This Week in Earnings – Q1'26Materials Sector Beat

Our Thought Leadership this week addresses:

- Key Events

- Earnings Snap, covering the S&P 500 stats to date

- Spotlight on Materials in The Sector Beat

Inflation Mitigation Spotlight: Price Actions, Cost Discipline, and Operational Adjustments

Key Events

- Reports that the U.S. and Iran were actively in discussions to pause the ongoing conflict sent a jolt of optimism through markets during the week, with global equities rallying and crude prices falling on the news. The proposed framework would unfold in three stages: formally ending the war, resolving the crisis in the Strait of Hormuz, and launching a 30-day window for negotiations on a broader agreement. Both parties still have a significant amount of work before an agreement can be reached, with both the U.S. and Iran issuing separate, mutually exclusive redlines concerning the future of Iranian nuclear enrichment. (Source: Bloomberg, Reuters, WSJ, CNBC)

- The ISM Services PMI survey registered 53.6% for April, reflecting continued expansion of the services sector. Despite coming in marginally lower than March’s print of 54.0%, the April report marked the 22nd consecutive month of expansion, with Business Activity (55.9%), Supplier Deliveries (56.8%), and Prices (70.7%) all firmly at expansion levels. New Orders saw the largest contraction, falling 7.1% from the month before 53.5%. (Source: Institute for Supply Management, CNBC)

- The March JOLTs report showed Job Openings remained relatively unchanged at seasonally adjusted 6.9M, while hires increased to 5.6M. Meanwhile, Quits were broadly stable at 3.2M, and Layoffs and Discharges were little changed at 1.9M. This broadly supports the view that labor markets are resilient despite recent inflationary and broader macro concerns, and is seen as supportive of the current level of interest rates. (Source: Bureau of Labor Statistics, CNBC, WSJ)

- The SEC formally proposed amendments that would allow public companies to elect semi-annual reporting instead of quarterly reporting this week. Under the proposal, companies can file a new Form 10-S for the first half of the year and continue filing an annual Form 10-K. This would replace the existing reporting cadence of three quarterly Form 10-Qs and one annual report. The proposed filing deadline would be either 40 or 45 days after the end of the semiannual period, depending on filer type. (Source: U.S. Securities and Exchange Commission, Journal of Accountancy)

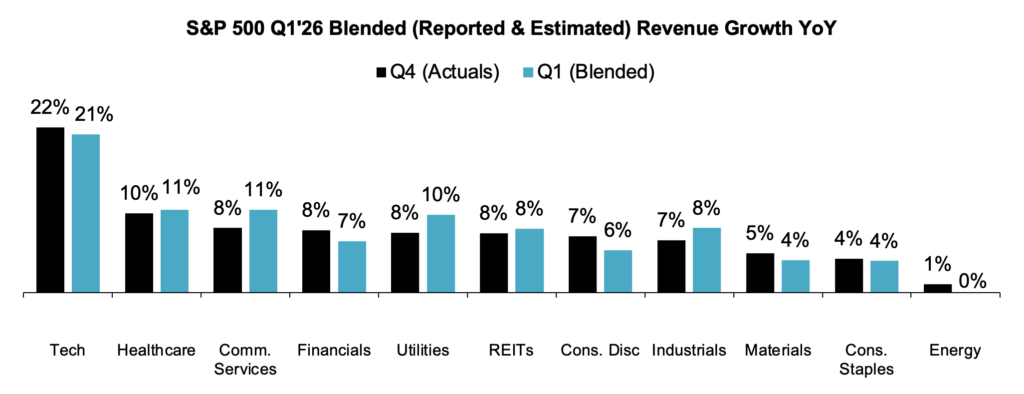

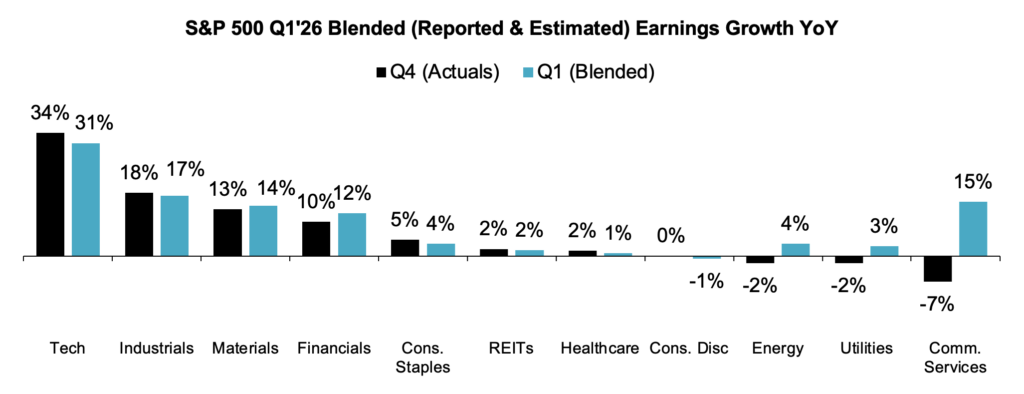

S&P 500 Earnings Snap

- 88% of the S&P 500 has reported earnings to date

Q1'26 Revenue Performance

- 78% have reported a positive revenue surprise, notably above the 1- and 5-year averages of 73% and 70%, respectively

- Blended revenue growth (combines actual reported results for companies and estimated results for companies yet to report) is 11%

- Companies are reporting revenue 2.1% above consensus estimates, higher than the 1- and 5- year averages of 9% and 2.0%, respectively

Q1'26 EPS Performance

- 84% have reported a positive EPS surprise, below the 1- and 5-year averages of 78% for both the 1- and 5- year averages.

