This Week in Earnings – Q2’23

The Sector Beat: Industirals

In today’s thought leadership, we cover:

- Key Events this week

- Earnings Snap, covering the S&P 500 stats to date

- Spotlight on Industrials in The Sector Beat

Key Events

GDP Growth

Consumer Confidence

Interest Rates

Manufacturing and Services

U.S.

S&P Global’s flash U.S. Composite Purchasing Managers’ Index (PMI) indicated U.S. business activity slowed to a five-month low in July, dragged down by decelerating service-sector growth; the index fell to a reading of 52.0 in July from 53.2 in June, with service-sector activity falling to 52.4 in July from 54.4 one month prior (Source: S&P Global)

EU

S&P Global’s flash Composite PMI indicated Eurozone business output fell at the fastest rate in eight months in July, with deteriorating forward-looking indicators such as future output expectations and new order inflows pointing to the likelihood of the downturn deepening in coming months; services slowed to the weakest level since January, though still remained in expansion territory (Source: S&P Global)

China

China’s former foreign minister, Qin Gang, who was replaced on Tuesday after he went missing from public view for more than a month, is now disappearing from parts of the Foreign Ministry’s website; authorities didn’t provide a reason for their decision to remove Qin Gang from his post, which has now been filled by his predecessor, Wang Yi, but the Foreign Ministry previously cited unspecified health reasons for Qin’s absence (Source: WSJ)

S&P 500 Earnings Snap

51% of the S&P 500 has reported earnings to date

Q2'23 Revenue Performance

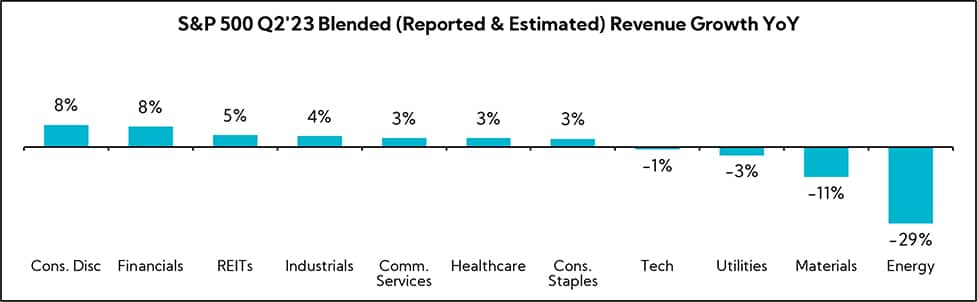

- 62% have reported a positive revenue surprise, below the 1-year average (71%) but above the 5-year average (69%)

- Blended revenue growth (combines actual reported results for companies and estimated results for companies yet to report) is -0.4%

- Companies are reporting revenue 1.5% above consensus estimates, and slightly below the 1-year average (+2.5%) and above the 5-year average (+2.0%)

Q2’23 EPS Performance

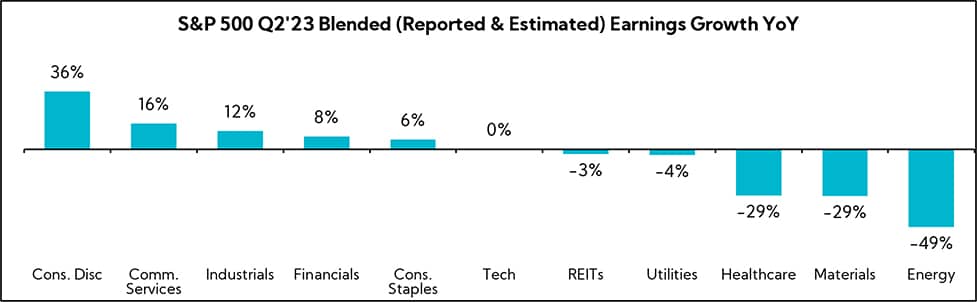

- 79% have reported a positive EPS surprise, above the 1-year average (73%) and slightly above the 5-year average (77%)

- Blended earnings growth (combines actual reported results for companies and estimated results for companies yet to report) is –6.4%

- Companies are reporting earnings 6.6% above consensus estimates, well above the 1-year average (+3.2%) but below the 5-year average (+8.4%)

