This Week in Earnings – Q3'25

Consumer Discretionary Sector Beat

Our thought leadership this week addresses:

- Key Events

- Earnings Snap, covering the S&P 500 stats to date

- In Focus: Layoffs

- Spotlight on Consumer Discretionary in The Sector Beat

Key Events

Monetary Policy

- The Federal Reserve lowered its benchmark interest rate by 25 bps to 3.75% to 4.00%, in a move that was widely expected by markets. The Fed noted that economic activity continues to expand at a moderate pace, while job gains have slowed, and unemployment remains low. Inflation has risen since earlier in the year and remains elevated. The Fed also announced plans to end quantitative tightening on December 1, 2025. (Source: The Federal Reserve)

- The Bank of Canada lowered its overnight rate by 25 bps to 2.25%, with the Bank Rate at 2.5% and the deposit rate at 2.20%. According to its Monetary Policy Report, the Canadian economy is adjusting to steep U.S. tariffs and heightened uncertainty. The report highlights that the trade conflict’s impact on growth and inflation has become increasingly evident, with exports to the U.S. and business investment both declining. It also notes growing uncertainty around global trade dynamics, demographic shifts, and AI adoption. (Source: Bank of Canada)

Trade/Tariffs

- Following their meeting in South Korea, Presidents Trump and Xi agreed to extend the U.S.–China trade truce. As part of the agreement, China will postpone export controls on rare earths for one year, while the U.S. will reduce the fentanyl tariff rate from 20% to 10%, bringing the average tariff on Chinese imports down to 45%. (Source: Bloomberg)

Consumer Confidence

- The Consumer Confidence Index decreased 1 point to 94.6 this month. Senior Economist at The Conference Board highlights that, “Consumers’ write-in responses were led by references to prices and inflation, which continued to be the main topic influencing consumers’ views of the economy. References to tariffs declined further this month but remained elevated. Mentions of jobs and employment eased somewhat after picking up in September. The write-in comments remained mostly negative overall, but less so than in previous months. References to U.S. politics were up notably, with the ongoing government shutdown mentioned multiple times as a key concern.” (Source: The Conference Board)

ADP Private-Sector Employment

- With the U.S. government shutdown delaying official economic data, the ADP National Employment Report provides timely insight into private-sector labor market conditions. In September, ADP reported a decline of 32,000 private-sector jobs, driven largely by losses in service industries, particularly leisure and hospitality (-19,000), other services (-16,000), professional and business services (-13,000), and financial activities (-9,000). This contrasts with August, when the private sector added 54,000 jobs, led by gains in service-providing industries such as leisure and hospitality (+50,000) and professional and business services (+15,000). This shows an ongoing shift in job growth and emerging constraints on opportunities across key service industries. (Source: ADP National Employment Report)

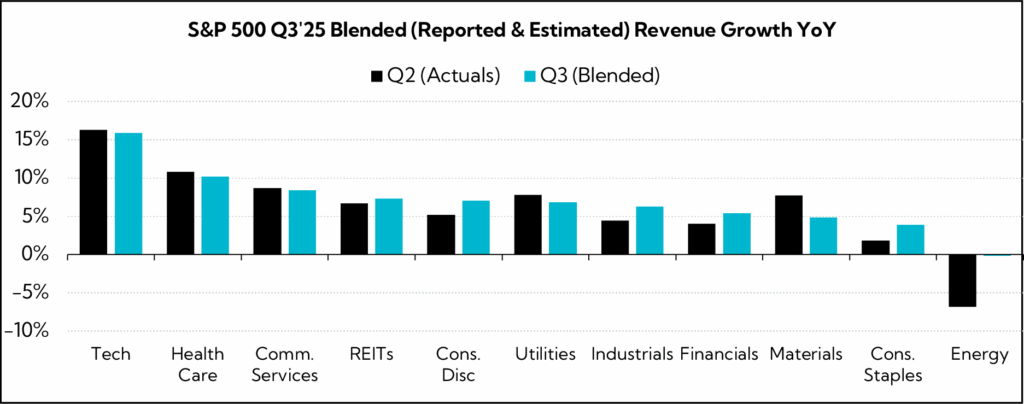

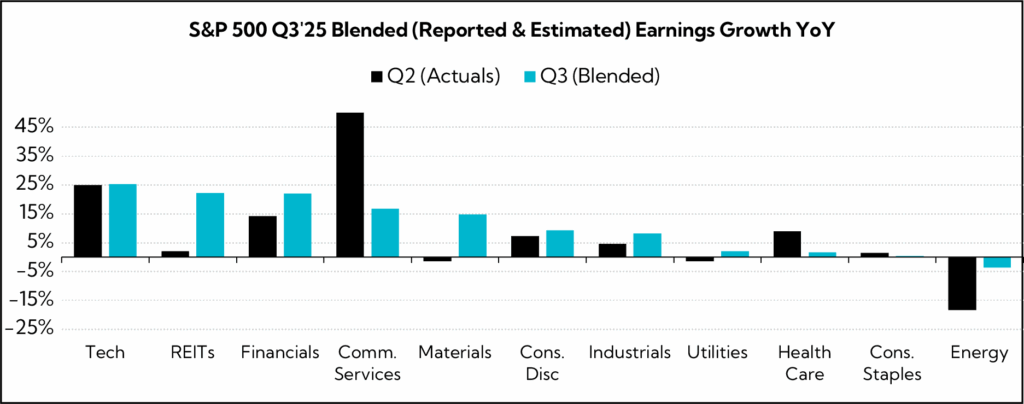

S&P 500 Earnings Snap

63% of the S&P 500 has reported earnings to date

Q3'25 Revenue Performance

- 80% have reported a positive revenue surprise, above both the 1-year average (62%) and the 5-year average (70%)