- Blended earnings growth (combines actual reported results for companies and estimated results for companies yet to report) is 29%

- Companies are reporting earnings 1% above consensus estimates, above the 1- and 5-year averages of 7.1% and 7.3%, respectively

The Sector Beat – Materials

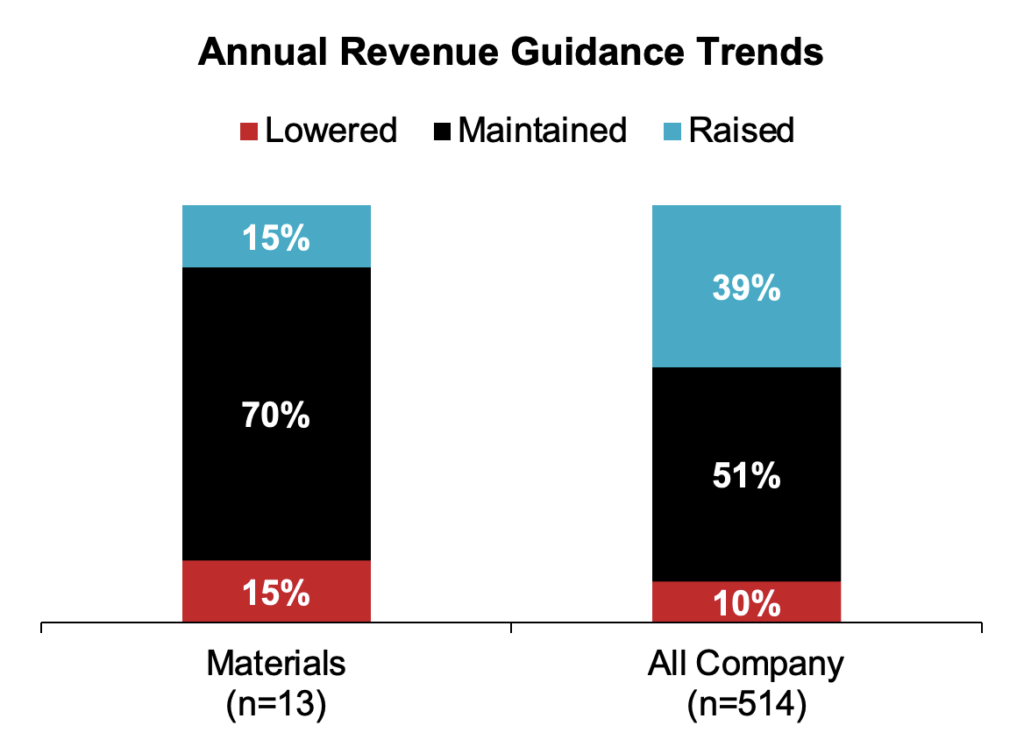

Materials Guidance Trends

We analyzed annual revenue and EPS guidance for calendar-year U.S. Materials companies with market caps ≥$1B that have reported to date.

For comparison purposes, we provide an All-Company benchmark that tracks, in real time, a basket of calendar-year companies with ≥$1B in market cap across all sectors that have reported earnings to date (n = 698).1

1. As of 5/7/2026

Guidance Breakdown by Industry1

Industry

# of Companies

Chemicals

16

Packaging & Containers

7

Construction Materials

3

Metals & Mining

3

Total

29

Revenue Guidance

To date, only 15% of Materials companies providing 2026 outlooks have Raised revenue guidance, compared to nearly 40% of the All-Company benchmark. As well, 15% Lowered annual revenue guidance, slightly above average, citing softer demand in international markets and select product categories. The majority Maintained guidance given the level of geopolitical and macro uncertainty at this time.

