This Week in Earnings – Q4'25

Materials Sector Beat

Our thought leadership this week addresses:

- Key Events this week

- Earnings Snap, covering the S&P 500 stats to date

- Spotlight on Materials in The Sector Beat

Key Events

Supreme Court Strikes Down President Trump’s Global Tariffs

- Early Friday morning, the U.S. Supreme Court ruled 6-3 that President Trump’s broad tariffs were unlawful. This marks the first time during Trump’s second term that the highest court has definitively ruled against the administration. The case involved two set categories of tariffs: one applied to nearly every country in the world to address trade deficits, and another set imposed against Mexico, Canada, and China, which the administration claimed were responsible for the illegal flow of fentanyl into the U.S. Writing for the majority, Chief Justice Roberts, rejected the use of the International Emergency Economic Powers Act (IEEPA) as justification for either category. He stated, “Had Congress intended to convey the distinct and extraordinary power to impose tariffs, it would have done so expressly.” Equity markets traded moderately higher following the decision, led by trade- and tariff-exposed stocks. (Source: WSJ, United States Supreme Court)

Rising U.S.-Iran Tensions

- U.S.–Iran tensions have intensified amid reports that the U.S. military is positioned for a potential strike, though President Trump has not made a final decision and indicated developments could come within 10 days. While diplomacy remains publicly prioritized, officials acknowledge significant gaps in negotiations over Iran’s nuclear program, and the U.S. has expanded its military presence in the region as Israel signals readiness for escalation. Markets have largely looked through the developments, though oil prices have reacted sharply amid renewed concerns over potential disruptions, including threats involving the Strait of Hormuz. (Source: Bloomberg, NBC, Axios)

January FOMC Minutes

- The Fed released the minutes from its January 27–28 FOMC meeting on Wednesday, showing few surprises following its decision to hold rates steady. Policymakers noted inflation progress may be slower and uneven, partly reflecting tariff-related pressures, while still expecting those effects to fade over time. Officials described a stabilizing labor market and solid growth supported by resilient consumer spending and AI-related investment, reinforcing a cautious, data-dependent stance; markets continue to price the first rate cut around June. (Source: Federal Reserve, CNBC)

U.S. Economic Data

- New orders for U.S. manufactured durable goods declined 1.4% in December to $319.6 billion, marking the second decrease in three months and following a 5.4% gain in November. Orders excluding transportation rose 0.9%, while orders excluding defense fell 2.5%. The overall decline was driven by a 5.3% drop in transportation equipment orders, which have also decreased in two of the past three months. (Source: Census Bureau)

- The U.S. goods and services trade deficit widened to $70.3B in December from a revised $53.0B in November, as exports fell $5.0B MoM to $287.3B while imports rose $12.3B to $357.6B. The increase reflected a larger goods deficit and a narrower services surplus. For 2025, the overall deficit declined 0.2% YoY, with exports rising 6.2% and imports increasing 4.8% compared to 2024. (Source: Bureau of Economic Analysis)

- U.S. initial jobless claims declined by 23K to a seasonally adjusted 206K for the week ended February 14, below the consensus estimate of 225K. Continuing claims increased to 1869K for the week ended February 7. (Source: Labor Department)

Policy-by-Post

- February 17: President Trump announced the launch of a U.S.–Japan trade agreement and highlighted new investment projects in energy and critical minerals – “Our MASSIVE Trade Deal with Japan has just launched! Japan is now officially, and financially, moving forward with the FIRST set of Investments under its $550 BILLION Dollar Commitment to invest in the United States of America — part of our Historic Trade Deal to REVITALIZE the American Industrial Base, create HUNDREDS OF THOUSANDS of GREAT American Jobs, and strengthen our National and Economic Security like never before. Today, I am pleased to announce three TREMENDOUS Projects in the Strategic Areas of Oil & Gas in the Great State of Texas, Power Generation in the Great State of Ohio, and Critical Minerals in the Great State of Georgia. The scale of these projects are so large, and could not be done without one very special word, TARIFFS. The Gas Power Plant in Ohio (A State I won THREE TIMES!) will be the largest in History, the LNG Facility in the Gulf of America will drive Exports, and further our Country’s Energy DOMINANCE, and our Critical Minerals Facility will end our FOOLISH dependance on Foreign Sources…” (Source: Truth Social)