- Blended revenue growth (combines actual reported results for companies and estimated results for companies yet to report) is 7.5% vs. 6.4% in Q2; excluding the Energy sector, the earnings growth estimate is 8.2% vs. 7.6% in Q2.

- Companies are reporting revenue 2.2% above consensus estimates, well above the 1-year average (+0.9%) and modestly above the 5-year average (+2.1%)

Q3’25 EPS Performance

- 83% have reported a positive EPS surprise, above both the 1-year average (77%) and the 5-year average (78%)

- Blended earnings growth (combines actual reported results for companies and estimated results for companies yet to report) is 13.8% in line with Q2; excluding the Energy sector, the earnings growth estimate is 14.7% vs. 15.7% in Q2.

- Companies are reporting earnings 8.3% above consensus estimates, above the 1-year average (+6.3%) and below the 5-year average (+9.1%)

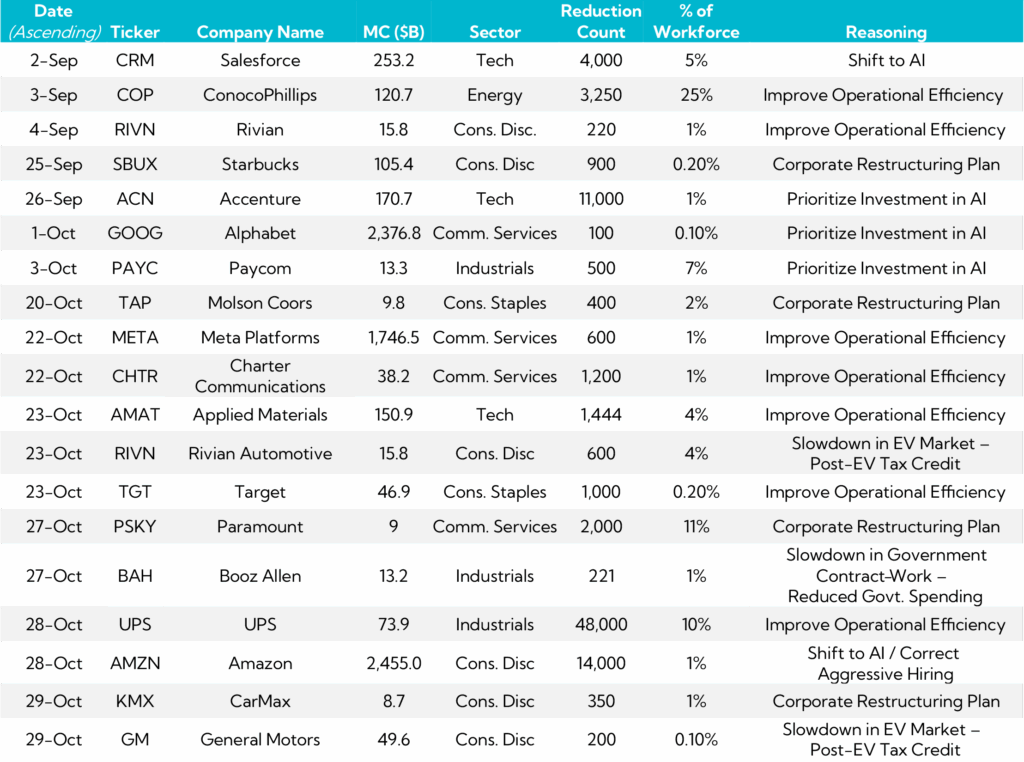

In Focus: Layoffs

Over the past two weeks, a number of major companies have announced significant workforce reductions as part of broader efforts to cut costs, boost efficiency, and align with strategic priorities like AI investment and corporate restructuring. Perhaps most notable was Amazon’s standout announcement to eliminate approximately 14,000 corporate jobs globally, with an expected overall reduction of up to 30,000 (10% of AMZN’s corporate workforce!).

The layoffs are not simply reactive but also proactive as companies cite weaker demand, shifting consumer patterns, and the necessity to restructure around efficiency and digital transformation. They are also responding to slowing workloads and contractual pressures in addition to cost containment.

These announcements reflect a dual focus: reducing headcount and operational complexity while reallocating resources toward newer growth areas and technology, specifically AI.