- Companies that Lowered guidance: (n = 2)

- Average midpoint: -2.1% growth versus 0.5% growth last quarter, compared to -5.9% a year ago

- Average spread: Decreased 90 bps from last quarter to 3%

- Companies that Maintained guidance: (n = 9)

- Average midpoint: 9% growth, compared to 11.6% last year

- Average spread: 7% versus 3.9% last year

- Companies that Raised guidance: (n = 2)

- Average midpoint: 7% growth versus 5.6% growth last quarter and 5.6% last year

- Average spread: Decreased 10 bps from last quarter to 2.9%

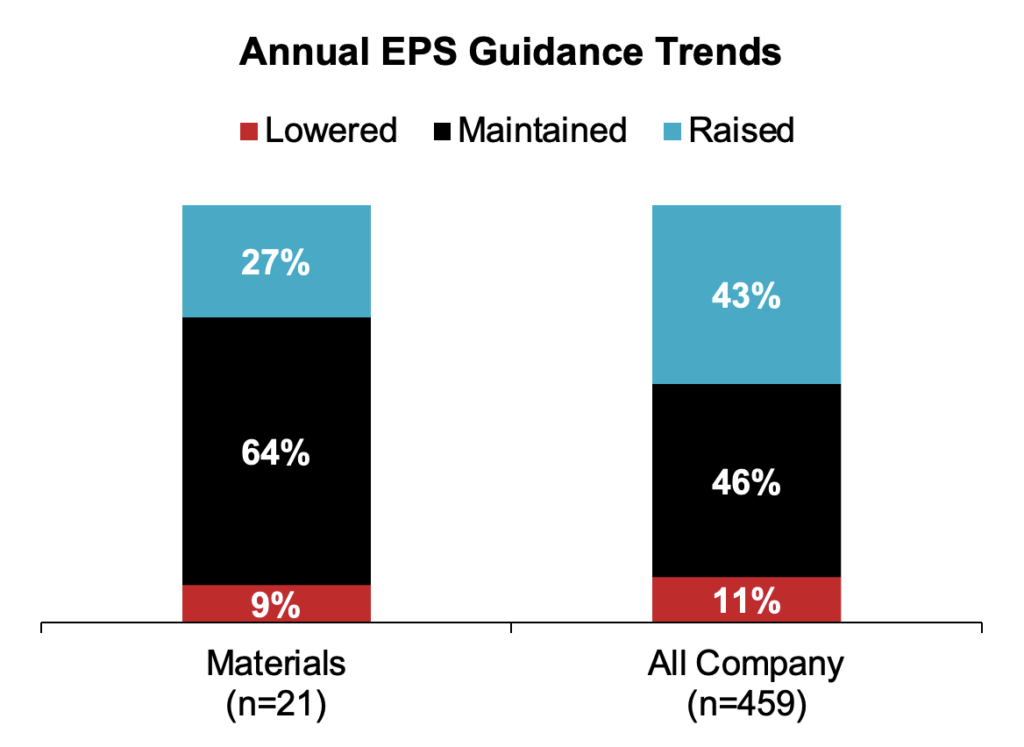

EPS Guidance

Similarly, only 27% of Materials companies Raised annual EPS guidance, with the majority choosing to Maintain outlooks.

- Companies that Lowered guidance: (n = 2)

- Average Midpoint: -6.5% growth versus 10.4% growth last quarter

- Average spread: Increased 650 bps from last quarter to 16.1%

- Companies that Maintained guidance: (n = 14)

- Average Midpoint: -1.4% growth, compared to 4.9% last year

- Average spread: 6.2% compared to 7.5% last year

- Companies that Raised guidance: (n = 5)

- Average Midpoint: 19.0% growth versus 16.1% growth last quarter, compared to 8.6% last year

- Average spread: Decreased 60 bps from last quarter to 2.6%, versus 4.3% last year

Earnings Call Analysis

In what has now become a cross-sector theme this reporting season, commentary among Materials companies struck a cautiously constructive tone. Management teams generally avoided sounding reactive, instead emphasizing pricing discipline, pass-through mechanisms, mitigation actions, and operating flexibility as critical tools in addressing the increased operating complexity introduced by the Iran War. This framing focused on stability and nimbleness rather than demand destruction, which some feared when the Conflict began.

That measured tone carried directly into Q&A. The focus shifted away from analysts assessing downside risk toward testing the durability of margin recovery and pricing power, and sizing the potential market-share gain opportunity. Analysts also focused on whether the ongoing global disruption is creating structural share-gain opportunities for North American producers and on management’s visibility into 2H. Steel producers were decisively positive in this regard, with executives highlighting lower import penetrations, strong order books, and protectionist tariff policies. Responses to analyst questions from Chemicals companies were more nuanced, with management teams acknowledging sequential improvement in demand but softness in durable goods, building and construction, and international buyers. Exiting the quarter, the core question is whether volumes, pricing, and order patterns among domestic producers reflect sustainable demand or are the result of a temporarily dislocated market.

Against that backdrop, guidance updates were generally stable across the group, though not without caveats. Companies that maintained guidance largely relied on cost actions, stronger volumes in select businesses, and mitigation plans to offset accelerating cost pressures from the Iran War. Given that most companies opted to maintain existing guidance rather than change it, investors will be looking to better gauge the extent to which improvements in Q1 results were driven by companies’ restocking and inventory buildup versus more structural tailwinds.

Messaging around capital allocation during the quarter was similarly disciplined, with companies emphasizing many of the shareholder-friendly aspects of their capital deployment decisions. Buybacks were positioned as opportunistic and supported by existing authorization capacity, divestiture proceeds, or improved leverage positions. Importantly, management teams did not position buybacks as a substitute for capex spend. Rather, they took a balanced approach that highlighted their commitment to funding core priorities while preserving the optionality to return capital to investors when the risk / reward is more compelling.