- February 17: President Trump promoted recent tax policy changes and their impact on 2026 tax refunds – “Tax Refunds this year, because of “THE GREAT BIG BEAUTIFUL BILL,” are substantially greater than ever before. In some cases, estimates are that over 20% will be returned to the Taxpayer. So, when you get your Tax Refund, think about what a wonderful President you have — NO TAX ON TIPS, NO TAX ON SOCIAL SECURITY FOR OUR GREAT SENIORS, NO TAX ON OVERTIME, INTEREST DEDUCTIONS ON CAR LOANS, AND MUCH MORE. Don’t spend all of this money in one place!” (Source: Truth Social)

- February 18: President Trump states that tariffs have significantly reduced the U.S. trade deficit – “THE UNITED STATES TRADE DEFICIT HAS BEEN REDUCED BY 78% BECAUSE OF THE TARIFFS BEING CHARGED TO OTHER COMPANIES AND COUNTRIES. IT WILL GO INTO POSITIVE TERRITORY DURING THIS YEAR, FOR THE FIRST TIME IN MANY DECADES. THANK YOU FOR YOUR ATTENTION TO THIS MATTER!” (Source: Truth Social)

Earnings Snap

85% of the S&P 500 has reported earnings to date

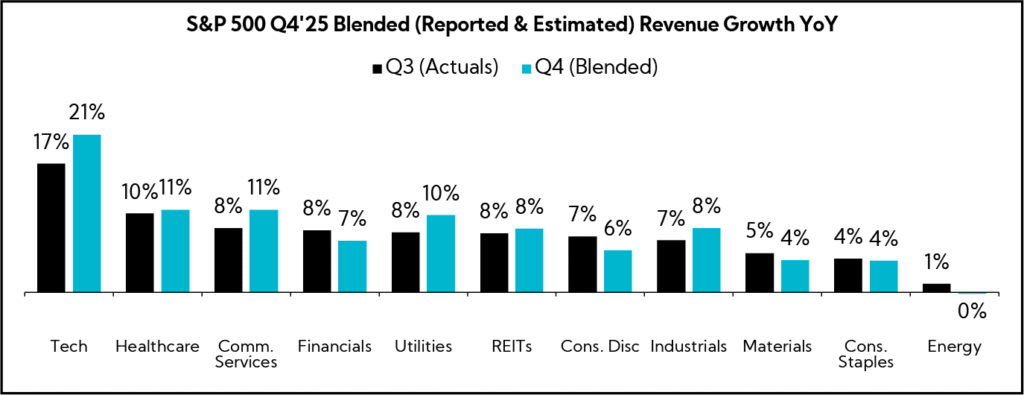

Q4'25 Revenue Performance

- 72% have reported a positive revenue surprise, slightly above the 1- and 5-year averages of 71% and 70%, respectively

- Blended revenue growth (combines actual reported results for companies and estimated results for companies yet to report) is 8.8%

- Companies are reporting revenue 1.8% above consensus estimates, higher than 1-year average of 1.3% and lower than the 5-year average of 2.0%

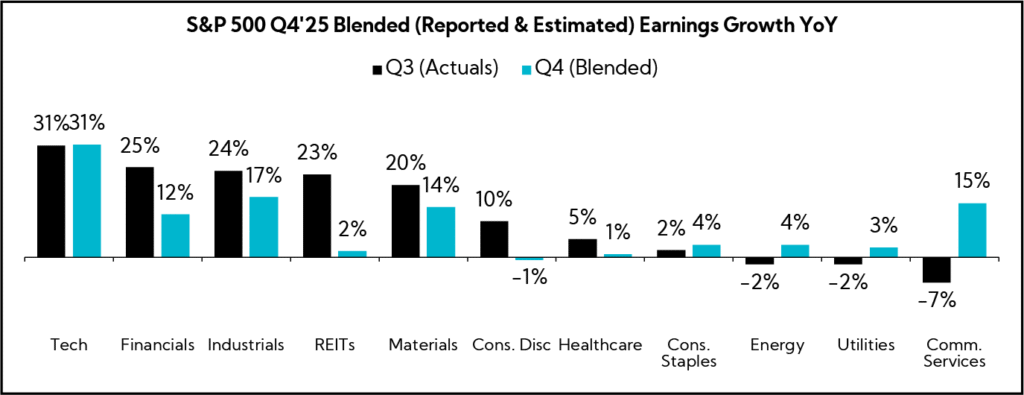

Q4’25 EPS Performance

- 73% have reported a positive EPS surprise, below the 1- and 5-year averages of 78% and 79%, respectively