The Sector Beat: Industrials

Guidance Trends

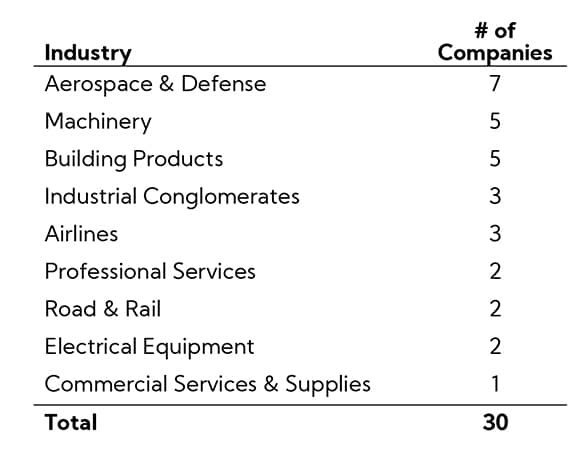

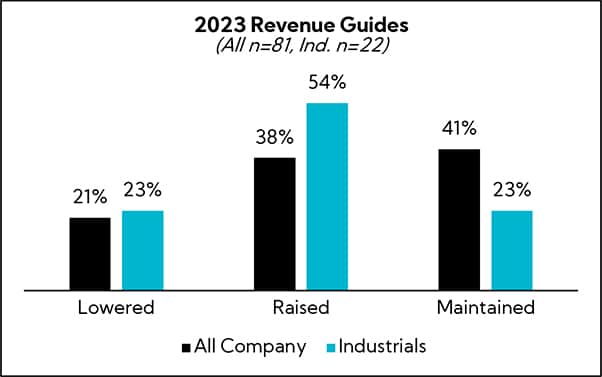

As we do every quarter, we analyzed annual revenue and EPS guidance provided by 30 industrial companies with market caps greater than $500M that have reported to date.1 Below are our findings.2

For comparison purposes, we are providing an “All-Company” benchmark, which represents all companies above $500M market cap and across all sectors that have reported since July 17, which we track in real time.3

Guidance Breakdown by Industry

On average, Industrials are seeing a greater number of companies raising guidance across both revenue and EPS, with slightly fewer maintaining than the All-Company benchmark. Consistent with the broader universe, few are lowering guidance at this time — a clear reflection of executives’ conservative 2023 projections introduced earlier in the year.

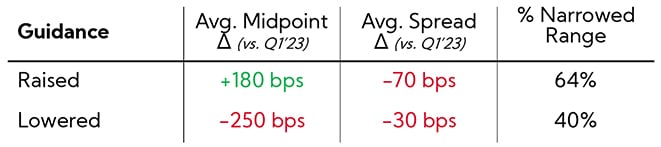

Revenue Guidance

Annual Revenue Guidance Summary

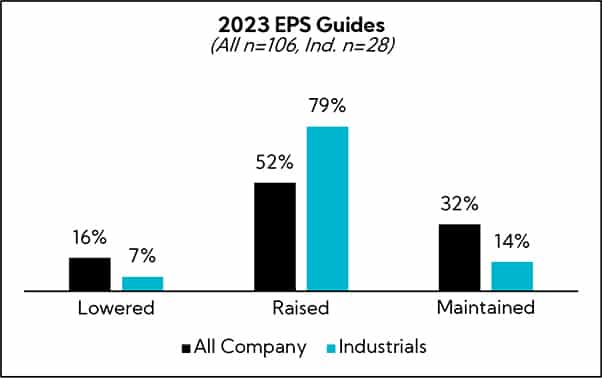

EPS Guidance

- Companies that raised guidance (n = 22):

- 77% raised the bottom and top of the original range

- 23% raised the bottom and maintained the top of the original range

- Average spreads decreased from $0.46 to $0.33, respectively

- Companies that maintained guidance (n = 4):

- Average spread of $0.61

- Only two industrials lowered guidance, with both companies largely exposed to the transportation industry

Annual Adjusted4 EPS Guidance

Earnings Call Analysis

Further, we analyzed the earnings calls for this group and the broader industrial universe to identify key themes.

As we noted last week, our Q2’23 Inside The Buy-Side® Industrial Sentiment Survey® found continued diverging perspectives among surveyed industrial investors and analysts and executive tone that was characterized as more positive. Notably, 59% described executive tone as Neutral to Bullish or Bullish, up from 52% last quarter and the highest level since Q4’21. Meanwhile, 45% of investors self-describe sentiment as Neutral to Bearish or Bearish, up from 37% QoQ, while those in the Neutral to Bullish or Bullish camp also saw a slight rise to 38% from 35%, underscoring continued bifurcation. Across three quarters, outright bearishness has eased.