Below, we’ve compiled some of the most noteworthy layoff disclosures announced within the last two months, the majority of which are from Consumer Discretionary, Communication Services, and Tech companies:

The Sector Beat: Consumer Discretionary

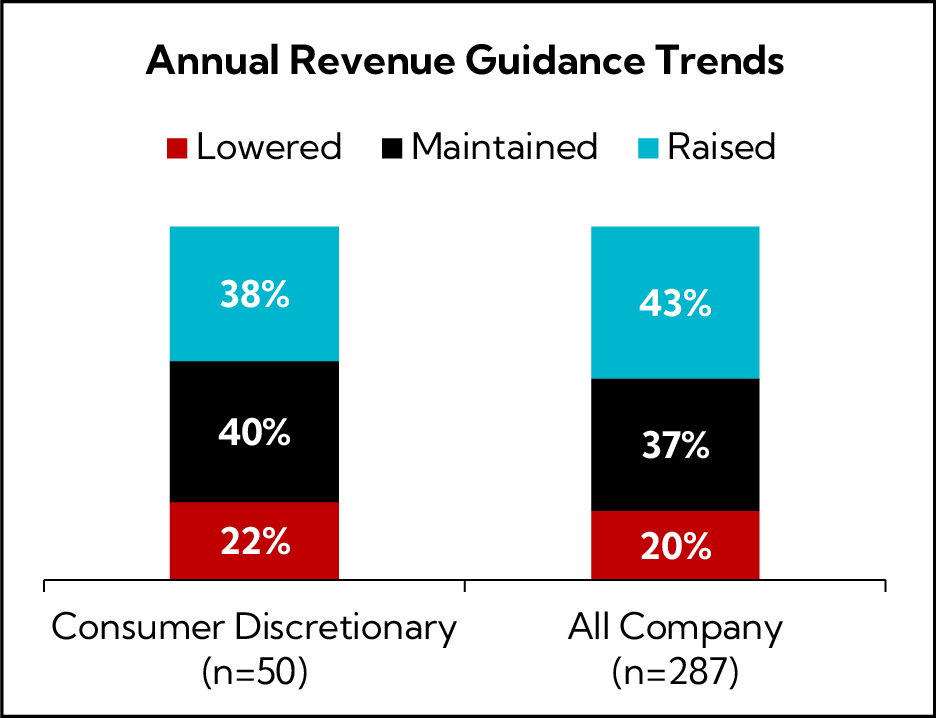

Consumer Discretionary Guidance: Initial Trends

At the beginning of each quarter, we analyze annual revenue and EPS guidance provided by U.S. Consumer Discretionary companies with market caps greater than $1B that have reported to date. Below are our findings. For comparison purposes, we provide an “All Company” benchmark, which tracks a basket of U.S. companies1 across all sectors that have reported earnings to date (n = 307).2

Guidance Breakdown by Industry

| Industry | Number of Companies |

|---|---|

| Specialty Retail | 13 |

| Automobile Components | 10 |

| Hotels, Restaurants & Leisure | 9 |

| Textiles, Apparel & Luxury Goods | 6 |

| Diversified Consumer Services | 5 |

| Household Durables | 5 |

| Distributors | 3 |

| Leisure Products | 3 |

| Broadline Retail | 2 |

| Automobiles | 1 |

| Total | 57 |

Source: Corbin Advisors

Revenue Guidance

To date, 40% of Consumer Discretionary companies have Maintained their annual revenue guidance, slightly above the All-Company benchmark. However, slightly fewer, 38%, have Raised guidance relative to the basket, though still well above the 22% who have Lowered annual forecasts.

- Companies that Lowered guidance (n = 11)

- Average midpoint of -0.8% growth versus 1.4% last quarter

- Average spread decreased by 20 bps to 1.8%

- Companies that Maintained guidance (n = 20)

- Average midpoint of 4.4% growth

- Average spread of 6%

- Companies that Raised guidance (n = 19)

- 12 companies raised the top and bottom of the original range, 5 raised the bottom, and 2 lowered the top but raised the bottom (i.e., increased midpoint)

- Average midpoint of 5% growth versus 4.6% last quarter

- Average spread decreased by 150 bps to 8%

- Overall midpoints assume 4.3% annual growth, on average, versus 4.0% last quarter