Separating the underlying demand from temporary support was also evident in end-market commentary. A consistent theme was the opportunity for U.S.-based producers to capture share as customers are beginning to place greater value on sourcing reliability, shorter supply chains, and reduced geopolitical exposure. This was most apparent in steel but was also present in chemical businesses with advantaged North American assets. This implication for IROs is important, as the sector’s opportunity is not solely tied to global volume recovery, but also to U.S. producers offering customers greater certainty and more resilient economics in an increasingly fragmented global trade environment.

Key Themes

Macro and Iran War

Companies Managing the Conflict through Price Increases; Higher Energy Costs Cloud 2H Visibility

- Linde ($228.2B, Chemicals): “With the Iranian conflict, it happened two-thirds into the quarter…one can roughly argue you had kind of two months before and one month after, based on the date. We’ve been seeing the…average pricing. So even though we’re a few percent below, pre and post that, there is a difference. And likely that price will continue to go up and roll its way through. I fully anticipate that to happen throughout the year.”

- Huntsman ($2.5B, Chemicals): “I struggle to see how inflationary pressures, particularly in areas reliant on imported energy, like much of Asia and Europe, will not see an inevitable downward pressure later in the year as consumer spending gradually shifts towards higher prices. To what degree this occurs is yet to be seen.”

- Stepan ($1.2B, Chemicals): “Our raw materials depend a lot on the oil supply chain, and we are seeing escalation in raw material inflation. We have a lot of pass-through contracts, and we have a disciplined process of increasing prices as well. In most of the businesses, we have been very successful in passing through the price increases in line with the raw material inflation. So that’s working through the system. It’s not only us, but it’s also the whole market going up, which gives us confidence that pricing will be sticky, more in some places than others, for sure. Raw material availability will continue to be a challenge because there are certain supply chains that are heavily impacted by the conflict in Iran, and there are some shortages in raw materials. The reality is that we could be growing faster than what we’re growing now, but we don’t have all the raw materials that we need.”

- Newmont ($115.6B, Metals & Mining): “Over the last few weeks, the world has experienced a notable increase in energy prices and impacts to global supply chain dynamics as a result of the ongoing conflict in the Middle East. We continue to monitor the geopolitical environment and its potential impact on cost closely.”

- Ecolab ($72.2B, Chemicals): “The operating environment remains dynamic…the conflict in the Middle East is one example. It has driven sharply higher global energy costs, creating additional pressure across supply chains.”

- Quaker Houghton ($2.4B, Chemicals): “Market conditions remain soft overall with pockets of incremental industrial gains tempered by weak automotive production. The hostilities in the Strait of Hormuz are creating inflationary pressure on raw materials and input costs, but so far, it has not had a significant direct or indirect impact on demand.”

Inventory

Risk Skews to Shortages Rather than Destocking, as Disrupted Supply Chains Constrain Raw Material Availability

- Huntsman ($2.5B, Chemicals): “From a sales perspective, we are seeing stronger-than-expected demand going well into Q2.This is being brought about by 3 factors: 1) , seasonality as we move into Q2 and the building season resumes across North America, Europe, and Asia; 2) customers who are buying ahead of the expected price increases that are being announced; and 3) disruptions that have been seen in certain trade flows that have impacted supply. An example of this would be some of our maleic customers in Europe who have become overly dependent on the Chinese supply of maleic and have seen a disruption in supply as raw materials and shipping costs have increased from that region. These 3 factors are also happening at a time when most inventory levels are very low across many supply chains.”

- PPG Industries ($23.2B, Chemicals): “Another positive data point, we are seeing our U.S. distributor fulfillment orders sequentially improve as industry levels — inventory levels normalize.”

- Tronox ($1.6B, Chemicals): “We are managing inventory, while maintaining flexibility. While we are not bringing all idled mining assets back online, we are evaluating selective ramp-ups where it makes sense, particularly for products where inventory levels are low, such as zircon.”

- Ashland ($2.4B, Chemicals): “We are not planning to make a significant inventory reduction. Given the uncertainty, we are focused right now on a specific product line. There are specific products that we’re going to build up.”

