markets and continued strength in DTC. Europe net revenues accelerated 10% in Q4, led by double-digit growth in our largest European markets, the UK and Germany. Asia net revenues grew 4% YoY, fueled by strong DTC performance. Key markets, including Japan and Turkey, delivered double-digit growth this quarter as the head-to-toe lifestyle offerings continue to resonate with consumers and drive growth.”

In Closing

Overall, management commentary points to a 2026 operating environment that rewards agility and execution over macro-driven growth. With consumer confidence still fragile and demand increasingly dependent on value and promotions, and tariffs continuing to create cost volatility and margin pressure, companies are planning conservatively and staying focused on controllables – this is particularly noticeable in staples companies who widened guidance ranges relative to last year. Disciplined pricing, sharper assortment and pack/price strategies, supply chain adjustments, and tighter alignment with retailers are central to navigating ongoing trade uncertainty and competitive intensity.

At the same time, the path to earnings resilience is being shaped by two parallel levers. First, sustained cost transformation and structural productivity initiatives are helping protect margins and fund targeted investment even as tariffs and other external costs remain a headwind. Second, scaled AI and digital deployment is becoming a meaningful differentiator, improving speed, efficiency, and customer engagement across the value chain.

The setup suggests continued dispersion in outcomes, with the strongest performers likely to be those that combine cost discipline with innovation and regional flexibility while navigating a still-volatile global backdrop.

When growth returns, rightsized cost bases coupled with smarter, automated, digitally-enabled operations should yield powerful operating leverage. The downturn will not be for naught

Up next week: Materials in our Sector Beat.