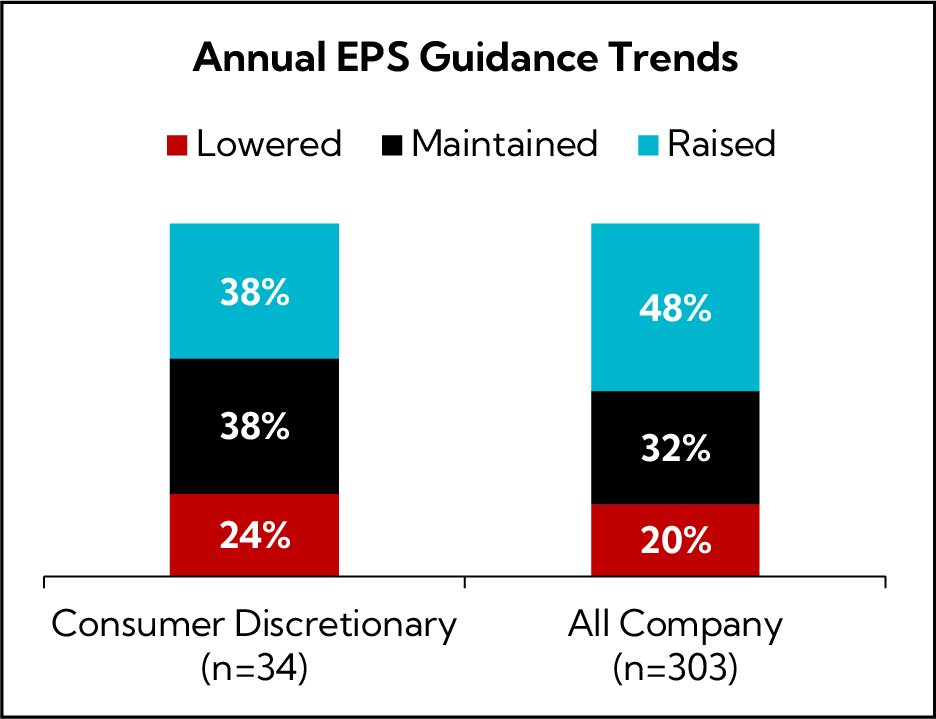

EPS Guidance

An equal share, 38%, of Consumer Discretionary companies have either Maintained or Raised annual EPS guidance, diverging from the All-Company benchmark where an additional 10% increased their estimates heading into the final calendar quarter. Meanwhile, 24% of Consumer Discretionary companies Lowered, slightly above the All-Company benchmark of 20%.

- Companies that Lowered guidance (n = 8)

- Half of the companies lowered the top and bottom of the original range, the other half only lowered the top.

- The average spread decreased from $0.30 to $0.21

- Companies that Maintained guidance (n = 13)

- Average spread of $0.31

- Companies that Raised guidance (n = 13)

- Nearly all companies raised the top and bottom of the range; 2 companies raised the bottom, but lowered the top

- Average spread decreased from $0.49 to $0.26

Earnings Call Analysis

We analyzed the earnings calls for this group and the broader Consumer Discretionary universe to identify key themes.

With more than three quarters of the year behind us, companies are closing out 2025 and highlighting entering 2026 with cautious optimism, reflecting an environment of persistent macro uncertainty but gradual stabilization. Across categories, executives cite the positive direction of travel regarding interest rates but also increasing inflationary pressures and mounting tariffs as key variables shaping demand and consumer sentiment. For homebuilders, affordability constraints continue to weigh on sales, though lower rates could provide relief and unlock pent-up demand. Meanwhile, some retailers suggest the consumer environment is bottoming out rather than worsening.

Indeed, while Consumer Discretionary companies are delivering Q2 beats at a healthy clip, our analysis finds most of the sector maintaining full-year Revenue and EPS guidance. Still, more companies have raised guidance than last quarter, though below the All-Company benchmark.

Tariffs remain a defining theme across the landscape, with companies actively mitigating headwinds through pricing, supply chain diversification, and onshoring or reshoring while waiting on “clear rules of engagement”. Import-reliant companies are absorbing near-term cost pressures while executing long-term strategies to spread sourcing risk and reduce dependence on China. Conversely, domestic manufacturers view the current tariff environment as a competitive advantage, reinforcing their strong U.S. production bases. While tariffs continue to add operational complexity, most companies express confidence that mitigation playbooks will offset structural cost impacts over time.

The consumer is cautious but resilient, echoing the sentiment by Big Banks. The dichotomy between income levels continues, with higher-income consumers willing to spend selectively on premium experiences, while middle- and lower-income households are showing signs of value-conscious trade-down behavior. Overall, sentiment remains cautious but not collapsing — consumers are still spending, but with greater scrutiny.

Across the board, companies are driving efficiency and margin improvement through disciplined cost control, restructuring, and lean initiatives. While all are optimizing pricing, some are also pursuing multi-year transformation programs to lower structural costs and expand margins. Simultaneously, the sector is accelerating AI and digital adoption. Companies are integrating with OpenAI, building AI powered chatbots, leveraging agentic AI, and deploying advanced tools to automate workflows, enhance customer interactions, and unlock productivity gains.

Globally, performance remains uneven. While U.S. consumers remain more resilient, internationally, Asia (sans China) is leading growth with strong momentum in India, Japan, and Korea, while Europe continues to face pricing pressure and soft demand.

Key Consumer Discretionary Themes

Macro & Outlooks

Cautious Optimism Remains as We Look Ahead to 2026, Reflecting a Mixed Macro Backdrop Defined by Persistent Uncertainty but Emerging Stabilization; Tariff Volatility and Inflation Pressure On One Side and Interest Rate Direction On the Other Influence Demand and Consumer Sentiment

- Tractor Supply ($30.6B, Specialty Retail): “We see AURs continuing to be in a positive scenario the back half of this year and going into 2026. In general, the consumer continues to engage in the lifestyle. We have a solid demand for our core business.”