- Blended earnings growth (combines actual reported results for companies and estimated results for companies yet to report) is 13.9%

- Companies are reporting earnings 5.1% above consensus estimates, below the 1- and 5-year averages of 7.4% and 7.7%, respectively

The Sector Beat: Materials

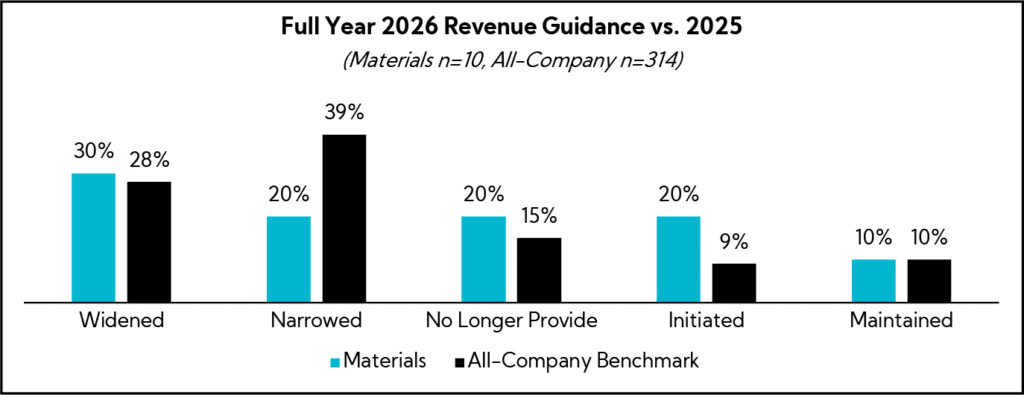

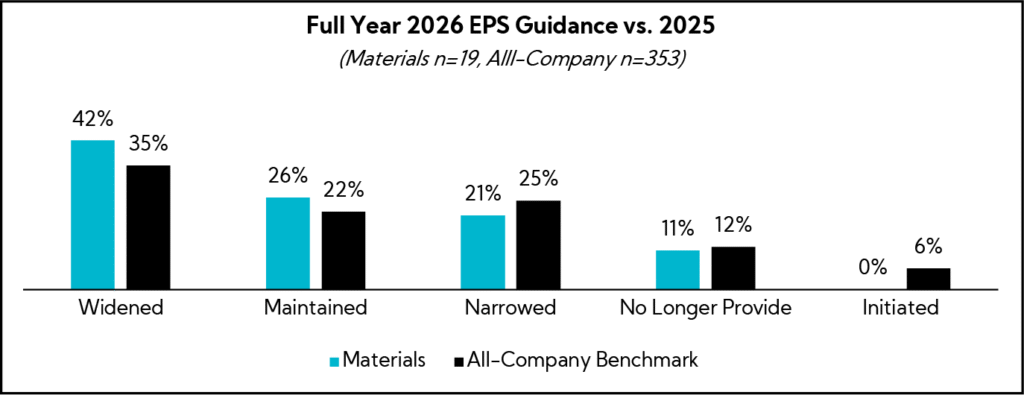

Materials Guidance Trends

We analyzed annual revenue and EPS guidance provided by calendar year U.S. Materials companies with market caps ≥$1B that have reported to date.

For comparison purposes, we provide an “All-Company” benchmark, which tracks in real-time a basket of calendar year companies ≥$1B in market cap across all sectors that have reported earnings to date (n = 471).1

1. As of 2/19/2026

Guidance Breakdown by Industry

| Industry | Number of Companies |

|---|---|

| Chemicals | 13 |

| Packaging & Containers | 5 |

| Construction Materials | 4 |

| Metals & Mining | 3 |

| Total | 15 |

Source: Corbin Advisors

Annual Revenue and EPS Guidance

Revenue

- 30% Widened spreads relative to last year, in line with the all-company benchmark (28%); 63% of midpoints are above 2025 actuals

EPS

- 42% Widened spreads relative to last year, while 26% Maintained and 21% Narrowed; 94% of midpoints are above 2025 actuals

Earnings Call Analysis

We analyzed earnings call prepared remarks and Q&A for this group and the broader Materials sector universe to identify key themes.