Examining industrial earnings commentary indeed reveals mixed messaging, but markedly improved versus last quarter. Despite ongoing uncertainties in the global economy, executives across various sub-sectors express cautious optimism for the second half of 2023. Many point to a resilient consumer, moderating inflation, improved supply chains, and secular stimulus tailwinds as evidence of a normalizing — even improving — environment. Yet, the potential impacts of heightened interest rates and geopolitical tensions have added a shroud of unpredictability heading into Q3 and beyond.

Underlying demand appears to be “stable”, and significant strides in operational efficiency have enabled companies to streamline their lead times and work down their book-to-bill ratios. To that end, some industrials are noticing customers throttling their ordering patterns in lieu of improved lead times.

Many have managed to bolster their margins through a combination of cost cutting and input pressure stabilization. While some have succeeded in implementing price increases without compromising orders, the likelihood of waning pricing power, fueled by potential disinflation and even deflation, suggests that future price increases will need to be more modest and strategic.

With nearly 80% of industrials raising annual EPS expectations, our guidance analysis suggests many were indeed playing to the “under promise and over deliver” when initially guiding earlier this year. Still, industrial investor angst continues to outpace that of management teams, a sign that many may not be buying the rosier picture just yet.

Key Earnings Call Themes

Despite Continued Near-term Economic Uncertainty, Executives Reinforce Cautious Optimism About the Back Half of 2023 as Conditions “Stabilize”; A Resilient Consumer Continues to Boost Sentiment

- Owens Corning (FY Q2’23 – $12.9B, Building Products & Equipment): “We expect inflation to continue to moderate, but the impact of higher interest rates and ongoing geopolitical tensions to result in continued market uncertainty and slower global economic growth. That said, we anticipate many of our end markets to be relatively stable with housing sentiment in the US turning more positive; and many of the key verticals within our non-residential businesses continuing to hold up. Based on this near-term market outlook, for the third quarter, we expect our volumes to be relatively stable sequentially with positive overall pricing YoY.”

- Armstrong World Industries (FY Q2’23 – $3.6B, Building Products & Equipment): “The backdrop of overall uncertainty tied to the macroeconomic still exists. So, cautious as we approach the back half of the year, and we are monitoring the market. But as we noted in our guidance…we removed our worst-case market scenario and took that off the table. That being said, there is still a lot of uncertainty as we head into the back half year.”

- Franklin Electric (FY Q2’23 – $4.5B, Specialty Industrial Machinery): “On the macro level, we’re not economists, we’re not predicting where the economy is going. We don’t see a recession built into our outlook. We see the economy continuing to move along at the current level through the end of the year and into 2024.”

- Automatic Data Processing (FY Q4’23 – $106.0B, Staffing & Employment Services): “While the economic backdrop remains uncertain…Our fiscal 2024 outlook assumes some moderation in economic activity over the course of the year, but nothing dramatic.”

- Knight-Swift Transportation (FY Q2’23 – $9.6B, Trucking): “I don’t know that we’ve ever seen freight demand fall this far so fast and for so long without an accompanying economic recession. I’m not suggesting that truckload demand softness is an automatic predictive indicator of broader economic weakness. In fact, we’re very encouraged with how consumers in the economy have digested interest rate increases and their positive impact on inflation.”

- Dover (FY Q2’23 – $20.7B, Specialty Industrial Machinery): “In terms of the total macro, we’re happy that that demand has held up. You see part of the negative headwind to some is the destocking because everybody is destocking because they’re afraid of the macro to a certain extent. That’s been exasperated a little bit by the cost of capital working its way through the system. Where we go from here? We’re positioning for a soft landing.”

An Improved Operational Environment Results in Streamlined Lead Times for Many; Book-to-Bill Ratios are Normalizing (ex-Aerospace and Defense, Where Companies Continue to See Supply Constraints)

Lead Times

- Franklin Electric (FY Q2’23 – $4.5B, Specialty Industrial Machinery): “As our lead times are improving, we are reducing transfers to our Headwater Distribution segment to rightsize their inventory of our products. We expect that other customers are rightsizing inventories as well. We believe these weather and destocking headwinds to be transitory while we continue to see healthy end-market demand across our business.”

- Allegion (FY Q2’23 – $10.5B, Security & Protection Services): “We did see some softness in non-residential mechanical demand as customers and distribution partners adjust their ordering patterns to our reduced lead times due to much improved supply chain and operational execution.”