- Brunswick ($3.9B, Leisure Products): “While the trade and economic environment remains extremely dynamic, we believe that we are well-positioned to benefit from any industry recovery due to the operating leverage inherent in our businesses. Our tariff mitigation strategies are working to reduce our net exposure. And we believe that our substantial, vertically integrated U.S. manufacturing base positions us relatively well in an environment of persistent tariffs. Interest rates are coming down with further cuts expected, reducing the cost of financing for both end consumers and dealers, as we approach the fall boat show season and the restocking cycle for what we anticipate at the moment to be a modestly stronger 2026.”

- Genuine Parts ($18.4B, Distributors): “As I think about how 2026 could set up, I think we’re in a similar dynamic to a year ago. Everyone was waiting on the outcome of an election. We got election resolution and clarity, and we started the year 2025 with a bit more optimistic outlook. As we find ourselves at the end of 2025, we sit in a similar place. There’s a lot of folks sitting on the sidelines, not around an election, but more around what’s going to happen with interest rates and how do we get some good clear rules of engagement on tariffs. If we got that in the fourth quarter, I think you could see a trading environment in 2026 that would be a little bit more robust.”

- Wayfair ($8.5B, Specialty Retail): “The industry backdrop is getting better. It is no longer getting worse at a fast rate. If you think about multiple years of double-digit declines, that means that you’ve come pretty far off of where you were. And if you take the trend back to pre-COVID, we’re quite far off what the long-term trend had been. What’s happening now? It’s no longer declining at that type of rate. We think it’s more like flattish. It came off a high, it broke trend, and then it basically has bottomed out.“

- Dorman Products ($3.7B, Automobile Components): “Looking across the Light Duty market, macro trends continued to remain positive with vehicle miles traveled increasing YoY. However, uncertainty in the market related to tariffs and trade dynamics continues to persist. We’re closely monitoring the environment and continue to work with our suppliers and customers as part of our overall tariff mitigation strategy. While it appears that inflationary pricing has started to reach our end-users, we remain confident in our ability to drive long-term growth as nondiscretionary repair parts have historically performed well through various economic cycles.”

- PulteGroup ($22.4B, Household Durables): “From a sales standpoint, we are now in the seasonally slowest part of the year, but we remain optimistic that lower rates in combination with strong economy and higher confidence can ultimately work to energize new, and just as importantly, existing home sales. Demand within [the] existing home market remains soft, resulting in elevated levels of inventory. The extent the lower rates can revitalize existing home sales it will be a positive for U.S. housing.”

- Leggett & Platt ($1.3B, Household Durables): “Throughout the quarter, we continue to navigate a very dynamic environment. We still believe tariffs will be a net positive for us, but remain concerned that wide-ranging tariffs could drive inflation, hurt consumer confidence and pressure consumer demand. We are actively mitigating some of the negative impacts experienced in a few of our businesses, such as supply chain disruptions that can have an indirect impact on us and our customer demand disruptions.”

Tariffs

Companies are Deploying Mitigation “Playbooks” To Offset Tariffs, Including Pricing, Supply Chain Diversification, and Product Localization Tactics with Near-term Cost Pressures Expected to Ease Over Time; Domestic Manufactures View Tariffs as an Advantage

- Hasbro ($10.7B, Leisure Products): “The tariff pressure in Q3 was roughly a $20M cost. As we look into Q4, there’s a bit more, so it’s a bit of a heavier quarter. The net impact is going to be about $60M within 2025. As we look into 2026, we are fully running our tariff playbook. As we calculate the various scenarios of where that absolute rates will play out, we’re really putting all of our levers to work from how we think about pricing, our product mix and our supply chain, and how we’re managing all of our operating expenses to mitigate and offset the impact.“

- Polaris ($3.0B, Leisure Products): “Our gross tariff impacts for the year rose by $10M since July, driven by international retaliatory policies and increased commodity exposure. Despite this, given deferrals and mitigating actions, we don’t expect a material change to our 2025 P&L outlook and now expect the impact from new tariffs to be approximately $90M. We’re executing our mitigation strategies effectively with an urgent focus on our China spend, with a long-term plan to drastically reduce our spend on all China parts and components. By the end of 2027, we expect our actual China spend to be down by approximately 80% relative to 2024, which equates to less than 5% of our cost of goods sold coming from China.”

- Whirlpool ($4.7B, Household Durables): “Tariffs come in various forms and have been slowly ramping up during Q3. The full burden of reciprocal tariffs, which were announced on August 7, only became effective as of October 5, and are now finally fully in place. This ramp-up brought extensive preloading of inventories ahead of tariffs. And while this is not a surprise, it lasted longer than we anticipated. Regardless of these temporary impacts, the fundamental perspective on tariffs remains the same. We are the domestic producer with more than 80% of our U.S. sales produced in the U.S., while our competitors are largely importers. Tariffs, by definition, support domestic producers.”

- Leggett & Platt ($1.3B, Household Durables): “Our teams are actively engaged with customers and suppliers across our global footprint to reduce tariff exposure and minimize impacts. In general, import issues are an ongoing risk, especially for our Bedding Products segment, but we are encouraged that some recent enforcement actions support fair competition for domestic manufacturers and importers alike. Now more than ever, misclassification of shipments and understated product values are additional problems that domestic manufacturers face when competing against imports. While we continue to believe that imports have a role in the S. bedding market, the domestic industry must be able to compete on a level playing field.”