Materials companies broadly expect a gradual but uneven recovery in 2026, supported by easing interest rates, infrastructure investment, and AI-driven demand, though visibility remains limited. Several management teams see early signs of stabilization in volumes and pricing, particularly in Europe and parts of China, but the recovery is not yet broad-based. Residential construction and other interest rate-sensitive markets remain soft, consumer sentiment is cautious, and trade and geopolitical uncertainty continue to weigh on the outlook. As a result, companies are positioning for improvement but are not assuming a sharp rebound and guiding with wider EPS ranges than the all-company benchmark.

Inventory dynamics remain a key swing factor. Across the value chain, companies and their customers are tightly managing working capital and maintaining lean inventory positions amid lingering uncertainty. Destocking appears to be nearing an end in some segments, with expectations for a more balanced environment by mid-year. However, channel inventories remain cautious, and several executives noted that historically lean positioning can create temporary shortages if demand inflects faster than anticipated in 2026. The system is disciplined but potentially under-buffered.

Demand trends continue to diverge meaningfully by end market. Infrastructure, energy, advanced manufacturing, and AI and data center buildouts are providing the most consistent sources of growth, helping to offset ongoing weakness in residential construction, automotive, and other cyclical sectors. Data center investment in particular is emerging as a structural driver across metals, chemicals, construction materials, and electronics-exposed businesses, with hyperscale and electrification trends supporting incremental demand. These pockets of strength are supportive, but they have not yet translated into a broad-based acceleration across verticals.

In response to the uneven demand backdrop, companies are continuing to execute structural cost reduction and operational excellence programs. Headcount reductions, facility closures, procurement savings, process simplification, and increased automation are being deployed to reset cost bases and expand margins into 2026 and beyond. Many of these initiatives are multi-year in nature and are designed not only to protect profitability in a subdued environment but also to enhance operating leverage when volumes recover.

Regionally, North America and Latin America remain relatively resilient, supported by infrastructure spending, domestic manufacturing initiatives, and solid performance in select industrial and electronics markets. Europe appears to be stabilizing after a prolonged downturn but remains weak in automotive, particularly in premium segments. China shows signs of bottoming, though demand remains mixed amid policy shifts and trade uncertainties.

Key Themes

Macro and Outlook

Companies Broadly Expect a Gradual but Uneven Recovery into 2026, Supported by Easing Rates and Infrastructure and AI-driven Demand, but Tempered by Soft Residential Markets, Cautious Consumers, and China Uncertainty

- Huntsman ($1.9B, Chemicals): “As we look out over 2026, we anticipate a gradual recovery in North American homebuilding and durable goods as well as an improvement in the Chinese domestic market. We are seeing some very early signs of both improved volumes and pricing in Europe. It is too early to say these increases will fully materialize, but we remain hopeful. On the strategic front, I believe that 2026 will continue to be another year of changing market dynamics. Even if we start to see a recovery, we will likely see further opportunities for mergers, joint ventures and industry consolidation.”

- Amrize ($30B, Construction Materials): “In 2026, we expect the commercial market to pick up as interest rates continue to move lower and as customers accelerate their investments in advanced manufacturing, warehousing and logistics. In infrastructure, demand continues to be steady with federal, state and local authorities prioritizing modernization projects. We see an increasingly domestic focused agendas of our customers in both the U.S. and Canada. Each country is prioritizing national investments to build strong futures. Within residential, new construction remains soft. We expect demand to gradually return later this year. As the U.S. continues to have a significant housing shortage that will drive longer-term growth. As interest rates continue to decline, we expect pent-up demand to unwind and construction activity to accelerate across all sectors.”

- Freeport-McMoRan ($93.5B, Metals & Mining): “During 2025 copper prices largely tracked macro sentiment, market weighed U.S. dollar weakness, expected U.S. rate cuts, accelerating AI and technology-driven demand, and Chinese stimulus against mixed economic data, uncertainty around tariff and trade policy, economic pressures in China, and elevated geopolitical risk.”

- Sherwin-Williams ($87.9B, Chemicals): “The demand environment feels much like it did a year ago. The softer for longer dynamic we described again back in October remains intact. While some conditions are gradually becoming more stable, many of the indicators we track, along with cautious consumer sentiment, provide little support for any broad-based or accelerated recovery at this time. This environment is likely to persist well into 2026.”