Guidance Updates and Key Assumptions

Outlooks Steady but Not Painless as Companies Rely on Pricing, Volume Strength, and Mitigation Actions to Absorb Iran War-Driven Expense Pressure

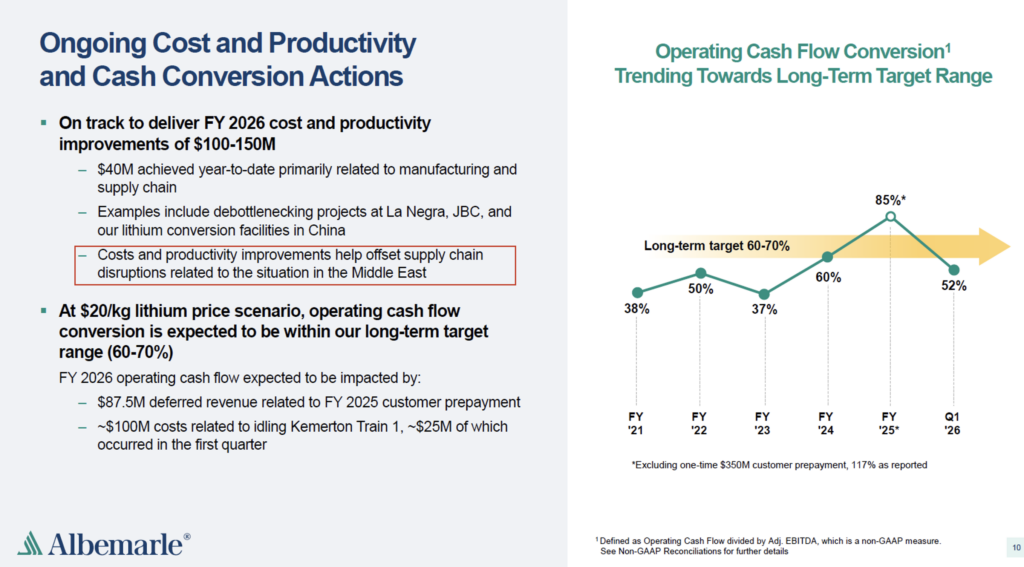

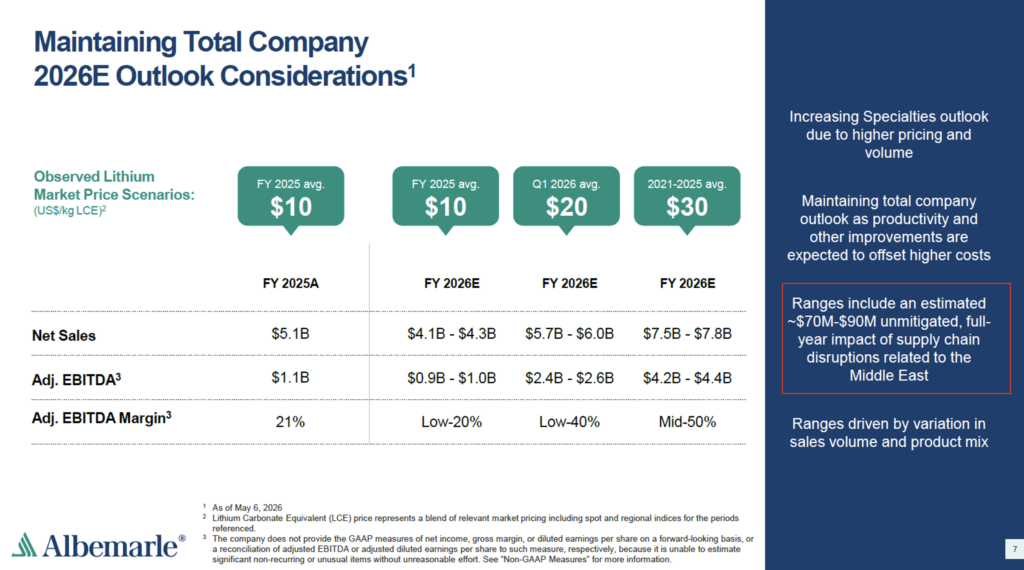

- Albemarle ($22.5B, Chemicals): “We are maintaining the company outlook for 2026 across all three price scenarios, despite global supply-chain disruptions related to the Middle East. We estimate that the unmitigated full-year impact of the supply-chain disruptions would be approximately $70 to $90M, and expect it to be offset by the… reduced interest expense following our debt reduction actions in Q1 and stronger than expected pricing and volumes in the specialties business, which gives us the confidence to increase our full-year specialties outlook.”

- International Paper ($16.5B, Containers & Packaging): “The key theme for Q2 is peak margin compression, as higher paper costs are realized ahead of pricing recovery. Energy-driven increases and paper prices are flowing through immediately, while pricing actions in packaging lag by roughly 3-6 months. This timing dynamic is pressuring margins in the near term before expanding as box pricing catches up…against that backdrop, price and mix are expected to be unfavorable for Q2.”

- Corteva ($54.7B, Chemicals): “With regards to the Middle East conflict, although we have minimal commercial presence in the area, we’re monitoring the situation closely.Given what we know today, while we’re keeping an eye on any feedstock exposure to our supply base, the main impact on Corteva is currently related to increases in oil prices. However, given typical inventory cycle turns, we believe that the 2026 impact is manageable within our current guidance range.”

- Chemours ($4.1B, Chemicals): “Despite a mixed global operating environment that includes challenging commercial end markets and overall raw material and other cost inflation, we still expect our full year consolidated net sales, adjusted EBITDA, and capital expenditure forecast to align with our previous guidance.”