- Ford Motor ($43.3B, Automobiles): “I’d like to thank President Trump and his team for the recent tariff policy developments, which are favorable to Ford as the most American auto manufacturer. Credit based on our large U.S. manufacturing volume will allow us to offset tariffs on imported auto parts we need for our strong American production and manufacturing base. In addition, tariffs leveling the playing field for those imported medium and heavy-duty trucks is a positive for Ford because we are no longer disadvantaged for building every single one of our Super Duty’s here in the United States.“

- Deckers Outdoor ($16.4B, Textiles, Apparel & Luxury Goods): “As a result of our price increases being implemented at the beginning of July in combination with actions to bring additional inventory in ahead of increased tariff rates being implemented, we saw a slight delay in the net headwind of tariffs and did not experience a meaningful negative impact in Q2 compared to the prior year result. However, this is unique to Q2 and our expectation of net tariff headwinds in the back half of fiscal year remains largely unchanged. We now expect the unmitigated tariff impact on FY26 to be approximately $150M. Further, we now estimate that our mitigation efforts for this fiscal year will offset approximately $75M to $95M of this pressure, including benefits from select, strategic, and staggered pricing increases as well as partial cost sharing with factory partners.”

- Mohawk Industries ($7.3B, Household Durables): “Our industry is currently at various stages of passing through the impact of higher tariffs on imported products and should compensate for increased product cost over time. We’re managing the impacts of tariffs on our U.S. imported product offering through pricing actions and supply chain optimization, and we are reinforcing the value of our domestic manufacturing.”

The Consumer

Cautious but Resilient, Prioritizing Essentials and Value while High-income Consumers Selectively Spend on Premium Experiences; Overall Sentiment Hinging on Improving Confidence and Rate Stability Heading Into 2026

- Wayfair ($8.5B, Specialty Retail): “As it relates specifically to brand and income, we are seeing strength in higher-end brands, and that’s been for quite some time. Perigold, which is our luxury brand, and the specialty retail brands – all operate at a higher average order value, higher price points – have seen some really nice strength, which I think is consistent with what others have seen from consumers; that the higher-income consumer has held in a bit better.“

- Cheesecake Factory ($3.3B, Hotels, Restaurants & Leisure): “Sometimes what we’ve seen in these environments is you do get trade down even from those that are being insulated based on sentiment [higher end consumer]. They may still have a job and a good income, but for whatever the reasons are, things are going down, they are still going out to eat and still spending, which would give you a positive read on their overall spend profile. But they may be taking it down a notch to a slightly lower price point experience.”

- O’Reilly Automotive ($84.4B, Specialty Retail): “We are still in the early stages of the consumer response to the ramp-up in price levels. It can be difficult to parse too finely the initial response from our DIY customers, but the pressure we have seen thus far is modest and in line with consumer reactions to economic shocks we have seen in the past. We remain cautious in our outlook on the consumer and expect that we could continue to see a conservative stance from consumers in how they manage spending in this environment. However, even in this environment, our DIY consumers are still showing a willingness to invest in and maintain their vehicles, and we believe any potential deferral pressure will be short term.“

- Mohawk Industries ($7.3B, Household Durables): “Across our geographies, consumer uncertainty continues to limit discretionary spending on large projects, particularly if financing with debt is required. Postponement of large renovation projects and declining home sales have been the primary driver of weakness in residential remodeling during the current cycle, while the commercial sector has remained stronger.”

- Amazon ($2455.0B, Broadline Retail): “Everyday Essentials continues to grow quickly and, year-to-date, is growing nearly twice as fast as the rest of the business. We remain committed to staying sharp on price and meeting or beating prices of other major retailers.”

- Pool ($11.7B, Distributors): “Uncertainty around tariffs and elevated borrowing rates continue to weigh on consumer sentiment and limit discretionary demand, particularly for pool projects that require financing.”

- Booking Holdings ($181.9B, Hotels, Restaurants & Leisure): “We saw the booking window in the U.S. normalize in Q3, which is also an encouraging improvement from Q2. That said, in the U.S., we continue to see slightly lower Average Daily Rates and a shorter length of stay versus the prior year, which may indicate that some S. consumers are continuing to be thoughtful on their discretionary spending.“

- Taylor Morrison Home ($5.9B, Household Durables): “Even though these generally well-qualified buyer groups are less sensitive to affordability constraints, all consumer segments have been impacted by macroeconomic and political uncertainty, which has weighed on buyer urgency and shopper sentiment. In addition, consumers are aware of the current competitive dynamics in the marketplace and are carefully weighing available incentives, pricing and spec offerings in their purchase decisions.”