- Armstrong World Industries (FY Q2’23 – $3.6B, Building Products & Equipment): “The biggest change for us versus where we were at the beginning of the year on the back half is the on-the-ground sentiment and conversations with our customers and the activity they see…they have better visibility to their backlogs. Not great, but better than what we had at the beginning of the year.”

- Hubbell (FY Q2’23 – $16.5B, Electrical Equipment & Parts): “Our lead times were out towards the 50-week range and they’re now down to two to three weeks range. That’s had an impact on how our customers have been ordering for us for the past couple of quarters and that’s been affecting the unit volumes that we’re shipping.”

Book-to-Bill Ratios

- Hubbell (FY Q2’23 – $16.5B, Electrical Equipment & Parts): “In the more commercial arena, we’re hearing anecdotes suggesting that their days of inventory are getting in line with their targets. And therefore, we may be nearer to the end of that adjustment period and our expectation in second half will be a little more balanced between book and bill.”

- Dover (FY Q2’23 – $20.7B, Specialty Industrial Machinery): “Organic bookings were down 8%, resulting in a book-to-bill of 0.92x, reflecting better lead times across the portfolio and continued strong shipments against backlogs in our longer-cycle and secular-growth-exposed businesses. As a result, our backlog continues to normalize but remains elevated relative to pre-pandemic levels.”

- Zurn Elkay Water Solutions (FY Q2’23 – $5.3B, Pollution & Treatment Controls): “Our order book-to-bill over the next six months is always going to be somewhere around 1.0x. We saw as lead times extended through a couple years post pandemic, that forced different order behavior. When you get to where we are today, the backlog sits at the traditional relatively low levels. The second half would imply a book-to-bill right around 1.0x, maybe just a touch better.”

Aerospace & Defense

- General Dynamics (FY Q2’23 – $60.1B, Aerospace & Defense): “We had a very good quarter from an orders perspective with an overall book-to-bill ratio of 1.2x for the company. Order activity was strong across the board, as each segment had a book-to-bill of 1:1 or greater in the quarter. “

- Textron (FY Q2’23 – $15.4B, Aerospace & Defense): “We’ve posted a strong book-to-bill again in the quarter. It’s both jets and turboprops. We continue to be really happy with how the market is behaving in terms of demand and pricing. As I think you’re hearing from everybody, the biggest challenge still remains on the supply chain side of things. It’s not getting worse; it’s probably getting better. But as you know, the challenge is every part is important.”

- Boeing (FY Q2’23 – $142.3B, Aerospace & Defense): “With demand strong, we still find ourselves in a supply-constrained environment and our focus continues to be on execution, both within our factories and the supply chain as we steadily increase production.”

Expense Management and Moderating Input Costs Support Margin Preservation; Continued Pricing Power Is Being Called Into Question

Cost Improvements

- Dover (FY Q2’23 – $20.7B, Specialty Industrial Machinery): “Underlying demand remains good across the portfolio and a significant volume of business is already in the backlog. We proactively intervened on our cost structure starting in the latter half of 2022 and we have continued these structural cost reductions in 2023, driving material earnings benefits. As a result, we are less reliant on top-line volume or price/cost to achieve our forecast in the second half.”

- Armstrong World Industries (FY Q2’23 – $3.6B, Building Products & Equipment): “SG&A in the quarter was essentially unchanged versus the prior year, as modest increases in selling expense in support of our digital initiatives were partially offset by the benefits from our previously announced cost savings initiative.”

- Carlisle (FY Q2’23 – $14.0B, Building Products & Equipment): “Despite the double-digit revenue decline, we expect consolidated margins to decline only 50 bps YoY in 2023. We remain focused on operational efficiencies, managing costs through our continuous improvement efforts and disciplined pricing, which is leading to better price cost capture this year.”

Input Cost Moderation

- Owens Corning: (FY Q2’23 – $12.9B, Building Products & Equipment): “From a cost perspective, we expect input materials, energy and delivery to continue to moderate, resulting in fairly neutral inflation for the quarter and positive, but narrowing price/cost.”

- Waste Management (FY Q2’23 – $66.1B, Waste Management): “While we experienced some impact of lingering inflation into Q2, signs of easing continued as the quarter progressed. The areas experiencing the most pressure are labor costs & repair and maintenance costs. There’s cause for optimism in both of these categories. Labor costs have continued to moderate during the second quarter, settling in the mid-single-digit range from the double-digit levels that we have seen over the last year. This improvement can be attributed to better employee retention.”