- Dow ($19.5B, Chemicals): “Across the broader macroeconomic landscape, there are mixed signals in several of our end market verticals and key geographies. Recent developments are showing some encouraging signals in response to structural industry challenges, as well as trade and tariff uncertainties. This includes several announcements of further ethylene capacity rationalizations, as well as the elimination of VAT export rebates on select products in China.”

- Avient ($3.3B, Chemicals): “Coming specifically to 2026, our premise is that macro environment will remain volatile, impacted by trade policies, geopolitics and moving supply chains. However, we are cautiously optimistic about 2026 being a better year than 2025 from a market demand”

Inventory

Tight Inventory and Working Capital Control Persist Amid Ongoing Destocking and Cautious Channel Behavior, Though Lean Positions Increase the Risk of Temporary Shortages if Demand Rebounds More Quickly in 2026

- Huntsman ($1.9B, Chemicals): “All companies right now in that supply chain are trying to control cash and trying to control inventories and working capital. Building suppliers, OSB producers, auto industries that are having to write off billions of dollars on EVs and so forth, they’re all focused on cash right now and inventory control. Having lived through a bunch of other sudden rebounds in the industry, this industry typically does not recover over the course of four or five quarters. It usually gets to a point where people realize products are tight, and all of a sudden we can’t restock in time for a demand upswing, and all of a sudden you find out there’s shortages. And we look back on every couple of years, this seems to happen. I wouldn’t be surprised if that were to happen in 2026 in certain regions of the world.”

- Celanese ($5B, Chemicals): “I do think there has continued to be an element of destocking. There was a lot of inventory throughout the value chain in this business. I think that will probably take another quarter or so. So, think mid-year where that evens out is our current estimation. And then, you should get to a bit more steady state and get a bit more balance as we get into the middle part of the year.”

- Louisiana-Pacific ($6B, Paper & Forest Products): “One consequence of recent market uncertainty is that dealers adopted a more cautious stance with regard to their inventory positions, holding fewer weeks of supply than normal. This adjustment coincided with a volume allocation prior to LP’s price increase that we now realized was somewhat larger than necessary. Unfortunately, the combined effect of these phenomena appears to have resulted in some pull forward at year-end, leading to elevated channel inventories with some of our two-step distribution partners.”

- Compass Minerals International ($1.1B, Metals & Mining): “Over time, as the balance sheet continues to improve and market dynamics adjust to historical norms, the optionality within our inventory management strategy will evolve. We’ve been very open that our inventory management plan could preclude our ability to meet excessive demand in fiscal 2026.”

- International Flavors & Fragrances ($17.8B, Chemicals): “While the overall performance of the company was very solid in 2025, I’m not as proud about the management of inventories. In the 1H of the year, we let inventories get higher than we had targeted. Mike had us put a lot of emphasis in the fourth quarter on driving down inventories, which is never a good thing to do quickly at the end of the year, but we did it. And we’ve put in a much better disciplined process to ensure that we manage inventories well throughout 2026 and for the future.”

- Packaging Corp of America ($19.8B, Containers & Packaging): “December got off to a strong start, leading us to believe that we would grow our volume over last year. Later in the month, customers appeared to manage their already low inventories further down for year end. The exception was e-commerce, which continued to remain strong well into the first week of January. In addition to the volume implications, this unfavorably impacted our December mix.”

Demand and End Markets

Strength in Infrastructure, Energy, and AI/Data Center Investment Serve as Key Growth Drivers into 2026, Offsetting Continued Softness in Residential, Automotive, and Other Interest Rate-sensitive End Markets

- Vulcan Materials ($39.6B, Construction Materials): “In 2026, we plan to continue our track record of compounding growth in what we expect to be an improving demand environment. We expect continued growth and public demand will now be complemented by improving private demand, resulting in modest overall growth in 2026.”

- Nucor ($41.2B, Metals & Mining): “For 2026, we continue to see strength in many of our primary end markets, including infrastructure, data centers and energy and in energy infrastructure. We are also seeing healthy demand related to advanced manufacturing in the border fence. While those markets remain strong, we have yet to see much improvement from interest rate sensitive markets like automotive and residential construction. In total, we expect domestic steel demand to be slightly up relative to 2025.”

- Freeport-McMoRan ($93.5B, Metals & Mining): “At a micro level, demand benefited from secular demand trends associated with electrification and AI data centers, and offset the impact of weakness in private construction and more cyclical sectors. Supply disruptions in copper and regional trade distortions, which drove significant material to the U.S., also impacted copper markets during 2025. In the U.S., our customers are reporting that data center demand represents the most significant source of growth for power cable and building wire. This growing sector is offsetting weakness in traditional demand sectors in residential construction and autos.”