- Newmont ($115.6B, Metals & Mining): “We are maintaining our cost guidance, and while higher oil prices may create incremental pressure, we view this as manageable at this time and are actively working to mitigate the impact, rather than viewing it as a risk to our operating plan. And as a reminder, the guidance we provided in February was based on a $70 per barrel Brent assumption, with diesel making up approximately 6% of our direct operating cost. For every $10 per barrel change in oil prices, we expect an approximate $60M impact on cost, which equates to roughly a $12 per ounce impact on all-in sustaining costs.”

- Sonoco ($4.9B, Containers & Packaging): “We are maintaining our full-year outlook, while recognizing that continued macroeconomic and geopolitical uncertainty, particularly late in our quarter, creates a dynamic operating environment. We will continue to monitor inflation and demand trends closely.”

End Markets

Demand Remains Steady but Uneven; Supply Constraints Create Share-Gain Opportunities for North American Producers…Datacenters Are the Gift that Keeps On Giving

- Ingevity ($2.6B, Chemicals): “What we saw this quarter, and we continue to see that trend in the early part of Q2, is that our competitors in Asia are actually pretty impacted by the Middle East conflict.We’ve been able to step in and provide volume in the shadow of that. We’ve taken advantage of what’s happening in that region of the world to supply those customers…APT [Advanced Polymer Technologies] was coming off a pretty prolonged period of demand weakness. So, we are starting to see some of that come back. Some of those costs and supply chain challenges have impacted some of our Asian competitors a bit more. So, we’re the beneficiary of that.”

- Martin Marietta ($36.2B, Construction Materials): “Beyond infrastructure, heavy non-residential construction demand continues to be driven by robust data center and power generation activity. Aggregates-intensive LNG work along the Gulf Coast is also gaining momentum, including projects such as the one at Port Arthur LNG, which Martin Marietta is actively supplying. Warehouse and distribution construction trends continue to recover as shipments increased positively in Q3’25 and have continued to trend favorably. By contrast, affordability pressures tied to higher interest rates continue to influence the pace of light non-residential and residential construction activity.”

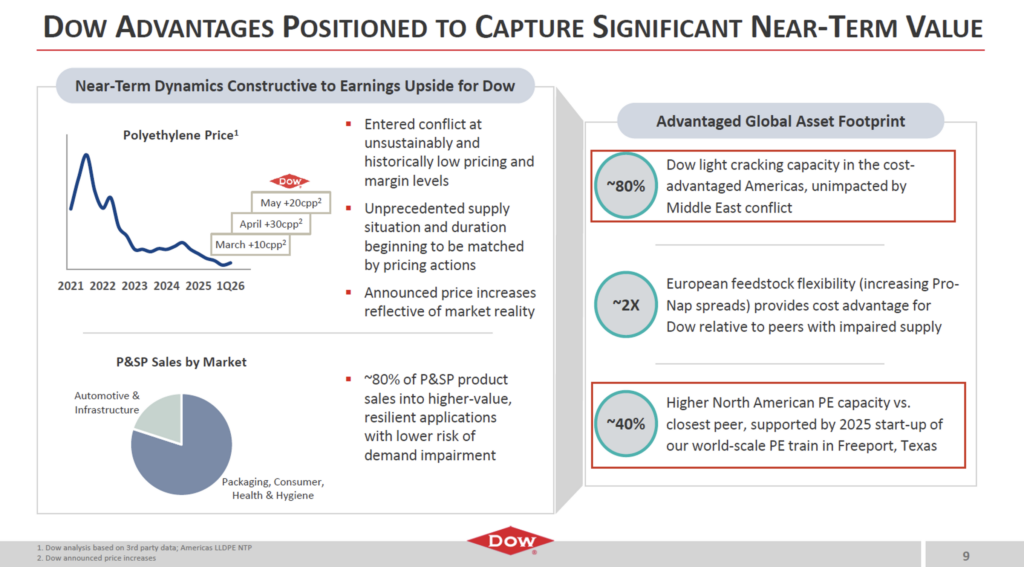

- Dow ($29.2B, Chemicals): “The headline is this – demand across many markets is steady. At the same time, supply is short, and arbitrage is increasing.On the demand side, for our core polyethylene packaging markets, conditions remain resilient, but we are seeing mixed signals in other key markets that Dow serves. Moving to supply dynamics, we anticipate that shutdowns, feedstock limitations, and logistical constraints will continue to reshape polyethylene product availability across regions. These conditions are creating ripple effects well beyond the Middle East, including significant impacts on logistics costs and transit time. Supply and feedstocks into Asia and Europe are constrained, which is triggering price increases globally. It is also leading to increased production in the Americas and is providing Dow with the opportunity to capture new business in Europe. The duration and severity of these constraints increase the likelihood of lasting industry impacts, including the potential for accelerated capacity rationalization as well as delays or cancellation of planned capacity additions.”

- Freeport-McMoRan ($79.9B, Metals & Mining): “Demand signals remain strong. Our customers in the US continue to report rising demand associated with AI datacenters and related energy infrastructure, which has more than offset weakness in private construction and in the auto sector. Recent reports from China reflect a significant resurgence of demand, with significant power grid spending and significant draws on Chinese exchange inventories in recent weeks.”