Margin & Cost

Companies Driving Margin Expansion through Disciplined Cost Control, Operational Efficiencies, and Restructuring…Including Headcount Reductions; Executives Positioning for Steadier Profitability Despite Ongoing Macro and Tariff Headwinds

- Gentex ($5.9B, Automobile Components): “The ongoing improvement in gross margin reflects the company’s disciplined focus on cost control and productivity improvements. However, the gross margin was negatively impacted by ~90 bps due to incremental tariffs in the quarter that were not offset through customers. Despite the incremental impact of tariffs on our business, the company has improved the overall gross margin to levels not seen in several years.“

- Polaris ($3.0B, Leisure Products): “We continue to manage costs carefully and drive lean and operational efficiencies across our business to exceed our goal of $40M in structural operational efficiencies this year. Some examples of these efficiencies include lower labor costs, driven by lean activities that have increased efficiency and improved material flow in all areas of the plant. We’re still in the early stages of lean deployment, which gives me great confidence in the efficiencies we have in front of us.”

- Booking Holdings ($181.9B, Hotels, Restaurants & Leisure): “During Q3, we realized approximately $70M of in-quarter savings from the Transformation Program, primarily in sales and other expenses and in personnel expenses. We also took further actions during the quarter to advance certain efficiency initiatives into the implementation phase. And as a result, we now estimate in-year savings for 2025 will exceed $225M, and we have enabled approximately $450M in annual run rate savings, surpassing our prior expectations.”

- Autoliv ($8.5B, Automobile Components): “Our gross margin was 19.3%, an increase of 130 bps YoY. The improvement was mainly the result of direct labor efficiency, headcount reductions and compensation from the supplier.”

- Genuine Parts ($18.4B, Distributors): “We expect to continue to expand gross margin. We expect SG&A leverage in Q4, building on the improvement we’ve experienced sequentially through 2025, driven by our ongoing costs and restructuring actions. For 2025, we expect to incur restructuring expenses in the range of $180M to $210M, and an expected benefit of $110M to $135M. When fully annualized in 2026, we expect our 2024 and 2025 restructuring efforts and cost actions to deliver over $200M of cost savings.”

- Group 1 Automotive ($5.3B, Specialty Retail): “While we’ve executed target restructuring initiatives to improve efficiency and return the business to more sustainable cost levels, costs continue to increase; some of its government-imposed through increased payroll tax-related charges. In response to current market conditions, we are taking further actions to reduce our corporate headcount by approximately an additional 10%. And we are taking additional expense actions to save an expected $8M in our stores. We will benefit from these savings in 2026. We will also be executing additional restructuring plans in future periods, as we exit select OEM sites.“

- Mohawk Industries ($7.3B, Household Durables): “Our previously announced restructuring initiatives continue to benefit our results by streamlining our operations and reducing our cost structure. We have identified additional restructuring projects that should deliver approximately $32M in annualized savings. We are leveraging the scope of our product portfolio, distribution advantages and industry leading brands to expand our relationships with current and new customers.”

AI & Digital Acceleration

Companies Embracing AI and Digital Tools as Core Enablers of Efficiency, Personalization, and Growth; Organizations Moving from Experimentation to Large-Scale Implementation…and Providing Hard Stats

- Booking Holdings ($181.9B, Hotels, Restaurants & Leisure): “While there is certainly a lot of excitement in the industry [towards AI/GenAI], our approach has been disciplined and focused on where AI can make a real difference for our customers, our partners, and our business. On the customer side, we saw encouraging developments this past quarter. At Agoda, for example, we launched an AI-powered chatbot that provides travelers with prompt hotel-specific answers. By cutting through complexity and delivering precise information quickly, it helps travelers make timely and more confident booking decisions, reducing uncertainty, and improving the overall experience.”

- Wayfair ($8.5B, Specialty Retail): “While AI has certainly become the buzzword of late, we’ve been on the forefront of machine learning for a long time, leveraging algorithms to drive everything from pricing decisions to marketing investments. Just as AI is evolving our operations, it’s also up-leveling how we work. We’re committed to ensuring that every Wayfairian can benefit from this AI transformation. Our engineers are integrating leading coding assistants to accelerate development cycles, while business teams in marketing and merchandising use generative tools to automate repetitive tasks and focus on more strategic work. We have provided a generative AI license to every single employee, and we are fostering a culture of hands-on innovation that goes beyond just structured training. We’re encouraging our entire team to find new ways to create value with these tools through programs.”

- Amazon ($2455.0B, Broadline Retail): “The stores team is also innovating rapidly with AI. For example, Rufus, our AI-powered shopping assistant, has had 250 million active customers this year with monthly users up 140% YoY, interactions up 210% YoY and customers using Rufus during a shopping trip being 60% more likely to complete a purchase. Our generative AI-powered audio feature that combines product summaries and reviews to make shopping easier has expanded from hundreds of products at launch to millions of products and millions of customers have used it streaming almost 3 million minutes. In Amazon Lens, an AI-powered visual search tool that lets customers find products with their phone’s camera, a screenshot or a bar code, now includes Lens Live, which instantly scans products and shows real-time matches in a swipeable carousel.”

- Ford Motor ($43.3B, Automobiles): “We’re also modernizing our facilities and IT to unlock the next level of efficiency. We are systemically deploying AI across the entire industrial system. For example, we have significantly improved CAD loading times to less than 1 minute. And we have added 900 AI-powered cameras across our plants to detect quality issues at the source and help us mitigate supply disruptions.”