- Celanese ($5B, Chemicals): “Electronics is the bright spot right now, it’s a net positive on a global basis. We’re seeing a global build-out from AI as well as data centers, and that’s positive in the electronics space. But it’s a small part of the overall base of the business. So, certainly, auto is a much larger piece of the base. And the business is going to trend kind of where that goes, at least at this point. And I would say auto is more mixed.”

- Element Solutions ($7.2B, Chemicals): “In the past year, demand from data center and high-performance computing markets drove 10% organic revenue growth in our electronics business, a trend that accelerated in Q4. Customer engagement is as strong as ever, partially driven by our pipeline of new, exciting products.”

- Amrize ($30B, Construction Materials): “You see continued infrastructure demand and an improving commercial landscape. In the commercial market, which makes up half of our business, demand is improving, led by new data centers. Data center construction has been and continues to be a significant bright spot as hyperscalers rapidly build out the infrastructure that will power the AI economy. This is the largest infrastructure expansion in recent history, and the U.S. is at the center. In fact, over 40% of global data center infrastructure investment is expected to be spent in the United States through 2030. In 2025 alone, we supported and supplied more than 30 data center projects, and we will see that work accelerating into this year.”

- Dow ($19.5B, Chemicals): “Across our packaging market vertical, global polyethylene fundamentals are expected to remain stable heading into 2026. Across the infrastructure sector, building and construction conditions are likely to gradually improve as interest rate cuts over the past 12 months gain traction. Housing starts and existing home sales remain well below historical averages, but there are some signs of positive momentum with existing home sales increasing for four months in a row. Consumer confidence have improved slightly but remains near historic lows, continuing to weigh on overall demand. At the same time, U.S. retail spending is holding steady in several categories with resilient sales of electronics as a bright spot.“

Cost Savings and Operational Excellence

Companies Continue to Execute Sizable Structural Cost Reduction Programs to Reset Cost Bases and Drive Multi-Year Margin Improvement, Including Facility Closures, Process Simplification, Automation, and Headcount Cuts

- Huntsman ($1.9B, Chemicals): “We targeted $100M of cost savings overall, which was head count reductions of ~500. This is almost 10% of the workforce, and closure of seven facilities. By the end of 2025, we’d achieved that annualized run rate of $100M. The in-year saving that we would expect in 2026, is about $45 million. excluding any impact from inflation. And you should get some additional savings to come through as well in 2027.”

- Cabot ($3.8B, Chemicals): “In fiscal year 2025, we delivered $50M of cost savings, and we expect to maintain these benefits in fiscal 2026. While we have new growth assets coming online that we anticipate will increase costs in fiscal year 2026, we expect these new assets will drive bottom line profitability. We also are focused on additional programs in fiscal 2026 that are targeted to reduce existing costs by another $30M. These programs include procurement savings, head count reductions in Reinforcement Materials, and benefits from accelerating technology deployment for improved yield and manufacturing efficiencies that we expect will be rolled out during fiscal 2026 and into fiscal 2027.”

- Constellium SE ($3.2B, Metals & Mining): “We’re pleased today to announce our next group-wide excellence program, which we’re calling Vision 2028. This program will target both operational efficiencies and cost reduction across our businesses and is one of the building blocks in our road map to our 2028 targets.”

- Olin ($2.5B, Chemicals): “In 2025, we delivered $44M in structural cost savings, and we expect to add an incremental $100M to $120M of annual Beyond250 savings during 2026 spread across our three businesses. We’ve enlisted outside expertise to help review our organization and processes against industry best practices. By streamlining our work processes, we’ve already been able to achieve a meaningful reduction in staffing. Through this exercise, we’ve identified many key performance metrics and gaps to close.”

- Dow ($19.5B, Chemicals): “We expect to deliver the remaining more than $500M in cost savings by the end of this year from our previously announced $1B program. Additionally, Transform to Outperform is expected to deliver at least $2B in near term EBITDA improvement. This work will radically simplify how we operate, streamline our end-to-end processes, reset our cost structure, and modernize how we serve our customers. As part of our commitment to operational excellence, we will simplify Dow’s operating model. We do anticipate this will include a global Dow workforce reduction of 4,500 roles. It will also result in a reduction of third-party roles and resources.This will allow us to speed up decision-making and put the right roles in the right areas of the company to better align with the changing market landscape and with where our customers are investing. We will also adopt new ways of working. This includes streamlining all of our end-to-end work processes by leveraging the power of automation and AI, which we expect will result in lower cost and improved efficiency across the entire organization.”