- Armstrong World Industries (FY Q2’23– $3.6B, Building Products & Equipment): “We were flat on total input costs in the second quarter. What we’re seeing is continued inflation on the raw material side with some offsetting benefits from energy and freight. In the back half, we’ll continue to see that inflationary pressure on the raw side and some continued moderation in deflation on the energy and freight side.”

- Hexcel (FY Q2’23 – $6.0B, Aerospace & Defense): “A lot of the inflationary pressures are transitory, energy costs are going to dissipate certainly as we look forward into 2024. Some of the commodity, chemicals, and raw materials that we buy are going to ease off.”

- Hubbell (FY Q2’23 – $16.5B, Electrical Equipment & Parts): “Price cost is really the biggest driver there and, interestingly, both levers contributing to the margin expansion. You’ve seen our price story play out over the last couple of years or so. But also this quarter, we had material cost flipping to a tailwind, so actual deflation in both the raws and our component costs there helping drive strong margins.”

Waning Pricing Power

- Zurn Elkay Water Solutions (FY Q2’23 – $5.3B, Pollution & Treatment Controls): “The pricing environment has continued to stick. There’s not been price give back in this environment. I’d call it stable going into next year and beyond. It looks like it’s getting back from what that normal ranges were. It feels like it’s back to normal trends on a go-forward basis.”

- Automatic Data Processing (FY Q4’23 – $106.0B, Staffing & Employment Services): “We want to make sure that we’re not getting greedy so we did get about 150 bps price in the year and we did that without the expense of seeing a decline in retention or NPS scores…For 2024, we do expect to have price increases again but we do not think that we’re going to be in the 150 bps range. We’re certainly going to be above our historical average of about 50 bps but once again we’ll watch closely and make sure that the underlying value proposition for our client stays in place and we will take some price for sure but not to the extent that we did in FY 2023.”

- 3M (FY Q2’23 – $61.8B, Conglomerates): “With disinflation, you’re going to start to have discussions around impact on price…the area where you have the most discussion typically are retail markets. That’s an ongoing discussion. Always is even in the times of high inflation it’s a strong discussion, but price is a topic everywhere. We’re confident that we’re priced in the right place as we come through this market dynamic broadly. So, we’re not looking at pressure specific in one segment or another, but I would say the conversation is something that we anticipate as we see disinflation and eventually, we see a deflation then we would expect it to ramp up.”

M&A — Deal Drought Continues as Buyers Cite Strict Lending Conditions and High Valuations, Though Funnel is Improving from Less Competition for Assets

- Waste Management (FY Q2’23 – $66.1B, Waste Management): “The valuations have crept up. A lot of these smaller businesses are seeing an uptick in their businesses coming out of COVID. There’s an expectation from some of these businesses that now is the time to sell, whether it’s because they don’t have succession plans behind them or because of some of the labor pressures that they’re anticipating. For us, it’s a double-edged sword. We want to make sure we do have a nice pipeline of M&A opportunities but we don’t want to fall into the trap of paying way up for these, so we’ll be patient when it comes to those.”

- Armstrong World Industries (FY Q2’23 – $3.6B, Building Products & Equipment): “We never left the acquisitions or the business development game…it’s our number two priority after using our free cash to invest back into this high ROIC business of ours…And then third, with the authorization we have even more headroom here to continue to buy back our shares and support a growth dividend.”

- Allegion (FY Q2’23 – $10.5B, Security & Protection Services): “Short of talking about any specific targets, I feel very good about the top of our funnel in terms of looking for acquisition targets…You can look and expect us to also be a disciplined buyer. But we do see acquisitions playing a key role in our overall growth strategy.”

- Dover (FY Q2’23 – $20.7B, Specialty Industrial Machinery): “Competition is less. There’s not a lot of assets out there, but competition is less. Private equity’s a bit stopped out right now for reasons we can understand. We’re looking at some attractive things here, but we’re going to keep our discipline in terms of the return.“

- Hubbell (FY Q2’23 – $16.5B, Electrical Equipment & Parts): “There are more assets coming to market than we typically see and there’s more assets above this $60M tuck-in that is quite typical for us. I feel that is in response to owners figuring this is a good time to get a good valuation. And we see the competition in those processes. It’s Interesting. The acquisition finance market is a bit different. You have higher interest rates and that’s affecting how some financial buyers approach the market…[The] higher multiple, can be justified given the growth and margin potential of some of the businesses that are being put in. I’m hoping not too many investment bankers are listening right now, but I do think there is probably some upward drift in multiple.”