- Smurfit WestRock ($19.9B, Containers & Packaging): “The quarter was also characterized by generally tepid demand, as consumer confidence remained muted, and the company experienced some logistical difficulties in Mexico as a result of local domestic security-related issues. As we begin Q2, we are seeing much improved demand with strengthening order books across all grades of both paper and converting products.”

Around the World

Global Disruption Reshuffling Trade Flows; Asia and Europe More Constrained While North American Producers Gain Volume and Export Opportunities

- Dow ($29.2B, Chemicals): “In the two months since the conflict began, the scale of disruption we have seen is unprecedented…transit through the region remains significantly impaired, largely driven by the ongoing disruption in the Strait of Hormuz. And the disruption has been amplified across Asia and Europe, tightening feedstock availability and pushing producers to reduce production or increase prices to cover the rapidly escalating costs occurring from the Conflict. Looking across regions, a large portion of Middle East capacity remains offline, with increasing risk of lasting infrastructure damage. In the Asia Pacific, feedstock constraints are limiting operating rates and reducing export availability, challenging producers who are operating at uncompetitive levels. And in Europe, high costs will require continued price increases to justify additional production. In contrast, the Americas continue to operate at high rates…it is estimated that roughly 3/4 of announced global capacity additions would be either directly impacted by the Conflict or dependent on supply chains that remain highly constrained. The longer these conditions persist, the greater the potential for further industry changes. And lastly, it is not likely that the pricing impact of these events will be temporary. We expect rising global production costs and a steepening global cost curve to continue influencing pricing and spreads.”

- International Paper ($16.5B, Containers & Packaging): “In both North America and EMEA, overall market demand is softer than we expected coming into the year by about 1 point. This reflects a more cautious consumer, particularly as inflation pressures and uncertainty persist. We have not seen abrupt changes in order patterns in either region, but I’m cautious about demand.”

- Linde ($228.2B, Chemicals): “EMEA continues to experience negative volumes, primarily from on-site customers shifting production to more competitive assets outside continental Europe. It remains to be seen what the longer-term effects could be for the Middle East conflict, but so far it appears activity is relocating to more feedstock advantaged assets in the Americas, and to a lesser extent, APAC.”

Capital Allocation

Companies Favor Shareholder Returns and Lean In Hard On Buybacks

- Ingevity ($2.6B, Chemicals): “We accelerated our share repurchases in Q1 beyond the ratable cadence we had planned. We remain committed to de-risking our balance sheet and reducing net leverage to our target of 2-2.5x while being opportunistic with share buybacks.”

- Scott’s Miracle-Gro ($3.4B, Chemicals): “First, we’re ready to embark on the first tranche of the multiyear share repurchase program we announced last quarter and said would begin once leverage was comfortably in the 3.0xs. We’re there. The ultimate goal is to buy back at least 1/3 of our outstanding shares. It will be earnings accretive, won’t add to our debt level, and has 0 implementation risk.”

- DuPont de Nemours ($18.6B, Chemicals): “We expect to launch a $275M accelerated share repurchase under our existing program, a clear example of how we continue to advance our strategic priority of driving disciplined capital allocation by returning cash to shareholders.”

- CRH ($74B, Construction Materials): “We also continue to return significant amounts of cash to our shareholders. Our ongoing share buyback program has returned approximately $400M so far this year, and today we are commencing a further quarterly tranche of $300M, to be completed no later than the 28th of July.”

- Air Products and Chemicals ($66.4B, Chemicals): “We remain committed to disciplined capital allocations that ensure that we are well-positioned to continue our strong track record of returning cash to our shareholders. In the 1H of fiscal 2026, we have returned $800M to shareholders in the form of dividends.”

- Avery Dennison ($12.3B, Containers & Packaging): “Our capital allocation during Q1 remained consistent with our established framework, and we returned $133M to shareholders through a balanced combination of $72M in dividends and $61M in share repurchases.”

Inflation Mitigation Spotlight: Price Actions, Cost Discipline, and Operational Adjustments

In reviewing Q1’26 earnings communications for Materials companies most exposed to oil-linked feedstocks, energy, logistics, and global trade, they frame the Iran War as significantly disrupting supply chains and costs, though not a broad-based demand shock.

The dominant response has been pricing actions, contractual pass-throughs, cost mitigation, and supply reliability as the primary levers available to management to protect margins.