Around the World

North America and LatAm Remain Relatively Resilient, Europe is Stabilizing but Still Weak in Autos, and China is Bottoming Amid Mixed Demand and Policy Uncertainty

- Celanese ($5B, Chemicals): “You’ve got some uncertainty in China with some of the EV credits and stimulus rolling off in China to start the year. So, we’ve seen some softness in auto in China. Europe has been relatively stable to start the year. And U.S., with the fleet mix becoming a little more certain and a focus of the OEMs around ICE and hybrids, that could be a net good thing for us. But I would say to start the year, it’s about as expected.”

- Constellium SE ($3.2B, Metals & Mining): “In North America, demand is relatively stable, though the tariff environment is creating some uncertainties. Automotive demand in Europe remains weak, particularly in the premium vehicle segment where we have greater exposure. European markets are seeing increased Chinese competition and have lowered their battery electric vehicle ambitions. Automotive production in Europe is also feeling the impact of the current Section 232 auto tariffs, given the number of vehicles Europe exports to the U.S. Industrial market conditions in North America and Europe became more stable in the second half of 2025, and we believe the markets, particularly in Europe, have bottomed after 3 years of market downturn. Nevertheless, we expect the specialties markets in Europe to remain relatively weak in the near term. We do believe North America provide us with some opportunities today given the current tariffs make imports less competitive compared to domestic production.”

- Linde ($212.5B, Chemicals): “The U.S. has proven to be a really resilient market. Sales are up across almost every end market, electronics, commercial space, stand out in that in terms of growth that we’ve seen there. Manufacturing has been stable. There is still some caution when we speak to our customers. Latam sales have been stable and growing. Brazil stands out as having had a really good year last year, and we saw that play out in Q4 as well. Canada, on the other hand remains flat and I don’t see any catalyst for that changing anytime soon. The China markets that we supply and work with closely are largely bottoming out. India also had a continued strong growth. I think we were happy to see that almost all end markets in India were improving and moving forward. The rest of APAC, largely stable. Australia, the comps will also get better as you can expect, but should see some kind of recovery this year as we move forward.”

- International Flavors & Fragrances ($17.8B, Chemicals):“All regions in Q4 grew contributions from both volume and price. When we look at the drivers of growth, really what stood out is North America, and that’s driven by new wins. The team has been really focused on making sure they grow their pipeline and increase their win rate and what you’re starting to see it materialize was some of the success that they had on some of those launches overall. In addition, Latin America was strong. EMEA and Greater Asia, they grew, but to a lesser extent.”

- Sylvamo ($2B, Paper & Forest Products): “The overall European industry supply and demand environment continues to be challenging.However, market conditions have started to show signs of improvement as pulp prices began to rebound in Q4 and the improvement continues into Q1.”

In Closing

Overall, management commentary reflects signs of cautious optimism rather than conviction. The tone across calls suggests that while the worst of the downturn may be behind certain regions and end markets, the path forward remains uneven and highly dependent on rate trajectories, policy clarity, and sustained strength in infrastructure and AI-related investment. Visibility is improving incrementally, but not enough to support broad-based acceleration, which explains the measured guidance approach and continued emphasis on flexibility.

Importantly, companies are not waiting for demand to normalize before acting. Balance sheet discipline, continued structural cost actions, and operational simplification are positioning the sector to protect margins in the near term while enhancing leverage to an eventual recovery. If infrastructure, electrification, and data center buildouts continue to offset cyclical softness, incremental volume improvement could translate into outsized earnings impact given the leaner cost structures now in place.

The Materials sector enters 2026 more disciplined, more regionally selective, and increasingly tied to structural growth themes, but still navigating macro uncertainty and cautious customer behavior. While the Supreme Court’s ruling this morning clarified the limits of the Executive Branch’s authority to impose tariffs, uncertainty has increased as the path forward remains unclear and the administration is likely to pursue other legal justifications. We will continue to monitor the evolving trade landscape closely, as tariffs are likely to remain a central narrative element for exposed companies.

In the meantime, stay tuned for our Closing the Quarter piece next week, rounding out the Q4’25 earnings season!