Government Stimulus “Displaying Quantifiable Progress” as Incentive Programs Work Their Way Through the System and Boost Re/Onshoring Efforts

- Wabash (FY Q2’23 – $1.1B, Farm & Heavy Construction Machinery):“Reshoring is displaying quantifiable progress as of late, as evidenced by the significant increase of 77% in construction spending on manufacturing facilities in the United States, in May compared to the same month of the previous year. This trend is exciting as it indicates the ongoing reorganization of supply chains post-COVID.”

- Hubbell (FY Q2’23 – $16.5B, Electrical Equipment & Parts): “In telco and distribution, we’re seeing orders and quotes up over 50% over prior year. There’s some support here from stimulus packages, from government policy, where IRA is helping spur development through the provision of the tax credits versus the IIJA, providing harder funding dollars to spend on the projects.”

- Armstrong World Industries (FY Q2’23 – $3.6B, Building Products & Equipment): “We continue to see increasing bidding activity for airport projects. This increase in demand has been fueled by the recent infrastructure bill, which includes $5B in spending specifically for airports…These opportunities are growing and often involve a wide range of materials from Mineral Fiber, wood, metal and more of Armstrong’s complete portfolio. Given the scale and complexity of these projects and now Armstrong’s size and capabilities, we expect the tailwind from transportation to last beyond 2026.”

- Allegion (FY Q2’23 – $10.5B, Security & Protection Services): “The institutional segment continues to flash signals of resilience. Healthcare, education, and even airports are still in the benefiting phase from the infrastructure bill because airport terminal renewal was one of the founding principles there of that bill.”

- General Electric (FY Q2’23 – $126.5B, Specialty Industrial Machinery):“Onshore Wind was strong again led by North American equipment, growing more than three-fold. We serve many of North America’s largest developers and the IRA incentives are helping grow orders significantly this year.”

- Encore Wire (FY Q2’23 – $2.9B, Electrical Equipment & Parts): “We expect that the current legislation in place to help funding infrastructure needed for broad electrification will bolster long-term demand for many of our product categories. We also expect that this demand will raise the floor for the price of many raw material inputs for years to come.”

China — A Reversal from Last Quarter, Companies Are Downplaying Their China Exposure as Limited Demand Pressures Pricing, with Some Moving Manufacturing Elsewhere

- Boeing (FY Q2’23 – $142.3B, Aerospace & Defense): “We certainly want to support our customers in China, and we will be the free-trade beacon with respect to our administration and all the political influences. But I’m just going to leave it postured just the way it has been. Know that we have 85 airplanes that we would like to begin delivery on. We’re getting good signals, but our guidance is not dependent on it.”

- 3M (FY Q2’23 – $61.8B, Conglomerates): “Regionally, China’s recovery has been slow, impacted by electronics and soft export trends.”

- Owens Corning (FY Q2’23 – $12.9B, Building Products & Equipment): “Now in Asia, it continues to be a spot pricing market, and we will likely continue to see some tougher discussions around pricing in those markets as the Chinese market continues to operate at the levels it’s been at for the last 18 to 24 months and local production is being not used fully in the Chinese domestic market. In general, it’s being exported to other places as I’ve called out India in prior quarters.”

- Allegion (FY Q2’23 – $10.5B, Security & Protection Services): “APAC for us, we do have some China exposure. It’s not a lot, but there’s no doubt, China is under a lot of pressure. And so, our relatively small but profitable business there is certainly lower relatively speaking.”

- Dover (FY Q2’23 – $20.4B, Specialty Industrial Machinery): “We have two businesses that have a kind of a material exposure to China, and that’s one of them. That [performance] is just a reflection mostly of demand to China being quite poor.”

In Closing

Industrials generally continue to outpace conservative expectations that were set heading into 2023. Companies in this segment are starting to take the worst-case scenarios off the table and out of their guidance ranges as the economic environment is holding up well enough to garner some cautious optimism. Meanwhile, inflation is becoming less of a headwind for margins. It remains to be seen how much the impact of higher interest rates will continue to filter through the economy in the coming quarters.

For now, it appears this will be more of a discussion point when companies start projecting out for calendar year 2024.

- As of 12:00pm on July 27, 2023

- A small number of the 30 companies tracked do not report one of either revenue or EPS guidance, hence the difference in “n” in chart headers

- The total number of companies in the All-Company benchmarks are different across revenue and EPS charts and based on the data available and reported by companies at the time of our publication

- Non-GAAP figures reported by the individual companies analyzed