- Tractor Supply ($30.6B, Specialty Retail): “Over the last six months, we’ve done an enterprise integration with OpenAI, and we now have over 1,200 users that now have OpenAI enterprise accounts. What that allows us to do now is to start building agents to automate and make things simpler and faster.”

- Wyndham Hotels & Resorts ($6.7B, Hotels, Restaurants & Leisure): “This quarter, over 230 AI agents with encyclopedic knowledge on each of our 8,300 hotels began leveraging the power of Salesforce, Oracle, and Canary Technologies to generate and modify direct bookings while also answering questions and providing tailored travel recommendations by utilizing large language model AI and first-in-industry Agentic AI voice assistants.To date, Wyndham AI has already handled more than 500,000 customer interactions, delivering faster service, higher booking conversion, and a 25% reduction in average handle time, all contributing to nearly 300 bps of improvement in direct contribution for hotels leveraging Wyndham AI to its fullest potential.”

- Etsy ($6.1B, Broadline Retail): “In September, Etsy became the first live partner for their instant checkout feature, allowing users to buy items on Etsy directly through ChatGPT. We now provide a dedicated product feed that enables eligible purchases to be completed seamlessly within the chat experience, processed through Etsy Payments. Agentic visits represent a small slice of Ecommerce traffic today but they’re growing quickly. An early analysis suggests that these buyers come to Etsy with higher purchase intent than those from traditional search. And overtime, we believe these types of integrations will drive incremental growth and importantly, brand consideration for Etsy.”

Around the World

Global Trends Gradually Improving, Asia’s Growth Led by India, Japan, Korea, and China’s Selective Recovery; Softness and Pricing Pressures Remain in Europe

- Mattel ($5.5B, Leisure Products): “In EMEA, we saw four consecutive quarters of growth driven by strong consumer demand, and very disciplined execution across markets, and brands. In Asia Pacific, we’ve seen growth across key markets, including Australia, New Zealand, and China. In Latin America, there’s some industry softness in Mexico, but we continue to execute well, and as a whole, we look forward to continuing to grow our international business this year and over the long-term.”

- Mohawk Industries ($7.3B, Household Durables): “In the S., our commercial performance outpaced residential due to growth in the hospitality, healthcare and education sectors. In Europe, we improved sales volume in a difficult market. Pricing pressure persists with low market demand and our mix and productivity gains offset higher than anticipated input costs. Residential remodeling and new construction remain constrained, while the commercial channel shows continued strength, particularly in hospitality.”

- Pool ($11.7B, Distributors): “In Europe, net sales decreased 1% for the quarter in local currency and increased 6% in USD. Similar to last quarter, we saw growth in the southern countries, while impacts from political strain and related consumer uncertainty pressured sales in France.

- Levi Strauss ($7.8B, Textiles, Apparel & Luxury Goods): “ Our S. business was up 3%, delivering our fifth consecutive quarter of strong growth. Europe’s net revenues were up 3%, all key markets delivered growth led by very strong performance in the UK. While weather impacted footfall in June and July, we exited the quarter with strong performance in August and we continue to expect mid-single-digit growth in Europe for the year. Asia accelerated in the quarter, driven by double-digit growth in key markets like India, Japan, Korea and Turkey.”

- Group 1 Automotive ($5.3B, Specialty Retail): “The UK environment remains challenging with inflation, wage and insurance cost pressures and the Battery Electric Vehicle mandate, which continues to compress margins. “

- General Motors ($49.6B, Automobiles): “ In the U.S., we achieved our highest third quarter market share since 2017 with strong margins, and our restructured China business was profitable once again. GM China is continuing its successful turnaround and is comparing favorably to many of its global peers.”

- Booking Holdings ($181.9B, Hotels, Restaurants & Leisure): “We saw broad-based strength in room night growth across all major regions, and each region exceeded our expectations. Europe and the U.S. were up high-single-digits, and Asia and Rest of World each delivered low double-digit growth. We continued to see robust growth in certain travel corridors, including Canada to Mexico and Europe to Asia, which effectively offset softer demand in certain inbound corridors to the U.S.“

In Closing

The Consumer Discretionary sector commentary points to continued headwinds, including inflation and tariffs, but also tailwinds, namely a more conducive rate environment. Housing remains constrained by affordability, while several retailers indicate trends have bottomed rather than worsened. Against this macro, the consumer is cautious but resilient and increasingly bifurcated: higher-income shoppers selectively trade up to premium experiences, while value, essentials, and repairs hold up across income tiers. Tariffs persist as a swing factor, but mitigation playbooks — pricing, supply-chain diversification, and localized production — are increasingly proving effective, turning a headwind into a relative tailwind for domestic producers.

And then there are the spike in layoffs, as companies seek to protect margins…a clear signal that preparation is underway for a different operating environment: one with tighter margins, more automation, and a focus on productivity efficiency.

We will continue to highlight developing themes in our ongoing weekly earnings Sector Beat coverage to provide insightful information on the macroeconomic landscape and factors impacting market sentiment.

Up next week: Materials Sector Beat

- >$1B in market cap

- As of 12pm ET 10/30/25