- Companies with more direct commodity and feedstock exposure tended to be more explicit on pricing actions

- Several producers described selective or broad-based price increases tied to higher energy, raw materials, and/or transportation costs

- Communicating pass-through mechanisms were common; companies with shorter pricing cycles, contractual recovery, and/or stronger market positions struck a more confident tone

- Cost mitigation was generally framed as a preventative measure for future potential issues rather than an emergency action

- Management teams pointed to productivity programs, fixed-cost reduction, working-capital discipline, and capex prioritization to offset higher input costs

- Some energy-intensive companies opted to highlight operational responses to increased fuel costs, specifically calling out altered transportation routes or leveraging AI and similar tools to enhance operating performance

Select examples from earnings materials include:

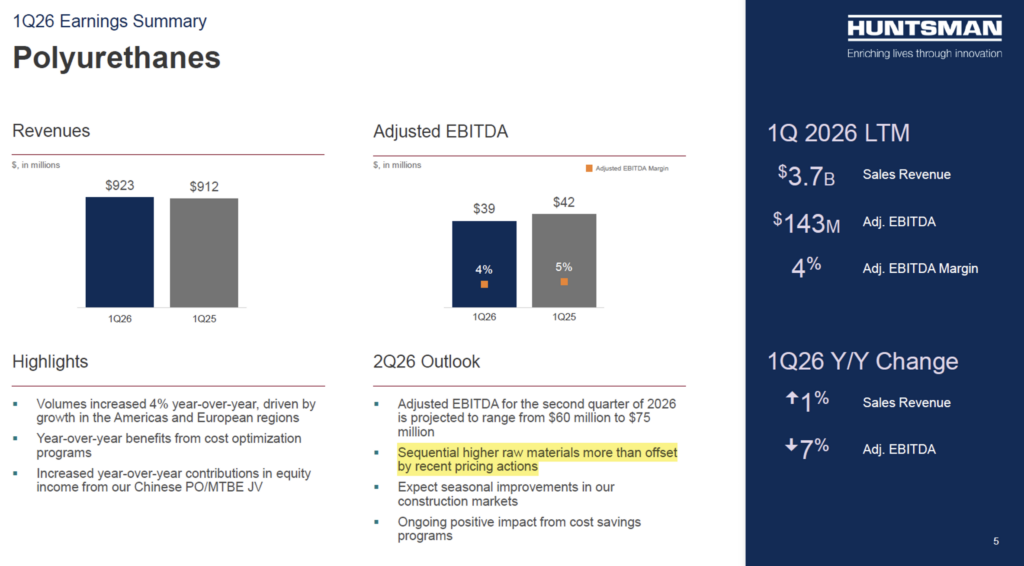

Huntsman ($2.6B, Chemicals): Noted recent pricing actions more than offset higher raw material costs

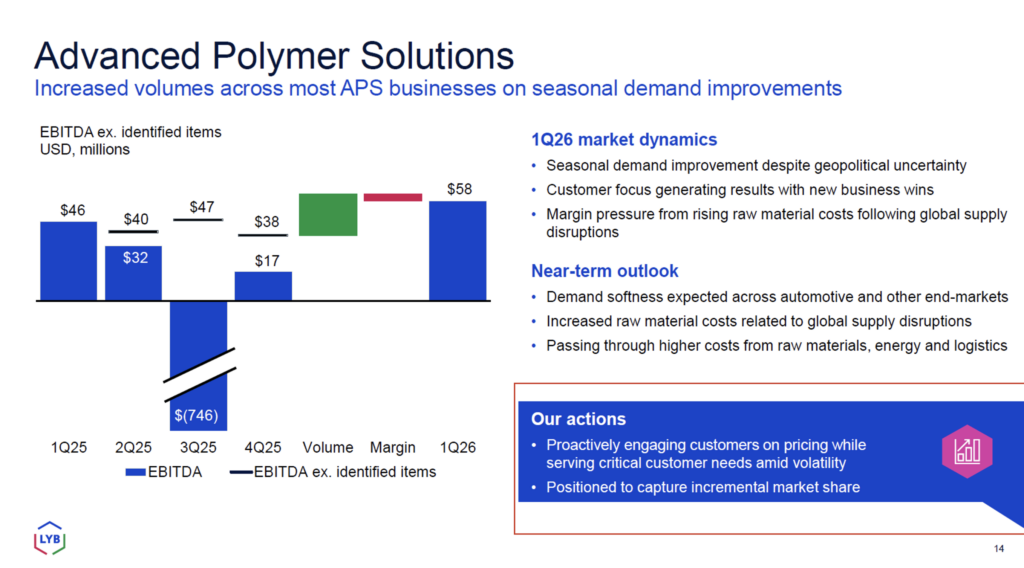

LyondellBasell ($23.1B, Chemicals): Noted actively engaging with customers on pricing

Albemarle: ($23.4B, Chemicals): Noted ongoing Iran War and its business impact, sized impact from supply chain disruptions in outlook

Dow ($29.2B, Chemicals): Highlighted relative insulation from conflict due to the advantages of North American assets

In Closing

Commentary from the front-line Materials Sector points to an ecosystem experiencing regional dislocation, benefiting North American-based producers, and to broad-based higher costs amid supply chain constraints, inflation, and pricing pass-through. While demand is currently holding up, the fluidity of events has some executives concerned about future buying activity, especially among consumers. Based on executive commentary, with the majority of companies preserving annual outlooks at this time, the global macro environment is showing more pronounced signs of stress.